Tesco 2010 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2010 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

Financial statements

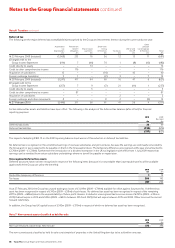

• IFRS 3 (revised) ‘Business Combinations’, effective for business

combinations for which the acquisition date is on or after the beginning

of the first annual reporting period beginning on or after 1 July 2009.

The revised standard continues to apply the acquisition method to

business combinations, with some significant changes, including: all

payments to purchase a business are to be recorded at fair value at the

acquisition date, with the contingent payments that are classified as

debt subsequently remeasured through the Group Income Statement.

There is a choice on an acquisition-by-acquisition basis to measure the

non-controlling interest in the acquiree either at fair value or at the non-

controlling interest’s proportionate share of the acquirer’s net assets.

All acquisition-related costs should be expensed. The Group will apply

IFRS 3 (revised) prospectively to all business combinations from

28February 2010.

• Amendment to IAS 39 ‘Financial Instruments: Recognition and

Measurement’ – Eligible Hedged Items, effective for annual periods

beginning on or after 1 July 2009. The amendment provides clarification

on how the principles that determine whether a hedged risk or portion

of cash flows is eligible for designation should be applied in particular

situations.

• IFRS 9 ‘Financial Instruments’, effective for annual periods beginning on

or after 1 January 2013. This is the first part of a new standard on

classification and measurement of financial assets that will replace IAS 39.

• Amendment to IAS 24 ‘Related Party Disclosures’, effective for annual

periods beginning on or after 1 January 2011.

• IFRIC 17 ‘Distributions of Non-Cash Assets to Owners’, effective for

annual periods beginning on or after 1 July 2009.

• IFRIC 18 ‘Transfers of Assets from Customers’, effective for transfers of

assets from customers received on or after 1 July 2009.

• IFRIC 19 ‘Extinguishing Financial Liabilities with Equity Instruments’,

effective for annual periods beginning on or after 1 July 2010.

The Group continually reviews amendments to the standards made under

the IASB’s annual improvements project.

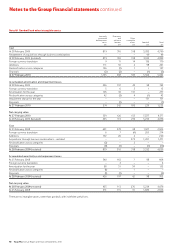

Use of non-GAAP profit measures – underlying profit before tax

The Directors believe that underlying profit before tax and underlying

diluted earnings per share measures provide additional useful information

for shareholders on underlying trends and performance. These measures

are used for internal performance analysis. Underlying profit is not defined

by IFRS and therefore may not be directly comparable with other

companies’ adjusted profit measures. It is not intended to be a substitute

for, or superior to IFRS measurements of profit.

The adjustments made to reported profit before tax are:

• IAS 32 and IAS 39 ‘Financial Instruments’ – fair value remeasurements –

Under IAS 32 and IAS 39, the Group applies hedge accounting to its

various hedge relationships when allowed under the rules of IAS 39

and when practical to do so. Sometimes the Group is unable to apply

hedge accounting to the arrangements but continues to enter into

these arrangements as they provide certainty or active management

of the exchange rates and interest rates applicable to the Group.

The Group believes these arrangements remain effective and

economically and commercially viable hedges despite the inability

to apply hedge accounting.

Where hedge accounting is not applied to certain hedging

arrangements, the reported results reflect the movement in fair value of

related derivatives due to changes in foreign exchange and interest

rates. In addition, at each period end, any gain or loss accruing on open

contracts is recognised in the Group Income Statement for the period,

regardless of the expected outcome of the hedging contract on

termination. This may mean that the Group Income Statement charge is

highly volatile, whilst the resulting cash flows may not be as volatile. The

underlying profit measure removes this volatility to help better identify

underlying business performance. During 2010 there was no impact

(2009 – £10m) of the IAS 32 and IAS 39 charge arose in the share of

post-tax profit of joint ventures and associates, with the remainder in

finance income/costs.

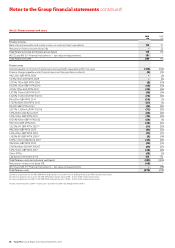

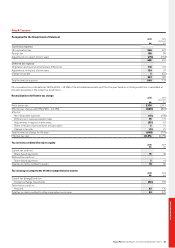

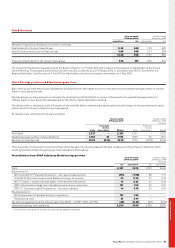

Note 1 Accounting policies continued

• IAS 19 Income Statement charge for pensions – Under IAS 19

‘Employee Benefits’, the cost of providing pension benefits in the

future is discounted to a present value at the corporate bond yield

rates applicable on the last day of the previous financial year.

Corporate bond yield rates vary over time which in turn creates

volatility in the Group Income Statement and Group Balance Sheet.

IAS 19 also increases the charge for young pension schemes, such as

Tesco’s, by requiring the use of rates which do not take into account

the future expected returns on the assets held in the pension scheme

which will fund pension liabilities as they fall due. The sum of these

two effects can make the IAS 19 charge disproportionately higher and

more volatile than the cash contributions the Group is required to

make in order to fund all future liabilities. Therefore, within underlying

profit we have included the ‘normal’ cash contributions for pensions

but excluded the volatile element of IAS 19 to represent what the

Group believes to be a fairer measure of the cost of providing post-

employment benefits.

• IAS 17 ‘Leases’ – impact of annual uplifts in rent and rent-free periods

– The amount charged to the Group Income Statement in respect of

operating lease costs and incentives is expected to increase significantly

as the Group expands its international business. The leases have been

structured in a way to increase annual lease costs as the businesses

expand. IAS 17 ‘Leases’ requires the total cost of a lease to be

recognised on a straight-line basis over the term of the lease,

irrespective of the actual timing of the cost. The impact of this

treatment in 2010 was a charge of £41m (2009 – £27m) to the Group

Income Statement after deducting the impact of the straight-line

treatment recognised as rental income within share of post-tax profits

of joint ventures and associates.

• IFRS 3 Amortisation charge from intangible assets arising on

acquisition – Under IFRS 3 ‘Business Combinations’, intangible assets

are separately identified and valued. The intangible assets are

required to be amortised on a straight-line basis over their useful

economic lives and as such is a non-cash charge that does not reflect

the underlying performance of the business acquired.

• IFRIC 13 ‘Customer Loyalty Programmes’ – This new interpretation

requires the fair value of customer loyalty awards to be measured

as a separate component of a sales transaction. The underlying profit

measure removes this fair value allocation to present underlying

business performance, and to reflect the performance of the

operating segments as measured by management.

• Exceptional items – Due to their significance and special nature,

certain other items which do not reflect the Group’s underlying

performance have been excluded from underlying profit. These gains

or losses can have a significant impact on both absolute profit and

profit trends; consequently, they are excluded from the underlying

profit of the Group. For the year ended 27 February 2010, exceptional

items are as follows:

– IAS 36 Impairment of goodwill arising on acquisitions – the carrying

value of goodwill relating to Japan was not fully recoverable,

resulting in an impairment charge of £131m (2009 – £nil), and as

such is a non-cash charge that does not reflect the underlying

performance of the business. The recoverable amount for Japan

was based on value in use, calculated from cash flow projections for

five years using data from the Group’s latest internal forecasts, the

results of which are reviewed by the Board.

– Restructuring costs – These relate to certain costs associated with

the Group’s restructuring activities. For the year ended 27 February

2010, the Group incurred £33m (2009 – £nil), relating to

restructuring activities.

There were no exceptional items in 2009.

Tesco PLC Annual Report and Financial Statements 2010 81