JVC 2000 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2000 JVC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

|

|

28 JVC 2000

The ranges of useful lives for computing depreciation are generally

as follows:

Buildings ...................................................................... 20 to 50 years

Machinery and equipment............................................ 3 to 7 years

Expenditures for maintenance and repairs are charged to income as

incurred.

Software costs

In accordance with the provisional rule of the JICPA’s Accounting

Committee Report No.12 “Practical Guidance for Accounting for

Research and Development Costs, etc.” (the “Report”), the Company

accounts for software which was included in long-term prepaid ex-

penses in investments and other in the same manner in 2000 as in

1999. Pursuant to the Report, however, the Company included

software in intangible assets in 2000. Software costs are amortized

using the straight-line method over the estimated useful lives (three to

five years). The amount for 1999 has been reclassified to conform to

the 2000 presentation.

Finance leases

Finance leases, except those leases for which the ownership of the

leased assets is considered to be transferred to the lessee, are ac-

counted for in the same manner as operating leases.

Research and development

Research and development expenditures for new products or improve-

ment of existing products are charged to income as incurred.

Income taxes

The Company provided income taxes at the amounts currently payable

for the years ended March 31, 1999 and 1998. Effective April 1, 1999,

the Company adopted the new accounting standard, which recognizes

tax effects of temporary differences between the financial statement

carrying amounts and the tax basis of assets and liabilities. Under the

new accounting standard, the provision for income taxes is computed

based on the pretax income included in the consolidated statement of

income. The asset and liability approach is used to recognize deferred

tax assets and liabilities for the expected future tax consequences of

temporary differences.

The amount of deferred income taxes attributable to the net tax

effects of the temporary differences at April 1, 1999 is reflected as a

cumulative adjustment of ¥27,259 million ($257,160 thousand) to the

retained earnings brought forward from the previous year. Prior years’

financial statements have not been restated.

As a result of adopting the tax effect accounting, deferred tax assets

and long-term deferred tax assets at March 31, 2000 were decreased

by ¥6,170 million ($58,208 thousand) and ¥14,729 million ($138,953

thousand), respectively, deferred tax liabilities and long-term deferred

tax liabilities at that date were increased by ¥460 million ($4,340 thou-

sand) and ¥44 million ($415 thousand), respectively, net loss for the

year ended March 31, 2000 was decreased by ¥1,959 million ($18,481

thousand), and the retained earnings at April 1, 1999 was decreased by

¥27,259 million ($257,160 thousand).

Employees’ retirement benefits and pension plans

The Company has funded pension plans and unfunded benefit plans to

provide retirement benefits for substantially all employees. Approxi-

mately 85% of total retirement benefits for employees is covered by

funded pension plans.

Upon retirement or termination of employment for reasons other

than dismissal for cause, eligible employees are entitled to lump-sum

and/or annuity payments based on their current rates of pay and length

of service.

Employees’ retirement benefits is principally stated at 40% (100%

for certain employees whose age reached 55) of the amount which

would be required to be paid (less the amount which is expected to be

covered by the pension plans) if all eligible employees voluntarily termi-

nated their employment at the balance sheet date, plus the unamor-

tized balance of certain previously accumulated amounts.

Costs with respect to the pension plans are funded as accrued in an

amount determined actuarially. Prior service costs are being funded

over 10 years and the resultant charges to income are offset by amorti-

zation of the excess amount of employees’ retirement benefits which is

expected to be covered by the pension plans.

Certain of the consolidated subsidiaries also have employees’ retire-

ment benefit plans and funded pension plans similar to those of the

Company.

Amounts per share of common stock

The computation of net income per share is based on the weighted av-

erage number of shares of common stock outstanding during each

year.

Diluted net income per share assumes dilution that could occur if

convertible bonds or similar securities were converted into common

stock exercised to result in the issuance of common stock. As the

Company reported net losses for the years ended March 31, 2000,

1999, and 1998, inclusion of potential common shares would have an

antidilutive effect on per share amounts. Accordingly, the Company’s

basic and diluted earnings per share computations are the same for the

periods presented.

Cash dividends per share represent the actual amount declared as

applicable to the respective years.

Reclassifications

Certain prior year amounts have been reclassified to conform to the

2000 presentation. These changes had no impact on previously

reported results of operations or shareholders’ equity.

3. TRANSACTIONS WITH MATSUSHITA ELECTRIC

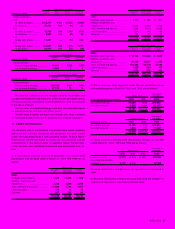

INDUSTRIAL CO., LTD.

The Company is a subsidiary of Matsushita Electric Industrial Co., Ltd.

(“Matsushita”). The Company’s relationship with Matsushita dates back

to 1954, when Matsushita acquired a controlling equity interest in the

Company. Since then, the Company has pursued an independent

management policy in all aspects of its operations based on the

principle of “mutual development through competition.” There is no re-

lationship of financial assistance between the two companies. Each

company has a right of access to the technology developed by the

other. At March 31, 2000, Matsushita held 133,227 thousand shares of

common stock of the Company, 52.40% of the total outstanding

shares.

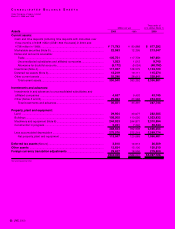

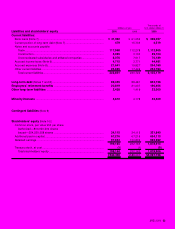

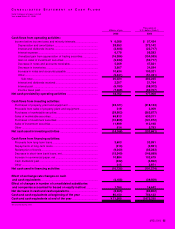

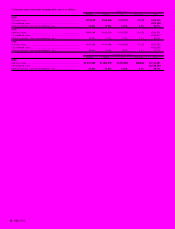

Major account balances with Matsushita at March 31, 2000 and

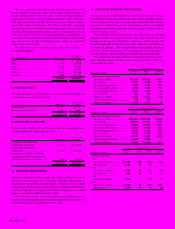

1999 were as follows:

Thousands of

Millions of yen U.S. dollars

2000 1999 2000

Due from Matsushita ....................... ¥ 298 ¥ 167 $ 2,811

Due to Matsushita ........................... 3,030 3,011 28,585

Sales to and purchases from Matsushita for the years ended March

31, 2000, 1999 and 1998 were as follows:

Thousands of

Millions of yen U.S. dollars

2000 1999 1998 2000

Net sales......................... ¥ 900 ¥1,352 ¥1,125 $ 8,491

Net purchases................. 35,879 30,558 33,225 338,481