HSBC 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

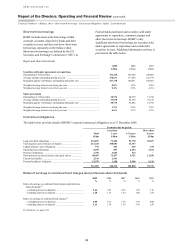

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Critical accounting policies

62

level of interest rates, portfolio seasoning, account

management policies and practices, changes in laws

and regulations, and other factors that can affect

customer payment patterns. Different factors are

applied in different regions and countries to reflect

the variation in economic conditions, laws and

regulations. The assumptions underlying this

judgement are highly subjective. The methodology

and the assumptions used in calculating impairment

losses are reviewed regularly in the light of

differences between loss estimates and actual loss

experience. For example, roll rates, loss rates and the

expected timing of future recoveries are regularly

benchmarked against actual outcomes to ensure they

remain appropriate.

The total amount of the Group’s impairment

allowances on homogeneous groups of loans is

inherently uncertain because it is highly sensitive to

changes in economic and credit conditions across a

large number of geographical areas. Economic and

credit conditions within geographical areas are

influenced by many factors with a high degree of

interdependency so that there is no single factor to

which the Group’s loan impairment allowances as

a whole are sensitive. However, HSBC’s loan

impairment allowances are particularly sensitive to

general economic and credit conditions in North

America. For example, a 10 per cent increase in

impairment allowances on collectively assessed

loans and advances in North America would increase

loan impairment allowances by US$1.3 billion at

31 December 2009 (2008: US$1.6 billion). It is

possible that the outcomes within the next financial

year could be different from the assumptions built

into the models, resulting in a material adjustment to

the carrying amount of loans and advances.

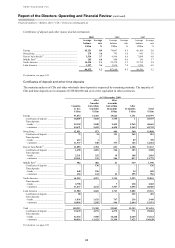

Goodwill impairment

HSBC’s accounting policy for goodwill is described

in Note 2p on the Financial Statements. Note 22 on

the Financial Statements lists the Group’s cash

generating units (‘CGU’s) by geographical region

and global business. Total goodwill for the Group

amounted to US$23 billion as at 31 December 2009

(2008: US$22 billion).

The process of identifying and evaluating

goodwill impairment is inherently uncertain because

it requires significant management judgement in

making a series of estimations, the results of which

are highly sensitive to the assumptions used. The

review of goodwill impairment represents

management’s best estimate of the factors below:

• the future cash flows of the CGUs are sensitive

to the cash flows projected for the periods for

which detailed forecasts are available, and to

assumptions regarding the long-term pattern of

sustainable cash flows thereafter. Forecasts are

compared with actual performance and

verifiable economic data in future years;

however, the cash flow forecasts necessarily and

appropriately reflect management’s view of

future business prospects at the time of the

assessment; and

• the rate used to discount the future expected

cash flows is based on the cost of capital

assigned to an individual CGU, and can have a

significant effect on the CGU’s valuation. The

cost of capital percentage is generally derived

from a Capital Asset Pricing Model, which

incorporates inputs reflecting a number of

financial and economic variables, including the

risk-free interest rate in the country concerned

and a premium to reflect the inherent risk of the

business being evaluated. These variables are

subject to fluctuations in external market rates

and economic conditions outside management’s

control and are therefore established on the basis

of significant management judgement and are

subject to uncertainty.

When this exercise demonstrates that the

expected cash flows of a CGU have declined and/or

that its cost of capital has increased, the effect is to

reduce the CGU’s estimated recoverable amount.

If this is lower than the carrying value of the CGU,

a charge for impairment of goodwill will be

recognised in HSBC’s income statement for the year.

The accuracy of forecast cash flows is subject to

a high degree of uncertainty in volatile market

conditions. In such market conditions, management

retests goodwill for impairment more frequently than

annually to ensure that the assumptions on which the

cash flow forecasts are based continue to reflect

current market conditions and management’s best

estimate of future business prospects.

During 2009, no impairment of goodwill was

identified (2008: US$10.6 billion). In addition to

the annual impairment test which was performed as

at 1 July 2009, HSBC reviewed the current and

expected performance of the CGUs as at

31 December 2009 and determined that there was no

indication of potential impairment of the goodwill

allocated to them. However, in the event of a

significant deterioration in economic and credit

conditions compared with those reflected by

management in the cash flow forecasts for the CGUs,

a material adjustment to a CGU’s recoverable amount

may occur which may result in the recognition of an

impairment charge in the income statement.