HSBC 2009 Annual Report Download - page 286

Download and view the complete annual report

Please find page 286 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

Insurance operations > PVIF > Non-economic assumptions // Capital management and allocation

284

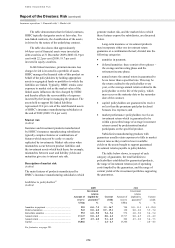

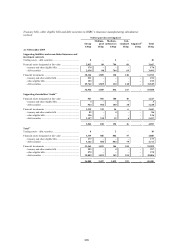

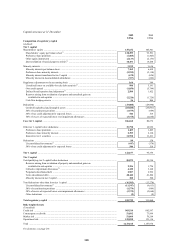

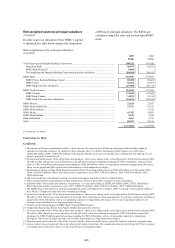

Movements in total equity and PVIF of insurance operations

(Audited)

2009 2008

Tota l

equity

PVIF

included in

total equity

Total

equity

PVIF

included in

total equity

US$m US$m US$m US$m

At 1 January ............................................................................... 7,577 2,033 8,430 1,965

Value of new business written during the year71 ....................... 600 600 452 452

Movements arising from in-force business:

– expected return ................................................................... (123) (123) (186) (186)

– experience variances72 ........................................................ (44) (44) (36) (36)

– change in operating assumptions ....................................... 48 48 (7) (7)

Investment return variances ....................................................... 16 16 (94) (94)

Changes in investment assumptions .......................................... 19 19 12 12

Return on net assets ................................................................... 522 – (310) –

Exchange differences and other ................................................. (83) 231 (93) (73)

Capital transactions .................................................................... 48 – (591) –

At 31 December ......................................................................... 8,580 2,780 7,577 2,033

For footnotes, see page 291.

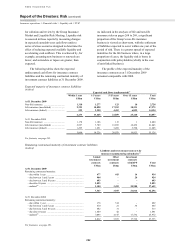

Non-economic assumptions

(Audited)

The policyholder liabilities and PVIF are determined

by reference to non-economic assumptions which

include, for non-life manufacturers, claims costs and

expense rates and, for life manufacturers, mortality

and/or morbidity, lapse rates and expense rates. The

table below shows the sensitivity of profit for the

year to, and total equity at, 31 December 2009 to

reasonably possible changes in these non-economic

assumptions at that date across all insurance

manufacturing subsidiaries, with comparatives for

2008.

The cost of claims is a risk associated with non-

life insurance business. An increase in claims costs

would have a negative effect on profit. The main

exposures to this scenario are in the UK, Hong

Kong, Latin America and Bermuda.

Mortality and morbidity risk is typically

associated with life insurance contracts. The effect of

an increase in mortality or morbidity on profit

depends on the type of business being written. For a

portfolio of term assurance contracts, an increase in

mortality usually has a negative effect on profit as

the number of claims increases. For a portfolio of

annuity contracts, an increase in mortality rates

typically has a positive effect on profit as the period

over which the benefit is being paid to the

policyholder is shortened. However, when an

annuity contract includes life cover, the positive

effect on profit of the increase in mortality may be

offset by the benefits payable under the life

insurance. The largest exposures to mortality and

morbidity risk exist in France, Hong Kong, the UK

and the US.

Sensitivity to lapse rates is dependent on the

type of contracts being written. For insurance

contracts, the cost of claims is funded by premiums

received and income earned on the investment

portfolio supporting the liabilities. For a portfolio of

term assurance, an increase in lapse rates typically

has a negative effect on profit due to the loss of

future premium income on the lapsed policies. For a

portfolio of annuity contracts, an increase in lapse

rates has a positive effect on profit as the obligation

to pay future benefits on the lapsed contracts is

extinguished. France, Hong Kong, the UK and the

US are the sites which are most sensitive to a change

in lapse rates.

Expense rate risk is the exposure to a change in

expense rates. To the extent that increased expenses

cannot be passed on to policyholders, an increase in

expense rates will have a negative impact on profits.