HSBC 2009 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

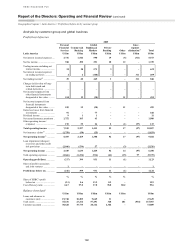

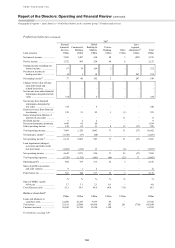

HSBC HOLDINGS PLC

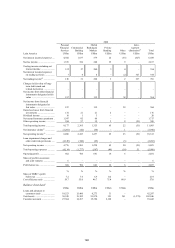

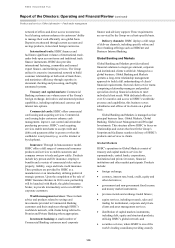

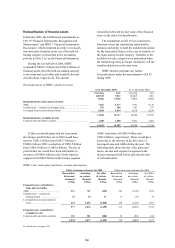

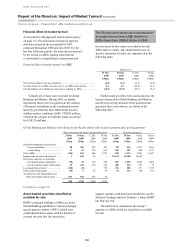

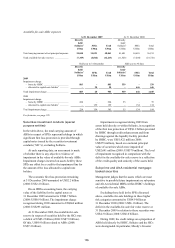

Report of the Directors: Impact of Market Turmoil

151

Background and disclosure policy

(Audited)

As a result of the widespread deterioration in the

markets for securitised and structured financial

assets and consequent disruption to the global

financial system which began in mid-2007, the

markets for these assets have remained illiquid and

it has remained difficult to observe prices for

structured credit risk, including senior tranches of

such risk. The ensuing constraint on the ability of

financial institutions to access wholesale markets to

fund such assets has put additional downward

pressure on asset prices. As a consequence, since

2007 many financial institutions have recorded

considerable reductions in the fair values of asset

values, including their asset-backed securities

(‘ABS’s) and leveraged structured transactions, most

significantly for sub-prime and Alt-A mortgage-

backed securities (‘MBS’s) and collateralised debt

obligations (‘CDO’s) referencing these securities.

A further constraint on liquidity within the

market for securitised assets emerged in 2009 as

rating agencies changed their rating methodologies

in response to changed circumstances, precipitating

widespread downgrades and the fear of further

downgrades across all tranches of securitised paper.

This accentuated illiquidity, particularly for those

institutions subject to the Basel II framework, which

ties capital requirements to external credit ratings

without reference to the actual level of expected loss

on the securities. In light of these issues around

liquidity and the risk to capital from further write-

downs, ratings changes and realised losses and

impairments in 2009, many financial institutions

took steps to reduce leveraged exposures, build their

liquidity and raise additional capital.

Volatility in financial markets, particularly in

the first half of 2009, resulted in wider transaction

spreads, although these narrowed during the second

half of the year. Markets for securitised and

structured financial assets continued to be severely

constrained, and the primary market for all but US

government-sponsored issues remained weak.

Notwithstanding these developments, the severe

deterioration in the fair value of assets supported by

sub-prime and Alt-A mortgages experienced in 2008

began to reverse in 2009 as buyers sought higher

yields in the low interest rate environment. For

example, spreads tightened modestly on Alt-A assets

and sub-prime assets as greater clarity of ultimate

losses emerged.

This section contains disclosures about the

effect of the ongoing market turmoil on HSBC’s

securitisation exposures and other structured

products. HSBC’s principal exposures to the US and

the UK mortgage markets take the form of credit risk

from direct loans and advances to customers which

were originated to be held to maturity or refinancing,

details of which are provided on page 218.

Financial instruments which were most affected

by the market turmoil include those exposures to

direct lending which are held at fair value through

profit or loss, or are classified as available for sale,

which are also held at fair value. Financial

instruments included in these categories comprise

ABSs, including MBSs and CDOs, and exposures to

and contingent claims on monoline insurers

(‘monolines’) in respect of structured credit activities

and leveraged finance transactions which were

originated to be distributed.

In accordance with HSBC’s policy to provide

meaningful disclosures that help investors

and other stakeholders understand the

Group’s performance, financial position and

changes thereto, the information provided in

this section goes beyond the minimum

levels required by accounting standards,

statutory and regulatory requirements and

listing rules.

HSBC has voluntarily adopted the draft British

Bankers’ Association Code on Financial Reporting

Disclosure (‘the draft BBA Code’) for its 2009

Financial Statements. This sets out five disclosure

principles together with supporting guidance. The

principles are that UK banks will:

• provide high quality and meaningful disclosures

useful to decision-making;

• review and enhance their financial instrument

disclosures for key areas of interest;

• assess the applicability and relevance of good

practice recommendations to their disclosures,

acknowledging the importance of such

guidance;

• seek to enhance the comparability of financial

statement disclosures across the UK banking

sector; and

• clearly differentiate in their annual reports

between information that is audited and

information that is unaudited.

In the context of facilitating an understanding

of the ongoing turmoil in markets for securitised and

structured assets and in line with the principles of the

draft BBA Code, HSBC has continued to assess

good practice recommendations issued from time to

time by relevant regulators and standard setters.