HSBC 2009 Annual Report Download - page 276

Download and view the complete annual report

Please find page 276 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

Insurance operations > Financial risks > Market risk

274

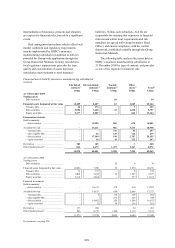

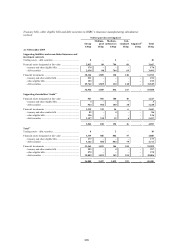

The table demonstrates that for linked contracts,

HSBC typically designates assets at fair value. For

non-linked contracts, the classification of the assets

is driven by the nature of the underlying contract.

The table also shows that approximately

64.4 per cent of financial assets were invested in

debt securities at 31 December 2009 (2008: 62.9 per

cent) with 22.2 per cent (2008: 19.7 per cent)

invested in equity securities.

In life linked insurance, premium income less

charges levied is invested in a portfolio of assets.

HSBC manages the financial risks of this product on

behalf of the policyholders by holding appropriate

assets in segregated funds or portfolios to which the

liabilities are linked. Typically, HSBC retains some

exposure to market risk as the market value of the

linked assets influences the fees charged by HSBC

and thereby affects the recoverability of expenses

incurred by the Group in managing the product. The

assets held to support life linked liabilities

represented 22.4 per cent of the total financial assets

of HSBC’s insurance manufacturing subsidiaries at

the end of 2009 (2008: 19.4 per cent).

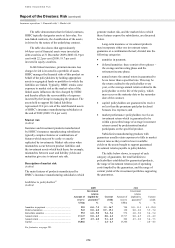

Market risk

(Audited)

Insurance and investment products manufactured

by HSBC’s insurance manufacturing subsidiaries

typically comprise features or combinations of

features which may not be easily or exactly

replicated by investments. Market risk arises when

mismatches occur between product liabilities and

the investment assets which back them; for example,

mismatches between asset and liability yields and

maturities give rise to interest rate risk.

Description of market risk

(Audited)

The main features of products manufactured by

HSBC’s insurance manufacturing subsidiaries which

generate market risk, and the market risk to which

these features expose the subsidiaries, are discussed

below.

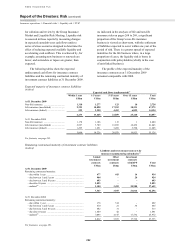

Long-term insurance or investment products

may incorporate either one investment return

guarantee or a combination thereof, divided into the

following categories:

• annuities in payment;

• deferred annuities: these consist of two phases –

the savings and investing phase and the

retirement income phase;

• annual return: the annual return is guaranteed to

be no lower than a specified rate. This may be

the return credited to the policyholder every

year, or the average annual return credited to the

policyholder over the life of the policy, which

may occur on the maturity date or the surrender

date of the contract;

• capital: policyholders are guaranteed to receive

no less than the premiums paid plus declared

bonuses less expenses; and

• market performance: policyholders receive an

investment return which is guaranteed to be

within a prescribed range of average investment

returns earned by predetermined market

participants on the specified product.

Subsidiaries manufacturing products with

guarantees usually retain exposures to falls in market

interest rates as they result in lower available

yields on the assets bought to support guaranteed

investment returns payable to policyholders.

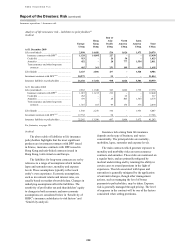

The table below shows, in respect of each

category of guarantee, the total liabilities to

policyholders established for guaranteed products,

the range of investment returns (net of operating

costs) implied by the guarantees, and the range of

current yields of the investment portfolios supporting

the guarantees.

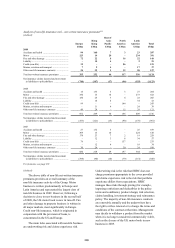

Liabilities to policyholders62

(Audited)

2009 2008

Amount of

reserve

Investment

returns

implied by

guarantee63

Current

yields

Amount of

reserve

Investment

returns

implied by

guarantee63

Current

yields

US$m % % US$m % %

Annuities in payment .......................................... 925 0.0 – 7.5 1.3 – 16.7 744 0.0 – 11.5 6.5 – 28.0

Deferred annuities ............................................... 943 0.0 – 6.0 0.9 – 15.1 120 0.0 – 6.0 3.9 – 7.4

Immediate annuities ............................................ 553 6.0 – 9.0 5.4 – 5.4 576 6.0 – 9.0 5.4 – 5.4

Annual return ...................................................... 17,147 0.0 – 4.5 0.8 – 6.2 13,717 0.0 – 4.5 2.2 – 4.9

Annual return ...................................................... 497 4.5 – 6.0 5.1 – 6.5 302 4.5 – 6.0 3.4 – 7.3

Capital ................................................................. 15,866 – 2.4 – 4.3 13,346 – 2.0 – 4.3

For footnotes, see page 291.