HSBC 2009 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

189

Securitisations

HSBC uses SPEs to securitise customer loans and

advances that it has originated, mainly in order to

diversify its sources of funding for asset origination

and for capital efficiency purposes. In such cases, the

loans and advances are transferred by HSBC to the

SPEs for cash, and the SPEs issue debt securities

to investors to fund the cash purchases. Credit

enhancements to the underlying assets may be used

to obtain investment grade ratings on the senior debt

issued by the SPEs. HSBC has also established

securitisation programmes in the US and Germany

where loans originated by third parties are

securitised. Most of these vehicles are not

consolidated by HSBC as it is not exposed to the

majority of risks and rewards of ownership in the

SPEs. In 2009, demand for the securitised products

remained low.

In addition, HSBC uses SPEs to mitigate the

capital absorbed by some of the customer loans and

advances it has originated. Credit derivatives are

used to transfer the credit risk associated with such

customer loans and advances to an SPE, using

securitisations commonly known as synthetic

securitisations. These SPEs are consolidated when

HSBC is exposed to the majority of risks and

rewards of ownership.

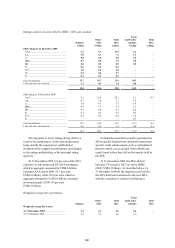

Total assets of HSBC’s securitisations which are on-

balance sheet, by balance sheet classification

At 31 December

2009 2008

US$bn US$bn

Trading assets ............................ 0.9 1.3

Loans and advances to customers 35.4 50.8

Other assets ................................ 1.4 1.1

Derivatives ................................. 1.2 1.4

38.9 54.6

These assets include US$0.9 billion (2008:

US$1.3 billion) of exposure to US sub-prime

mortgages.

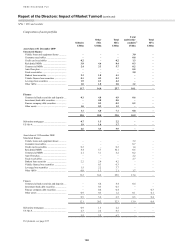

Total assets of HSBC’s securitisations which are

off-balance sheet

2009 2008

US$bn US$bn

HSBC originated assets .............. 0.6 0.6

Non-HSBC originated assets:

– term securitisation

programmes ......................... 10.5 13.5

11.1 14.1

HSBC’s financial investments in off-balance

sheet securitisations at 31 December 2009 amounted

to US$0.1 billion (2008: US$0.2 billion). These

assets include assets which are classified as

available-for-sale securities and measured at fair

value, and have been securitised by HSBC under

arrangements by which HSBC retains a continuing

involvement in them. Further details are provided in

Note 20 on the Financial Statements.

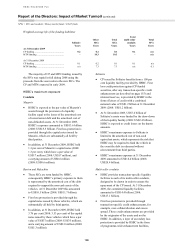

HSBC’s maximum exposure

The maximum exposure is the aggregate of any

holdings of notes issued by these vehicles and the

reserve account positions intended to provide credit

support under certain pre-defined circumstances to

senior note holders. HSBC is not obligated to

provide further funding. At 31 December 2009,

HSBC’s maximum exposure to consolidated and

unconsolidated securitisations amounted to

US$8.0 billion (2008: US$8.0 billion).

Other

HSBC also establishes SPEs in the normal course

of business for a number of purposes, for example,

structured credit transactions for customers to

provide finance to public and private sector

infrastructure projects, and for asset and structured

finance (‘ASF’) transactions.

Structured credit transactions

HSBC provides structured credit transactions to

third-party professional and institutional investors

who wish to obtain exposure, sometimes on a

leveraged basis, to a reference portfolio of debt

instruments. In such structures, the investor receives

returns referenced to the underlying portfolio by

purchasing notes issued by the SPEs. HSBC enters

into contracts with the SPEs, generally in the form of

derivatives, in order to pass the required risks and

rewards of the reference portfolios to the SPEs.

HSBC’s risk in relation to the derivative contracts

with the SPEs is managed within HSBC’s trading

market risk framework (see ‘Market risk’ on

page 250).

In certain transactions HSBC is exposed to risk

often referred to as gap risk. Gap risk typically arises

in transactions where the aggregate potential claims

against the SPE by HSBC pursuant to one or more

derivatives could be greater than the value of the

collateral held by the SPE and securing such

derivatives. HSBC often mitigates such gap risk by

incorporating in the SPE transaction features which