HSBC 2009 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Geographical regions > Latin America > 2008

140

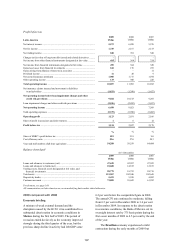

2008 compared with 2007

Economic briefing

Inflationary pressures developed in Mexico during

the course of 2008, mostly due to rising commodity

prices, as consumer price inflation accelerated from

3.7 per cent in January to 6.5 per cent by the year-

end. In response, the Bank of Mexico raised its

overnight interest rate by 75 basis points to 8.25 per

cent by the end of the year, although a variety of

economic indicators pointed to a sharp loss of

momentum during the final quarter as global growth

slowed.

The Brazilian economy performed strongly

during the first half of 2008, driven by domestic

demand, with the annual rate of consumer price

inflation rising from 4.6 per cent in January to

6.4 per cent in July, towards the upper limit of the

central banks’ tolerance range. Conditions within

the labour market improved, with the rate of

unemployment well below levels observed a year

earlier. In line with many other economies within the

region, however, conditions weakened markedly

towards the end of 2008, with industrial production

falling by close to 20 per cent during the fourth

quarter.

In Argentina, economic activity held at a

reasonably robust level for much of the year,

although measures of industrial production growth

slowed noticeably during the final months of 2008.

Declines in commodity prices during the second half

of 2008 and the reduced value of exports raised

concerns over the level of capital outflow from the

country, while domestic currency interest rates

increased sharply. The official headline rate of

consumer price inflation rose during the first half of

2008, reaching 9.3 per cent in June 2008 before

slowing to 7.2 per cent in December, although

methodological changes make comparisons over

year difficult.

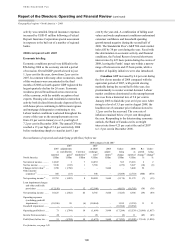

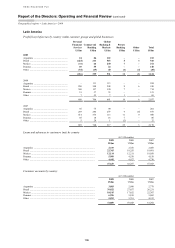

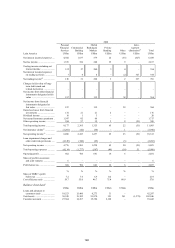

Reconciliation of reported and underlying profit before tax

2008 compared with 2007

Latin America

2007

as

reported

US$m

2007

acquisitions,

disposals

& dilution

gains10

US$m

Currency

translation11

US$m

2007

at 2008

exchange

rates17

US$m

2008

acquisitions

and

disposals10

US$m

Under-

lying

change

US$m

2008

as

reported

US$m

Re-

ported

change13

%

Under-

lying

change13

%

Net interest income .......... 5,576 – 155 5,731 – 727 6,458 16 13

Net fee income ................. 2,153 – 58 2,211 – (44) 2,167 1 (2)

Other income15 ................. 1,536 (11) 23 1,548 71 269 1,888 23 17

Net operating income16 .... 9,265 (11) 236 9,490 71 952 10,513 13 10

Loan impairment charges

and other credit risk

provisions .................... (1,697) – (64) (1,761) – (731) (2,492) (47) (42)

Net operating income ...... 7,568 (11) 172 7,729 71 221 8,021 6 3

Operating expenses .......... (5,402) – (190) (5,592) – (398) (5,990) (11) (7)

Operating profit ............... 2,166 (11) (18) 2,137 71 (177) 2,031 (6) (8)

Income from associates ... 12 – – 12 – (6) 6 (50) (50)

Profit before tax ............... 2,178 (11) (18) 2,149 71 (183) 2,037 (6) (9)

For footnotes, see page 149.

Review of business performance

In Latin America, HSBC reported a pre-tax profit

of US$2.0 billion compared with US$2.2 billion in

2007, a decrease of 6 per cent. On an underlying

basis, pre-tax profits decreased by 9 per cent as

increased revenues were offset by higher loan

impairment charges, largely in Mexico and Brazil,

and increased operating costs across the region.

Net interest income increased by 13 per cent.

Growth in average personal lending volumes was

mainly driven by vehicle finance and payroll loans

in Brazil, and credit cards and personal loans in

Mexico. Average credit card balances increased as a

result of significant organic growth in 2007 which

was not repeated in 2008. Commercial loan volume

growth was driven by increased lending for working

capital and trade finance loans in Brazil, and

medium-sized businesses and the real estate sector in

Mexico. Increased income on customer liabilities,

which was driven by volume growth, particularly in

time deposits, was largely offset by a contraction in

deposit spreads, primarily on US dollar denominated

accounts. Active repricing strategies were deployed