HSBC 2009 Annual Report Download - page 243

Download and view the complete annual report

Please find page 243 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

241

Impaired loans increased by 37 per cent to

US$2.3 billion at 31 December 2008.

The most significant increase was in Mexico,

reflecting higher impairment charges in the credit

card portfolio due to a combination of higher

average balances from organic expansion and

growing delinquency rates driven by a deterioration

in credit quality as the 2006 and 2007 vintages

continued to season and move into later stages of

delinquency. Management action to improve the

quality of new business included tightened

underwriting, enhanced collection strategies and

better managed customer acquisition channels. The

commercial portfolio in Mexico also experienced

higher impairment charges due to credit quality

deterioration among small and medium sized

enterprises as the economy weakened. In Brazil,

higher impairment charges were driven by a

combination of balance growth and credit quality

deterioration in the vehicle finance and payroll loan

portfolios.

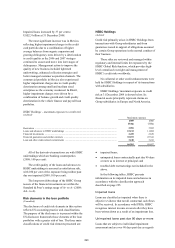

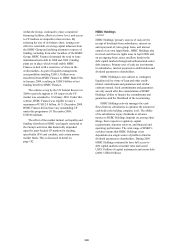

HSBC Holdings

(Audited)

Credit risk primarily arises in HSBC Holdings from

transactions with Group subsidiaries and from

guarantees issued in support of obligations assumed

by certain Group operations in the normal conduct of

their business.

These risks are reviewed and managed within

regulatory and internal limits for exposures by the

HSBC Global Risk function, which provides high-

level centralised oversight and management of

HSBC’s credit risks worldwide.

No collateral or other credit enhancements were

held by HSBC Holdings in respect of its transactions

with subsidiaries.

HSBC Holdings’ maximum exposure to credit

risk at 31 December 2009 is shown below. Its

financial assets principally represent claims on

Group subsidiaries in Europe and North America.

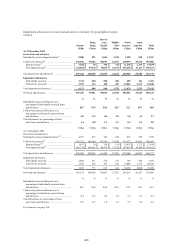

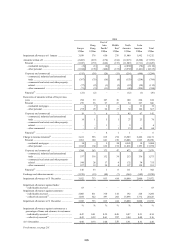

HSBC Holdings – maximum exposure to credit risk

(Audited)

Maximum exposure

2009 2008

US$m US$m

Derivatives ............................................................................................................................................ 2,981 3,682

Loans and advances to HSBC undertakings ........................................................................................ 23,212 11,804

Financial investments ........................................................................................................................... 2,455 2,629

Financial guarantees and similar contracts .......................................................................................... 35,073 47,341

Loan and other credit-related commitments ........................................................................................ 3,240 3,241

66,961 68,697

All of the derivative transactions are with HSBC

undertakings which are banking counterparties

(2008: 100 per cent).

The credit quality of the loans and advances to

HSBC undertakings is assessed as satisfactory risk,

with 100 per cent of the exposure being neither past

due nor impaired (2008: 100 per cent).

The long-term debt ratings of the HSBC Group

issuers of the financial investments are within the

Standard & Poor’s ratings range of A+ to A– (2008:

AA– to A).

Risk elements in the loan portfolio

(Unaudited)

The disclosure of credit risk elements in this section

reflects US accounting practice and classifications.

The purpose of the disclosure is to present within the

US disclosure framework those elements of the loan

portfolios with a greater risk of loss. The three main

classifications of credit risk elements presented are:

• impaired loans;

• unimpaired loans contractually past due 90 days

or more as to interest or principal; and

• troubled debt restructurings not included in the

above.

In the following tables, HSBC presents

information on its impaired loans and advances in

accordance with the classification approach

described on page 225.

Impaired loans

Loans are classified as impaired when there is

objective evidence that not all contractual cash flows

will be received. In accordance with IFRSs, HSBC

recognises interest income on assets after they have

been written down as a result of an impairment loss.

Unimpaired loans past due 90 days or more

Loans that are subject to individual impairment

assessment and are over 90 days past due as regards