HSBC 2009 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

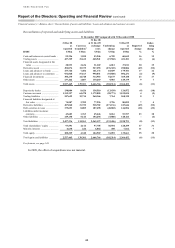

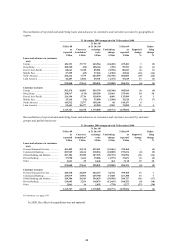

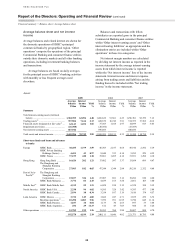

HSBC HOLDINGS PLC

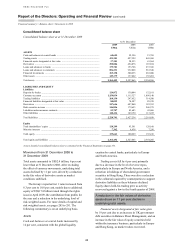

Report of the Directors: Operating and Financial Review (continued)

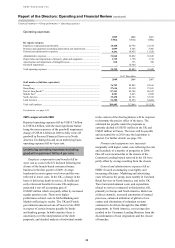

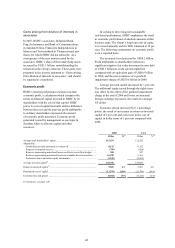

Financial summary > Group performance > Loan impairment charges

36

impairment charges in the real estate secured

portfolio. Loan impairment charges in the Card

and Retail Services portfolio decreased despite

the state of the US economy and higher levels of

unemployment and personal bankruptcy. The main

reason was the decline in card balances following

actions taken to manage risk beginning in the fourth

quarter of 2007 and continuing through 2009, and

stable credit conditions.

In HSBC Bank USA, increased loan impairment

charges in the personal lending portfolios were due

to additional delinquencies which resulted in

increased write-offs in the prime first lien mortgage

loan portfolios as house prices continued to

deteriorate in certain markets.

Loan impairment charges and other credit risk

provisions increased significantly in Global Banking

and Markets. Loan impairment charges increased,

reflecting the impairment of a small number of

exposures in the financial and property sectors in

Europe and the Middle East. Further impairments

were also recognised in respect of certain asset-

backed securities held in the available-for-sale

portfolio, reflecting mark-to-market losses which

HSBC judged to be significantly in excess of the

likely ultimate cash losses.

Loan impairment charges declined in

Personal Financial Services in the US but

rose in Commercial Banking outside Hong

Kong and in Global Banking and Markets.

In the UK, loan impairment charges rose in both

the Commercial Banking and Personal Financial

Services portfolios. However, despite the contraction

in the economy, charges remained a low proportion

of the portfolio. In Commercial Banking, loan

impairment charges largely reflected economic

weakness in a broad range of sectors.

In UK Personal Financial Services, loan

impairment charges also increased as unemployment

rose. This was seen primarily in the credit card and

unsecured personal loan portfolios. In the residential

mortgage portfolios, delinquency rates decreased

as HSBC continued to benefit from very limited

exposure to buy-to-let and self-certified mortgages.

HSBC’s mortgage exposure continued to be well

secured, with an average loan-to-value ratio for new

UK business in HSBC Bank’s mortgage portfolio,

excluding First Direct, of under 55 per cent in 2009,

compared with 59 per cent in 2008.

In the Middle East, loan impairment charges

increased markedly from US$280 million to

US$1.3 billion as the region experienced a

significant economic contraction in activity,

predominantly in real estate and construction,

which particularly affected the UAE. Commercial

Banking recorded a number of specific loan

impairment charges and a significant increase

in collective loan impairment charges. Lower

employment in the region, largely driven by the

decline in construction activity, led to a rise in loan

impairment charges in Personal Financial Services,

particularly in the credit card and personal lending

portfolios.

In Latin America, portfolios were affected by

the weaker economic environment for much of

the year. In Personal Financial Services, loan

impairment charges rose by 12 per cent to

US$2.0 billion, with increased delinquencies in

credit cards, mortgages, vehicle finance and payroll

loans due to higher unemployment. In the Brazilian

Commercial Banking portfolios, higher

delinquencies were experienced primarily in the

business banking and mid-market segments. In

Mexico, action taken in 2008 to curtail originations

and increase collection resources held loan

impairment charges broadly unchanged

notwithstanding the deterioration in the economy

and the impact of the H1N1 virus.

In India, as in Mexico, curtailment of

origination activity in unsecured personal lending

slowed the increase in loan impairment charges in

the unsecured credit card and personal lending

portfolios in Personal Financial Services. In

Commercial Banking, a higher number of corporate

failures including a number of fraud-related losses,

led to increased loan impairment charges.

Loan impairment charges and other credit risk

provisions in Hong Kong decreased by 35 per cent to

US$500 million as the economic environment

improved in 2009, credit conditions recovered and

international trade volumes improved.

In Private Banking, loan impairment charges

increased from a very low level, largely attributable

to a specific charge relating to a single client

relationship in the US.

2008 compared with 2007

Reported loan impairment charges and other credit

risk provisions were US$24.9 billion in 2008, an

increase of 45 per cent over 2007, 46 per cent on an

underlying basis.

A deterioration in credit quality was

experienced across all customer groups and

geographical regions as the global economy slowed.

The rise in Group loan impairment charges and other

credit risk provisions also reflected an underlying