HSBC 2009 Annual Report Download - page 258

Download and view the complete annual report

Please find page 258 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

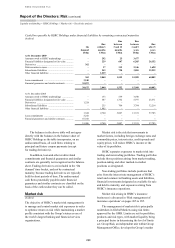

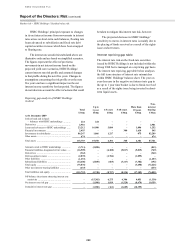

Market risk > Sensitivity of NII / Structural FX exposure

256

‘Summary of significant accounting policies’ on

page 369.

Sensitivity of net interest income

(Unaudited)

A principal part of HSBC’s management of market

risk in non-trading portfolios is to monitor the

sensitivity of projected net interest income under

varying interest rate scenarios (simulation

modelling). HSBC aims, through its management of

market risk in non-trading portfolios, to mitigate the

effect of prospective interest rate movements which

could reduce future net interest income, while

balancing the cost of such hedging activities on the

current net revenue stream.

For simulation modelling, businesses use a

combination of scenarios relevant to local businesses

and local markets and standard scenarios which are

required throughout HSBC. The standard scenarios

are consolidated to illustrate the combined pro forma

effect on HSBC’s consolidated portfolio valuations

and net interest income.

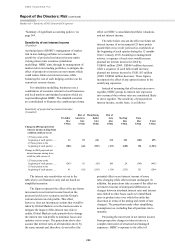

The table below sets out the effect on future net

interest income of an incremental 25 basis points

parallel fall or rise in all yield curves worldwide at

the beginning of each quarter during the 12 months

from 1 January 2010. Assuming no management

actions, a sequence of such rises would increase

planned net interest income for 2010 by

US$695 million (2009: US$463 million decrease),

while a sequence of such falls would decrease

planned net interest income by US$1,563 million

(2009: US$284 million decrease). These figures

incorporate the effect of any option features in the

underlying exposures.

Instead of assuming that all interest rates move

together, HSBC groups its interest rate exposures

into currency blocs whose rates are considered likely

to move together. The sensitivity of projected net

interest income, on this basis, is as follows:

Sensitivity of projected net interest income

(Unaudited)

US dollar

bloc

US$m

Rest of

Americas

bloc

US$m

Hong Kong

dollar

bloc

US$m

Rest of

Asia

bloc

US$m

Sterling

bloc

US$m

Euro

bloc

US$m

Total

US$m

Change in 2010 projected net

interest income arising from

a shift in yield curves of:

+25 basis points at the

beginning of each quarter ..... 13 92 416 112 363 (301) 695

–25 basis points at the

beginning of each quarter ..... (382) (46) (507) (133) (689) 194 (1,563)

Change in 2009 projected net

interest income arising from

a shift in yield curves of:

+25 basis points at the

beginning of each quarter ..... (243) 42 (45) 100 28 (345) (463)

–25 basis points at the

beginning of each quarter ..... 41 (42) (285) (114) (235) 351 (284)

The interest rate sensitivities set out in the

table above are illustrative only and are based on

simplified scenarios.

The figures represent the effect of the pro forma

movements in net interest income based on the

projected yield curve scenarios and the Group’s

current interest rate risk profile. This effect,

however, does not incorporate actions that would be

taken by Global Markets or in the business units to

mitigate the impact of this interest rate risk; in

reality, Global Markets seeks proactively to change

the interest rate risk profile to minimise losses and

optimise net revenues. The projections above also

assume that interest rates of all maturities move by

the same amount and, therefore, do not reflect the

potential effect on net interest income of some

rates changing while others remain unchanged. In

addition, the projections take account of the effect on

net interest income of anticipated differences in

changes between interbank interest rates and interest

rates linked to other bases (such as Central Bank

rates or product rates over which the entity has

discretion in terms of the timing and extent of rate

changes). The projections make other simplifying

assumptions too, including that all positions run to

maturity.

Projecting the movement in net interest income

from prospective changes in interest rates is a

complex interaction of structural and managed

exposures. HSBC’s exposure to the effect of