HSBC 2009 Annual Report Download - page 211

Download and view the complete annual report

Please find page 211 of the 2009 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

|

|

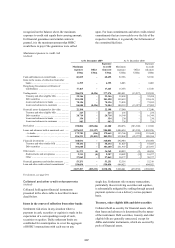

209

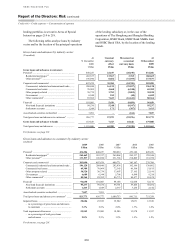

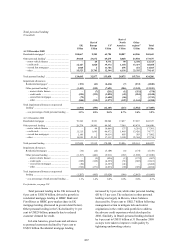

US$143 billion, 56 per cent). This included

US$22 billion (2008: US$32 billion) of treasury

and other eligible bills. Corporate debt and other

securities were US$84 billion or 32 per cent of

overall trading securities, in line with 2008’s level of

US$83 billion. Included within total securities

held for trading were US$41 billion (2008:

US$50 billion) of debt securities issued by banks

and other financial institutions.

A more detailed analysis of securities held for

trading is set out in Note 16 on the Financial

Statements and an analysis of credit quality is

provided on page 225.

Debt securities, treasury and other eligible bills

(Unaudited)

At US$360 billion, total financial investments

excluding equity securities were 23 per cent higher

at 31 December 2009 than at the end of 2008. Debt

securities, at US$302 billion, represented the largest

concentration of financial investments at 84 per cent

of the total, compared with US$252 billion (86 per

cent) at 31 December 2008. HSBC’s holdings of

corporate debt, ABSs and other securities were

spread across a wide range of issuers and

geographical regions, with 37 per cent invested in

securities issued by banks and other financial

institutions. In total, holdings in ABSs decreased by

US$8 billion due to a combination of movements in

fair values, principal amortisations and write-downs.

Total financial investments excluding equity

securities increased by 23 per cent to

US$360 billion in 2009.

Investments in securities of governments and

government agencies of US$171 billion were 46 per

cent of overall financial investments, 8 percentage

points higher than in 2008. US$58 billion of these

investments comprised treasury and other eligible

bills.

A more detailed analysis of financial

investments is set out in Note 19 on the Financial

Statements and an analysis by credit quality is

provided on page 225.

The insurance businesses held diversified

portfolios of debt and equity securities designated

at fair value (2009: US$25 billion; 2008:

US$20 billion) and debt securities classified as

financial investments (2009: US$35 billion; 2008:

US$28 billion). A more detailed analysis of

securities held by the insurance businesses is set

out on page 273.

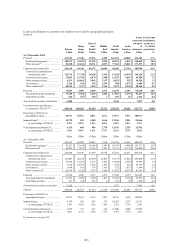

Derivatives

(Unaudited)

Derivative assets at 31 December 2009 were

US$251 billion, a decline of 49 per cent from

31 December 2008, primarily in foreign exchange,

interest rate and credit derivatives. The main drivers

of the reduction were fair value movements across

the entire portfolio arising from lower levels of

volatility within the financial markets, steepening

yield curves and narrowing credit spreads.

Exposure to derivative assets fell by 49 per

cent in 2009 to US$251 billion.

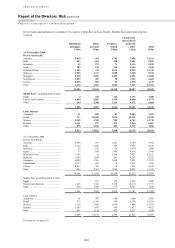

Loans and advances

(Unaudited)

At constant exchange rates, gross loans and advances

to customers (excluding the financial sector) at

31 December 2009 declined by US$83 billion or

9 per cent from 31 December 2008.

Personal lending represented 47 per cent of

total gross loans and advances to customers.

Residential mortgages of US$261 billion represented

28 per cent of total gross advances to customers and

constituted the Group’s largest concentration in

a single exposure type. As a result of continued

run-off in the US consumer finance exit portfolios,

personal lending within North America fell to be

broadly in line with European exposure.

Corporate, commercial and financial lending,

including settlement accounts, amounted to 52 per

cent of total gross loans and advances to customers

at 31 December 2009. The largest industry

concentrations were to non-bank financial

institutions and commercial real estate lending at

10 per cent and 8 per cent, respectively, of total

gross lending to customers.

Exposure to non-bank financial institutions

principally comprised secured lending on trading

accounts, primarily through repo facilities.

Commercial, industrial and international trade

lending declined moderately in 2009, falling as a

proportion of total lending by a single percentage

point to 21 per cent of total gross loans and advances

to customers. Within this category, the largest

concentration of lending was to the service sector,

which amounted to 6 per cent of total gross lending

to customers.

Loans and advances to banks were widely

distributed across major institutions in 2009.

Further discussion of significant movements in

credit quality of the personal lending and wholesale