EasyJet 2013 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2013 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

www.easyJet.com 91

Governance

Independent Auditors’ report

to the members of easyJet plc

REPORT ON THE ACCOUNTS

Our opinion

In our opinion:

• the accounts, defined below, give a true and fair

view of the state of the Group’s and of the

Company’s affairs as at 30 September 2013 and

of the Group’s profit and of the Group’s and

Company’s cash flows for the year then ended;

• the Group accounts have been properly prepared

in accordance with International Financial

Reporting Standards (IFRSs) as adopted by the

European Union;

• the Company accounts have been properly

prepared in accordance with IFRSs as adopted by

the European Union and as applied in accordance

with the provisions of the Companies Act 2006; and

• the accounts have been prepared in accordance

with the requirements of the Companies Act

2006 and, as regards the Group accounts, Article

4 of the IAS Regulation.

This opinion is to be read in the context of what we

say below.

What we have audited

The Group accounts and Company accounts

(the “accounts”), which are prepared by

easyJet plc, comprise:

• the Group consolidated and Company statements

of financial position as at 30 September 2013;

• the Group consolidated income statement and

consolidated statement of comprehensive

income for the year then ended;

• the Group consolidated and Company

statements of changes in equity and statements

of cash flows for the year then ended; and

• the notes to the accounts, which include a

summary of significant accounting policies and

other explanatory information.

The financial reporting framework that has been

applied in their preparation comprises applicable law

and IFRSs as adopted by the European Union and,

as regards the Company, as applied in accordance

with the provisions of the Companies Act 2006.

What an audit of accounts involves

We conducted our audit in accordance with

International Standards on Auditing (UK and Ireland)

(‘ISAs (UK & Ireland)’). An audit involves obtaining

evidence about the amounts and disclosures in the

accounts sufficient to give reasonable assurance

that the accounts are free from material

misstatement, whether caused by fraud or error.

This includes an assessment of:

• whether the accounting policies are appropriate

to the Group’s and Company’s circumstances

and have been consistently applied and

adequately disclosed;

• the reasonableness of significant accounting

estimates made by the Directors; and

• the overall presentation of the accounts.

In addition, we read all the financial and non-financial

information in the Annual Report to identify material

inconsistencies with the audited accounts and to

identify any information that is apparently materially

incorrect based on, or materially inconsistent with,

the knowledge acquired by us in the course of

performing the audit. If we become aware of any

apparent material misstatements or inconsistencies

we consider the implications for our report.

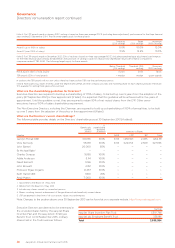

Overview of our audit approach

Materiality

We set certain thresholds for materiality. These

helped us to determine the nature, timing and

extent of our audit procedures and to evaluate the

effect of misstatements, both individually and on

the accounts as a whole.

Based on our professional judgement, we determined

materiality for the Group accounts as a whole to be

£23 million.

We agreed with the Audit Committee that we

would report to them misstatements identified

during our audit above £1 million as well as

misstatements below that amount that, in our

view, warranted reporting for qualitative reasons.

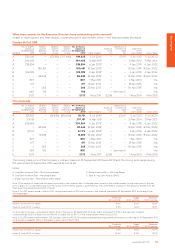

Overview of the scope of our audit

The Group operates through four trading subsidiary

undertakings as set out on page 129 and the

Group’s accounts are a consolidation of these

entities. In establishing the overall approach to

the Group audit we determined the type of work

that needed to be performed in respect of each

subsidiary; which comprised an audit of their

complete financial information. These procedures

gave us the evidence that we needed for our

opinion on the Group’s accounts as a whole.

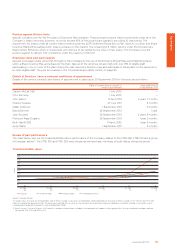

Areas of particular audit focus

In preparing the accounts, the Directors made a

number of subjective judgements, for example in

respect of significant accounting estimates that

involved making assumptions and considering

future events that are inherently uncertain. We

primarily focused our work in these areas by

assessing the Directors’ judgements against

available evidence, forming our own judgements,

and evaluating the disclosures in the accounts.

In our audit, we tested and examined information,

using sampling and other auditing techniques, to

the extent we considered necessary to provide

a reasonable basis for us to draw conclusions.

We obtained audit evidence through testing the

effectiveness of controls, substantive procedures

or a combination of both.

We considered the following areas to be those that

required particular focus in the current year. This is not

a complete list of all risks or areas of focus identified

by our audit. We discussed these areas of focus with

the Audit Committee. Their report on those matters

that they considered to be significant issues in relation

to the accounts is set out on page 71.