Cisco 2010 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2010 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

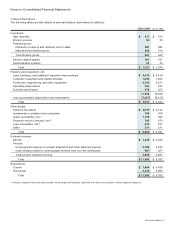

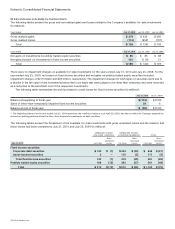

Notes to Consolidated Financial Statements

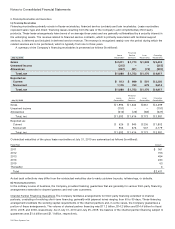

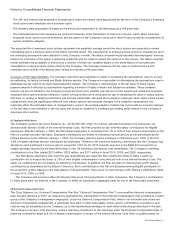

The Company enters into foreign exchange forward and option contracts to reduce the short-term effects of foreign currency

fluctuations on assets and liabilities such as foreign currency receivables, including long-term customer financings, investments, and

payables. These derivatives are not designated as hedging instruments. Gains and losses on the contracts are included in other

income (loss), net, and substantially offset foreign exchange gains and losses from the remeasurement of intercompany balances or

other current assets, investments, or liabilities denominated in currencies other than the functional currency of the reporting entity.

The Company hedges certain net investments in its foreign subsidiaries with forward contracts, which generally have maturities

of up to six months. The Company recognized a loss of $2 million in OCI for the effective portion of its net investment hedges for

the year ended July 31, 2010. The Company’s net investment hedges are not included in the preceding tables.

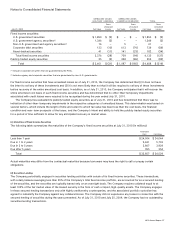

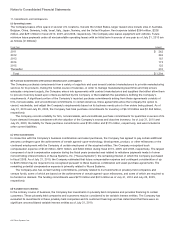

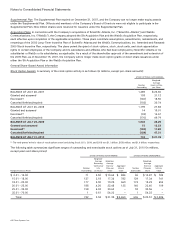

The notional amounts of the Company’s foreign currency derivatives are summarized as follows (in millions):

July 31, 2010 July 25, 2009

Cash flow hedging instruments $ 2,611 $ 2,965

No hedge designation 4,619 4,423

Net investment hedging instruments 105 103

Total $ 7,335 $ 7,491

(c) Interest Rate Risk

Interest Rate Derivatives, Investments The Company’s primary objective for holding fixed income securities is to achieve an

appropriate investment return consistent with preserving principal and managing risk. To realize these objectives, the Company

may utilize interest rate swaps or other derivatives designated as fair value or cash flow hedges. As of July 31, 2010 and July 25,

2009 the Company did not have any outstanding interest rate derivatives related to its fixed income securities.

Interest Rate Derivatives Designated as Cash Flow Hedge, Long-Term Debt In fiscal 2010 and 2009, the Company entered into

contracts related to interest rate derivatives designated as cash flow hedges, with an aggregate notional amount of $3.7 billion and

$3.9 billion, respectively, to hedge against interest rate movements in connection with its anticipated issuance of senior notes in

each of those fiscal years. These derivative instruments were settled in connection with the actual issuance of the senior notes. The

effective portion of these hedges was recorded to AOCI, net of tax, and is being amortized to interest expense over the respective

lives of the notes.

Interest Rate Derivatives Designated as Fair Value Hedge, Long-Term Debt In fiscal 2010, the Company entered into interest rate

swaps with a $1.5 billion notional amount designated as fair value hedges of a portion of the 2016 Notes. Under these interest rate

swaps, the Company receives fixed-rate interest payments and makes interest payments based on LIBOR plus a fixed number of

basis points. The effect of these swaps is to convert fixed-rate interest expense on a portion of the 2016 Notes to a floating rate

interest expense. The gains and losses related to changes in the fair value of the interest rate swaps are included in interest

expense and substantially offset changes in the fair value of the hedged portion of the underlying hedged debt. The fair value of the

interest rate swaps was $72 million as of July 31, 2010 and was reflected in other assets. The Company did not have any interest

rate swaps outstanding at July 25, 2009.

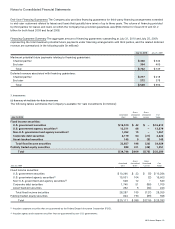

(d) Equity Price Risk

The Company may hold equity securities for strategic purposes or to diversify its overall investment portfolio. The publicly traded

equity securities in the Company’s portfolio are subject to price risk. To manage its exposure to changes in the fair value of certain

equity securities, the Company may enter into equity derivatives that are designated as fair value or cash flow hedges. The changes

in the value of the hedging instruments are included in other income (loss), net, and offset the change in the fair value of the

underlying hedged investment. The Company did not have any equity derivatives outstanding at July 31, 2010 and July 25, 2009.

In addition, the Company periodically manages the risk of its investment portfolio by entering into equity derivatives that are not

designated as accounting hedges. The changes in the fair value of these derivatives were also included in other income (loss), net.

The Company is also exposed to variability in compensation charges related to certain deferred compensation obligations to

employees. Although not designated as accounting hedges, the Company utilizes equity derivatives to economically hedge this

exposure. As of July 31, 2010 and July 25, 2009, the notional amount of the derivative instruments used to hedge such

liabilities was $169 million and $91 million, respectively.

(e) Credit-Risk-Related Contingent Features

Certain derivative instruments are executed under agreements that have provisions requiring the Company and counterparty to

maintain a specified credit rating from certain credit rating agencies. If the Company’s or counterparty’s credit rating falls below a

specified credit rating, either party has the right to request collateral on the derivatives’ net liability position. Such provisions did not

affect the Company’s financial position as of July 31, 2010 and July 25, 2009.

2010 Annual Report 63