Cisco 2010 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2010 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

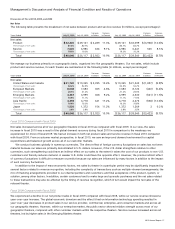

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Share-Based Compensation Expense

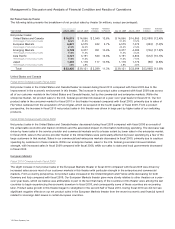

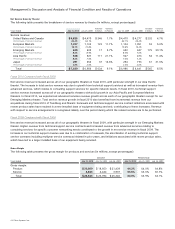

Share-based compensation expense is presented as follows (in millions):

Years Ended July 31, 2010 July 25, 2009 July 26, 2008

Share-based compensation expense $ 1,517 $ 1,231 $ 1,112

The determination of fair value of share-based payment awards on the date of grant using an option-pricing model is affected by

our stock price as well as assumptions regarding a number of highly complex and subjective variables. For employee stock options

and employee stock purchase rights, these variables include, but are not limited to, the expected stock price volatility over the term

of the awards, risk-free interest rate and expected dividends as of the grant date. For employee stock options, we used the implied

volatility for two-year traded options on our stock as the expected volatility assumption required in the lattice-binomial model. For

employee stock purchase rights, we used the implied volatility for traded options (with lives corresponding to the expected life of

the employee stock purchase rights) on our stock. The selection of the implied volatility approach was based upon the availability of

actively traded options on our stock and our assessment that implied volatility is more representative of future stock price trends

than historical volatility. The valuation of employee stock options is also impacted by kurtosis, and skewness, which are technical

measures of the distribution of stock price returns, and the actual and projected employee stock option exercise behaviors. See

Note 13 to the Consolidated Financial Statements.

Because share-based compensation expense is based on awards ultimately expected to vest, it has been reduced for

forfeitures. If factors change and we employ different assumptions in the application of our option-pricing model in future periods

or if we experience different forfeiture rates, the compensation expense that is derived may differ significantly from what we have

recorded in the current year.

Fair Value Measurements of Investments

Our fixed income and publicly traded equity securities, collectively, are reflected in the Consolidated Balance Sheets at a fair value

of $35.3 billion as of July 31, 2010, compared with $29.3 billion as of July 25, 2009. Our fixed income investment portfolio, as of

July 31, 2010, consisted primarily of the highest quality investment grade securities. See Note 7 to the Consolidated Financial

Statements.

As described more fully in Note 8 to the Consolidated Financial Statements, the valuation hierarchy is based on the level of

independent, objective evidence available regarding the value of the investments. It encompasses three classes of investments:

Level 1 consists of securities for which there are quoted prices in active markets for identical securities; Level 2 consists of

securities for which observable inputs other than Level 1 inputs are used, such as prices for similar securities in active markets or

for identical securities in less active markets and model-derived valuations for which the variables are derived from, or

corroborated by, observable market data; and Level 3 consists of securities for which there are unobservable inputs to the valuation

methodology that are significant to the measurement of the fair value.

Our Level 2 securities are valued using quoted market prices for similar instruments, nonbinding market prices that are

corroborated by observable market data, or discounted cash flow techniques in limited circumstances. We use inputs such as

actual trade data, benchmark yields, broker/dealer quotes, and other similar data, which are obtained from independent pricing

vendors, quoted market prices, or other sources to determine the ultimate fair value of our assets and liabilities. We use such

pricing data as the primary input, to which we have not made any material adjustments during fiscal 2010 and fiscal 2009 to make

our assessments and determinations as to the ultimate valuation of our investment portfolio. We are ultimately responsible for the

financial statements and underlying estimates.

The inputs and fair value are reviewed for reasonableness, may be further validated by comparison to publicly available

information and could be adjusted based on market indices or other information that management deems material to their estimate

of fair value. In the current market environment, the assessment of fair value can be difficult and subjective. However, given the

relative reliability of the inputs we use to value our investment portfolio, and because substantially all of our valuation inputs are

obtained using quoted market prices for similar or identical assets, we do not believe that the nature of estimates and assumptions

affected by levels of subjectivity and judgment was material to the valuation of the investment portfolio as of July 31, 2010. Level 3

assets do not represent a significant portion of our total investment portfolio as of July 31, 2010.

Other-than-Temporary Impairments We recognize an impairment charge when the declines in the fair values of our fixed income or

publicly traded equity securities below their cost basis are judged to be other than temporary. The ultimate value realized on these

securities, to the extent unhedged, is subject to market price volatility until they are sold.

Effective at the beginning of the fourth quarter of fiscal 2009, we were required to evaluate our fixed income securities for

other-than-temporary impairments subject to new accounting guidance. Pursuant to this accounting guidance, if the fair value of a

debt security is less than its amortized cost, we assess whether the impairment is other than temporary. An impairment is

considered other than temporary if (i) we have the intent to sell the security, (ii) it is more likely than not that we will be required to

14 Cisco Systems, Inc.