3M 2014 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2014 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

43

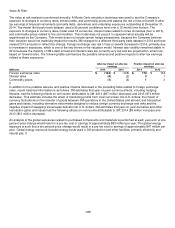

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

In the context of Item 7A, 3M is exposed to market risk due to the risk of loss arising from adverse changes in foreign

currency exchange rates, interest rates and commodity prices. Changes in those factors could cause fluctuations in

earnings and cash flows. Senior management provides oversight for risk management and derivative activities,

determines certain of the Company’s financial risk policies and objectives, and provides guidelines for derivative

instrument utilization. Senior management also establishes certain associated procedures relative to control and

valuation, risk analysis, counterparty credit approval, and ongoing monitoring and reporting.

The Company is exposed to credit loss in the event of nonperformance by counterparties in interest rate swaps, currency

swaps, commodity price swaps, and forward and option contracts. However, the Company’s risk is limited to the fair value

of the instruments. The Company actively monitors its exposure to credit risk through the use of credit approvals and

credit limits, and by selecting major international banks and financial institutions as counterparties. The Company does

not anticipate nonperformance by any of these counterparties.

Foreign Exchange Rates Risk:

Foreign currency exchange rates and fluctuations in those rates may affect the Company’s net investment in foreign

subsidiaries and may cause fluctuations in cash flows related to foreign denominated transactions. 3M is also exposed to

the translation of foreign currency earnings to the U.S. dollar. The Company enters into foreign exchange forward and

option contracts to hedge against the effect of exchange rate fluctuations on cash flows denominated in foreign

currencies. These transactions are designated as cash flow hedges. 3M may dedesignate these cash flow hedge

relationships in advance of the occurrence of the forecasted transaction. Beginning in the second quarter of 2014, 3M

began extending the maximum length of time over which it hedges its exposure to the variability in future cash flows of the

forecasted transactions from a previous term of 12 months to a longer term of 24 months. In addition, 3M enters into

foreign currency forward contracts that are not designated in hedging relationships to offset, in part, the impacts of certain

intercompany activities (primarily associated with intercompany licensing arrangements and intercompany financing

transactions). As circumstances warrant, the Company also uses foreign currency forward contracts and foreign currency

denominated debt as hedging instruments to hedge portions of the Company’s net investments in foreign operations. The

dollar equivalent gross notional amount of the Company’s foreign exchange forward and option contracts designated as

cash flow hedges and those not designated as hedging instruments were $2.2 billion and $6.6 billion, respectively, at

December 31, 2014. As of December 31, 2014, the Company had 200 million Euros in notional amount of foreign

currency forward contracts designated as net investment hedges along with 1.85 billion Euros in principal amount of

foreign currency denominated debt designated as non-derivative hedging instruments in certain net investment hedges as

discussed in Note 11 in the “Net Investment Hedges” section.

Interest Rates Risk:

The Company may be impacted by interest rate volatility with respect to existing debt and future debt issuances. 3M

manages interest expense using a mix of fixed and floating rate debt. To help manage borrowing costs, the Company may

enter into interest rate swaps that are designated and qualify as fair value hedges. Under these arrangements, the

Company agrees to exchange, at specified intervals, the difference between fixed and floating interest amounts calculated

by reference to an agreed-upon notional principal amount. The dollar equivalent (based on inception date foreign currency

exchange rates) gross notional amount of the Company’s interest rate swaps at December 31, 2014 was $1 billion.

Additional details about 3M’s long-term debt can be found in Note 9, including references to information regarding

derivatives and/or hedging instruments associated with the Company’s long-term debt.

Commodity Prices Risk:

Certain commodities the Company uses in the production of its products are exposed to market price risks. 3M manages

commodity price risks through negotiated supply contracts, price protection agreements and forward contracts. The

Company uses commodity price swaps as cash flow hedges of forecasted commodity transactions to manage price

volatility. Generally, the length of time over which 3M hedges its exposure to the variability in future cash flows for its

forecasted transactions is 12 months. 3M also enters into commodity price swaps that are not designated in hedge

relationships to offset, in part, the impacts of fluctuations in costs associated with the use of certain commodities and

precious metals.

The dollar equivalent gross notional amount of the Company’s commodity price swaps designated as cash flow hedges

and commodity price swaps not designated in hedge relationships were $20 million and $2 million, respectively, at

December 31, 2014.