Westjet 2009 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2009 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

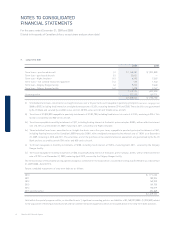

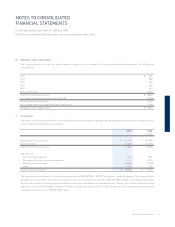

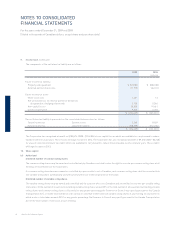

56 WestJet 2009 Annual Report

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS

For the years ended December 31, 2009 and 2008

(Stated in thousands of Canadian dollars, except share and per share data)

1. Summary of signifi cant accounting policies (continued)

(n) Leases

The Corporation classifi es leases as either a capital lease or an operating lease. Leases that transfer substantially all of the benefi ts and risk of

ownership to the Corporation are accounted for as capital leases. Assets under capital leases are depreciated on a straight-line basis over the

term of the lease. Rental payments under operating leases are expensed as incurred.

The Corporation provides for asset retirement obligations to return leased aircraft to certain standard conditions as specifi ed within the

Corporation’s lease agreements. The lease return costs are accounted for in accordance with the asset retirement obligations requirements and

are initially measured at fair value and capitalized to property and equipment as an asset retirement cost.

(o) Capitalized costs

Costs associated with assets under development, which have probable future economic benefi t, can be clearly defi ned and measured, and are

incurred for the development of new products or technologies, are capitalized. These costs are not amortized until the asset is substantially

complete and ready for its intended use, at which time, they are amortized over the life of the underlying asset.

Interest attributable to funds used to fi nance property and equipment is capitalized to the related asset until the point of commercial use.

(p) Future income tax

The Corporation uses the asset and liability method of accounting for future income taxes. Under this method, current income taxes are recognized

for the estimated income taxes payable for the current year. Future income tax assets and liabilities are recognized for temporary differences

between the tax and accounting bases of assets and liabilities, calculated using the currently enacted or substantively enacted tax rates anticipated

to apply in the period that the temporary differences are expected to reverse. Future income tax infl ows and outfl ows are subject to estimation in

terms of both timing and amount of future taxable earnings. Should these estimates change, the carrying value of income tax assets or liabilities

may change.

(q) Stock-based compensation plans

Grants under the Corporation’s stock-based compensation plans are accounted for in accordance with the fair-value-based method of accounting.

For stock-based compensation plans that will settle through the issuance of equity, the fair value of the option or unit is determined on the grant

date using a valuation model and recorded as compensation expense over the period that the stock option or unit vests, with a corresponding

increase to contributed surplus. The fair value of stock options is estimated on the date of grant using the Black-Scholes option pricing model,

and the fair value of the Corporation’s other equity-based share unit plans is determined based on the market value of the Corporation’s voting

shares on the date of the grant. Upon the exercise of stock options and units, consideration received, together with amounts previously recorded

in contributed surplus, are recorded as an increase in share capital.

Stock-based compensation plans that are to be settled in cash are accounted for as liabilities based on the intrinsic value of the awards. The

compensation expense is accrued over the vesting period of the award, based on the difference between the market value of the Corporation’s

common shares and the exercise price of the award, if any. Fluctuations in the market value of the Corporation’s common shares, determined

based on the closing share price on the last trading day of each reporting period, will result in a change to the accrued compensation expense,

which is recognized in the period in which the fl uctuation occurs.

The Corporation does not incorporate an estimated forfeiture rate for stock options or share units that will not vest, but rather accounts for actual

forfeitures as they occur.

For employees eligible to retire during the vesting period, the compensation expense is recognized over the period from the grant date to the

retirement eligibility date. In instances where an employee is eligible to retire on the grant date of the stock-based award, compensation expense

is recognized immediately.