Westjet 2009 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2009 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

WestJet 2009 Annual Report 21

measurement for the North American airline industry. Our bag

ratio represents the number of delayed or lost baggage claims

made per 1,000 guests.

$165.0 million during the third quarter of 2009. Additionally, we

signed and drew upon a 4.315 per cent fi xed-rate, fi ve-year term

loan, secured by one 800-series aircraft, for a total of US $32.0

million during the fourth quarter of 2009. Part of our cash and

cash equivalents balance relates to cash collected with respect

to advance ticket sales, for which the balance at December

31, 2009, was $286.4 million, as compared to $251.4 million at

December 31, 2008. Typically, we have cash and cash equivalents

on hand to have suffi cient liquidity to meet our liabilities when

due, under both normal and stressed conditions. As at December

31, 2009, we had cash on hand of 3.51 (2008 – 3.26) times the

advance ticket sales balance. Additionally, the increase in our

working capital ratio to 1.48, from 1.24 as at December 31, 2008,

further demonstrates our fi nancial stability and strong fi nancial

position. Credit risk associated with cash and cash equivalents is

minimized substantially by ensuring that these fi nancial assets

are invested primarily in debt instruments with highly rated

fi nancial institutions. As at December 31, 2009, we have not been

required to post collateral with respect to any of our outstanding

derivative contracts.

We monitor capital on a number of measures, including

adjusted debt-to-equity and adjusted net debt to EBITDAR

ratios. Our adjusted debt-to-equity ratio improved by 20.1 per

cent to 1.43 as at December 31, 2009, which included $779.7

million in off-balance-sheet aircraft operating leases. This

compared favourably to our adjusted debt-to-equity ratio of 1.79

at December 31, 2008, attributable to the signifi cant increase

in shareholders’ equity from the issuance of 15,398,500 voting

shares under our equity offering. As at December 31, 2009, our

adjusted net debt to EBITDAR ratio improved by 3.9 per cent to

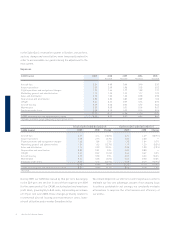

Key performance indicators

On-time performance and completion rates are calculated

based on the U.S. Department of Transportation’s standards of

On-time performance, indicating the percentage of fl ights that

arrived within 15 minutes of their scheduled time, is a key factor

in measuring our guest experience. During 2009, our on-time

performance improved by 1.6 points, due to more favourable

weather conditions, as compared to 2008. Our decline in on-

time performance in the fourth quarter of 2009 was due to a

number of factors, including winter weather, increased security

measures and the initial cutover to our new SabreSonic

reservation system.

Our completion rate remained relatively fl at for 2009 at 98.9

per cent versus 98.7 per cent in 2008. This indicator represents

the percentage of flights completed from flights originally

scheduled.

We also saw a signifi cant improvement in our bag ratio for 2009,

as compared to the prior year.

LIQUIDITY AND CAPITAL RESOURCES

The airline industry is highly sensitive to unpredictable

circumstances, and as such, maintaining a strong fi nancial

position is imperative to an airline’s success. During 2009,

the global recession negatively impacted the airline industry,

as evidenced by the rapid weakening of demand and reduced

discretionary spending. However, we have maintained one of

the most favourable balance sheets in the airline industry and

produced our 19th consecutive quarter of profi tability.

We completed 2009 with a signifi cant cash and cash equivalents

balance of $1,005.2 million, compared to $820.2 million as at

December 31, 2008. This increase primarily resulted from the

completion of an underwritten equity offering for net proceeds of

Three months ended December 31 Twelve months ended December 31

2009 2008 Change 2009 2008 Change

On-time performance 63.8% 68.9% (5.1 pts.) 78.6% 77.0% 1.6 pts.

Completion rate 99.1% 98.1% 1.0 pts. 98.9% 98.7% 0.2 pts.

Bag ratio 4.36 4.68 6.8% 3.57 4.12 13.3%