United Healthcare 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

UNITEDHEALTH GROUP

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

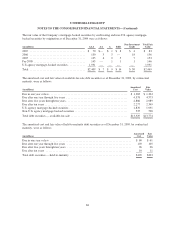

As of January 1, 2010, certain changes were made to the Medicare Part D coverage by CMS, including:

• The initial coverage limit increased to $2,830 from $2,700 in 2009.

• The catastrophic coverage begins at $6,440 as compared to $6,154 in 2009.

• The annual out-of-pocket maximum increased to $4,550 from $4,350 in 2009.

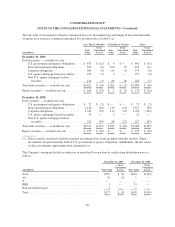

Property, Equipment and Capitalized Software

Property, equipment and capitalized software are stated at cost, net of accumulated depreciation and

amortization. Capitalized software consists of certain costs incurred in the development of internal-use software,

including external direct costs of materials and services and payroll costs of employees devoted to specific

software development. The Company reviews property, equipment and capitalized software for events or changes

in circumstances that would indicate that we might not recover their carrying value. If the Company determines

that an asset may not be recoverable, an impairment charge is recorded.

The Company calculates depreciation and amortization using the straight-line method over the estimated useful

lives of the assets. The useful lives for property, equipment and capitalized software are:

Furniture, fixtures and equipment 3 to 7 years

Buildings 35 to 40 years

Leasehold improvements Shorter of useful life or remaining lease term

Capitalized software 3 to 5 years

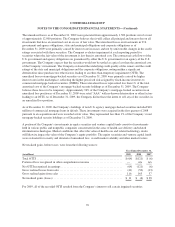

Goodwill

Goodwill represents the amount of the purchase price in excess of the fair values assigned to the underlying

identifiable net assets of acquired businesses. Goodwill is not amortized, but is subject to an annual impairment

test. Tests are performed more frequently if events occur or circumstances change that would more likely than

not reduce the fair value of the reporting unit below its carrying amount. To determine whether goodwill is

impaired, the Company performs a two-step impairment test. In the first step of the test, the fair values of the

reporting units are compared to their aggregate carrying values, including goodwill. If the fair value of the

reporting unit is greater than its carrying amount, goodwill is not impaired and no further testing is required. If

the fair value of the reporting unit is less than its carrying amount, the Company would proceed to step two of the

test. In step two of the test, the implied fair value of the goodwill of the reporting unit is determined by a

hypothetical allocation of the fair value calculated in step one to all of the assets and liabilities of that reporting

unit (including any recognized and unrecognized intangible assets) as if the reporting unit had been acquired in a

business combination and the fair value was reflective of the price paid to acquire the reporting unit. The implied

fair value of goodwill is the excess, if any, of the calculated fair value after hypothetical allocation to the

reporting unit’s assets and liabilities. If the implied fair value of the goodwill is greater than the carrying amount

of the goodwill at the analysis date, goodwill is not impaired and the analysis is complete. If the implied fair

value of the goodwill is less than the carrying value of goodwill at the analysis date, goodwill is deemed impaired

by the amount of that variance.

The Company calculates the estimated fair value of our reporting units using discounted cash flows. To

determine fair values the Company must make assumptions about a wide variety of internal and external factors.

Significant assumptions used in the impairment analysis include financial projections of free cash flow (includes

significant assumptions about operations, capital requirements and income taxes), long-term growth rates for

determining terminal value, and discount rates. Where available and appropriate, comparative market multiples

are used to corroborate the results of our discounted cash flow test.

62