Suzuki 2014 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2014 Suzuki annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

|

|

52 SUZUKI MOTOR CORPORATION

Consolidated Financial Statements

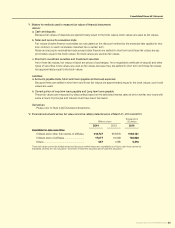

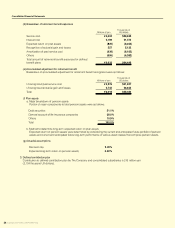

(d) Itemsrelatedtothecalculationstandardfortheretirementbenetobligation

NOTE 7:Retirementandseverancebenet

(Year ended March 31, 2013)

(a) Outlineofadoptedretirementbenetsystems

As for The Company, cash balance corporate pension plan and lump-sum retirement benet plan are established. And as for some

of consolidated subsidiaries, dened benet corporate pension plan and lump-sum retirement benet plan are established.

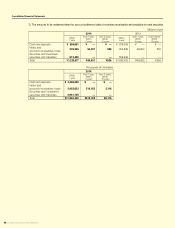

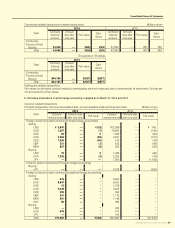

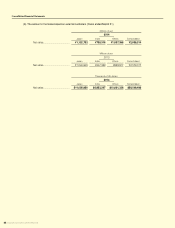

(b) ComponentofretirementbenetobligationasofMarch31,2013

Remarks: 1)

The premium retirement allowance paid on a temporary basis is not included.

2) Some of subsidiaries adopt simplified methods for the calculation of retirement benefits.

(c) ComponentofretirementbenetcostforyearendedMarch31,2013

Remarks: “a. Service cost” includes retirement benets cost of some of subsidiaries caluculated by simplied methods.

Millions of yen

a. Retirement benet obligation ¥(108,739)

b. Pension assets 83,842

c. Unfunded retirement benet obligation (a+b) ¥ (24,897)

d. Unrecognized difference by an actuarial calculation (810)

e. Unrecognized past service cost (decrease of liabilities) (4,063)

f. Net amount in consolidated balance sheet (c+d+e) (29,771)

g Prepaid pension cost 8,131

h. Provision for retirement benets (f-g) ¥ (37,903)

Millions of yen

a. Service cost ¥5,214

b. Interest cost 2,101

c. Assumed return on investment (699)

d. Amortized amount of actuarial difference 1,497

e. Amortized amount of past service cost (734)

f. Retirement benet cost (a+b+c+d+e) ¥7,379

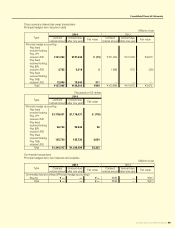

a. Allocation method of the estimated

amount of retirement benefits : Straight-line basis

b. Discount rate : Mainly 2.00%

c. Reassessment rate : 1.50%

d. Assumed return of investment ratio : Mainly 0.77%

e. Number of years for amortization : Mainly 15 years

of past service cost To be amortized by straight-line method with

certain term within the employees’ average remaining

service years at the time when the difference was caused.

f. Number of years for amortization : Mainly 15 years

of actuarial difference

To be amortized from the next fiscal year

by straight-line method with certain term within the

employees’ average remaining service years at the time

when the difference was caused.