SkyWest Airlines 2004 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2004 SkyWest Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

25

Interest expense increased to approximately $9.9 million during the year ended December 31, 2003, from approximately $3.6

million during the year ended December 31, 2002. The increase in interest expense was primarily due to the temporary long-debt

financing of the regional jets acquired by the Company during the twelve-month period ended December 31, 2003.

Liquidity and Capital Resources

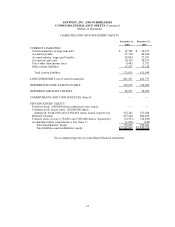

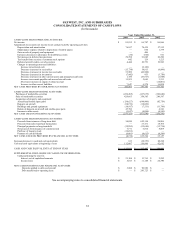

The Company had working capital of $536.5 million and a current ratio of 4.1:1 at December 31, 2004, compared to working

capital of $518.4 million and a current ratio of 4.4:1 at December 31, 2003. The principal sources of funds during the year ended

December 31, 2004 were $246.9 million provided by operating activities, $47.8 million of proceeds from returns on aircraft

deposits, $34.5 million of proceeds from the issuance of long-term debt and $7.8 million from the sale of common stock in

connection with the exercise of stock options under the Company’s stock option and employee stock purchase plans. During the

year ended December 31, 2004, the Company invested $193.4 million in flight equipment, $69.6 million in marketable securities,

$18.9 million in buildings and ground equipment and $3.5 million in other assets. The Company made principal payments on

long-term debt of $32.3 million, repurchased common stock for approximately $12.3 million and paid $6.4 million in cash

dividends. These factors resulted in a $0.6 million increase in cash and cash equivalents during the year ended December 31,

2004.

The Company’s receivables increased by approximately $15.8 million from December 31, 2004 from December 31, 2003. The

increase was primarily due to the increase in the price of fuel during the year and the fuel reimbursement provisions of the

Company’s contracts with its major partners. Under the contracts, the Company receives weekly wire transfers based on

estimated production and fuel costs, which payments are subsequently reconciled and adjusted after quarter and year end.

The Company’s position in marketable securities, consisting primarily of bonds, bond funds and commercial paper, increased to

$427.5 million at December 31, 2004, compared to $358.8 million at December 31, 2003. The increase in marketable securities

was due primarily to the Company’s cash management policies as excess cash is invested in marketable securities.

At December 31, 2004, the Company’s total capital mix was 62.7% equity and 37.3% debt, compared to 60.5% equity and 39.5%

debt at December 31, 2003. The change in the total capital mix during 2004 was primarily due to the Company’s refinancing

CRJ200s debt into long-term operating lease agreements with third-party lessors during the year ended December 31, 2004.

The Company expended approximately $71.9 million for aircraft related capital expenditures during the year ended December 31,

2004. These expenditures consisted primarily of $30.5 million for rotable spares, $15.8 million for engine overhauls, $6.7 million

for aircraft improvements, and $18.9 million for buildings, ground equipment and other assets.

The Company had available $10.0 million in an unsecured bank line of credit through January 31, 2006, with interest payable at

the bank’s base rate less one-quarter percent, which was a net rate of 5.0% at December 31, 2004. The Company had $6,461,000

of letters of credit with no borrowings outstanding under this line of credit as of December 31, 2004. Additionally, the Company

had $1,515,000 of letters of credit outstanding with another bank as of December 31, 2004. The Company believes that in the

absence of unusual circumstances, the working capital available to the Company will be sufficient to meet its present financial

requirements, including expansion, capital expenditures, lease payments and debt service obligations for at least the next 12

months.

At December 31, 2004 and December 31, 2003, the Company classified $9.2 million of cash as restricted cash on its condensed

consolidated balance sheets as required by the Company’s workers compensation policy.