Shutterfly 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 Shutterfly annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

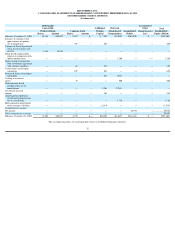

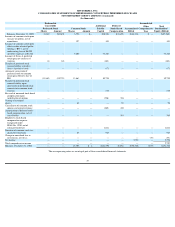

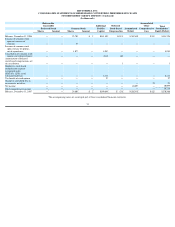

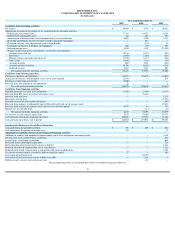

|

|

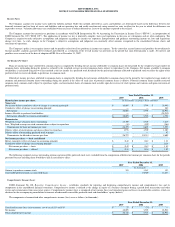

Note 1 — Description of Business

Shutterfly, Inc., (the “Company”) was incorporated in the state of Delaware in 1999 and began its services in December 1999. The Company is an Internet-based social

expression

and personal publishing service that enables customers to share, print and preserve their memories by leveraging a technology-

based platform and manufacturing processes. The

Company provides customers a full range of products and services to organize and archive digital images; share pictures; order prints and create an assortment of personalized items

such as cards, calendars and photo books. The Company is headquartered in Redwood City, California.

On September 29, 2006, the Company completed its initial public offering (“IPO”)

in which the Company sold 5,800,000 shares at a price to the public of $15.00 per share. As a

result of the IPO, a total of $87.0 million in gross proceeds was raised, with net proceeds to the Company of $78.5 million after deducting underwriting fees and commissions of

$6.1 million and other offering costs of $2.4 million. Upon the closing of the IPO, all shares of the Company’

s outstanding redeemable convertible preferred stock automatically

converted into an aggregate of 13,862,773 common shares.

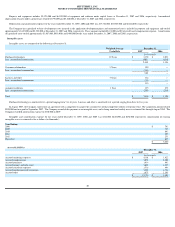

Note 2 — Summary of Significant Accounting Policies

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of the Company and its wholly owned subsidiary. The wholly owned subsidiary was dissolved in 2006

and was merged into the Company. All intercompany transactions and balances have been eliminated.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and

assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements as well as the reported

amounts of revenues and expenses during the reporting period. Significant items subject to such estimates and assumptions include intangible assets valuation and useful lives, excess

and obsolete inventories, deferred tax valuation allowance, legal contingencies, and the valuation of equity instruments among others. Actual results could differ from these estimates.

Cash, Cash Equivalents and Short Term Investments

The Company considers all highly liquid investments purchased with original maturities (at the date of purchase) of three months or less to be cash equivalents. Management

determines the appropriate classification of cash equivalents at the time of purchase and reevaluates such designations at each balance sheet date. Cash equivalents consist principally

of money market funds and commercial paper. Short term investments consist entirely of U.S. government agency securities.

At December 31, 2007, all investments are classified as “available-for-sale.”

In accordance with Statement of Financial Accounting Standards No 115, Accounting for Certain

Investments in Debt and Equity Securities (“SFAS 115”) available-for-

sale securities are carried at fair value, with the unrealized gains and losses, net of tax reported in a separate

component of accumulated other comprehensive income (loss) in shareholders’ equity. Realized gains and losses and declines in value judged to be other-than-temporary on available-

for-sale securities are reported in other income (expense), net. The cost of securities sold is based on the specific identification method. Interest on securities classified as available-for-

sale is included as a component of other income (expense), net. The contractual maturities for all of the Company’s available for sale securities are less than one year.

See Note 11 for a discussion of the Company’s investment in auction rate securities subsequent to December 31, 2007.

Fair Value of Financial Instruments

The carrying amount of certain of the Company’

s financial instruments, including accounts receivable and accounts payable, are carried at cost, which approximates their fair value

because of their short-

term maturities. Based on borrowing rates available to the Company for loans with similar terms, the carrying value of capital lease obligations, approximates fair

value.

Concentration of Credit Risk

Financial instruments that potentially subject the Company to credit risk consist principally of cash, cash equivalents, short term investments, and accounts receivable. Most of the

Company’

s cash and cash equivalents as of December 31, 2007, were deposited with financial institutions in the United States and Company policy restricts the amount of credit

exposure to any one issuer and to any one type of investment. Deposits held with financial institutions may exceed federally insured limits.

The Company’

s accounts receivable are derived primarily from sales to customers located in the United States who make payments through credit cards, sales of our products in

retail stores, and click-

through referral fees. Credit card receivables settle relatively quickly and the Company maintains allowances for potential credit losses based on historical

experience. To date, such losses have not been material and have been within management’

s expectations. Excluding amounts due from credit cards, as of December 31, 2007, two

customers accounted for 43% and 11% of the Company’s net accounts receivable. And as of December 31, 2006, one customer accounted for 14% of the Company’

s net accounts

receivable.

Inventories

Inventories are stated at the lower of cost on a first-in, first-

out basis or net realizable value. The value of inventories is reduced by estimates for excess and obsolete inventories.

The estimate for excess and obsolete inventories is based upon management’

s review of utilization of inventories in light of projected sales, current market conditions and market

trends. Inventories are primarily raw materials and consist principally of paper, photo book covers and packaging supplies.

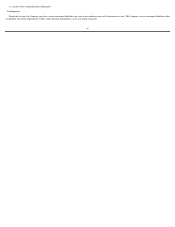

Property and Equipment

Property and equipment, including equipment under capital leases, are stated at historical cost, less accumulated depreciation and amortization. Depreciation and amortization are

computed using the straight-

line method over the estimated lives of the assets, generally three to five years. Amortization of equipment acquired under capital lease obligations is

computed using the straight-

line method over the shorter of the remaining lease term or the estimated useful life of the related assets, generally three to four years. Leasehold

improvements are amortized over their estimated useful lives, or the lease term if shorter, generally three to seven years. Upon retirement or sale, the cost and related accumulated

depreciation are removed from the balance sheet and the resulting gain or loss is reflected in operating expenses. Major additions and improvements are capitalized, while replacements,

maintenance and repairs that do not extend the life of the asset are charged to expense as incurred.

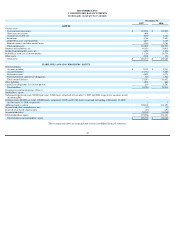

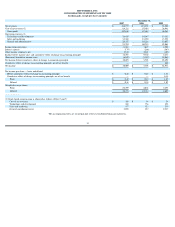

SHUTTERFLY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

36