Pentax 2003 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2003 Pentax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

|

|

43

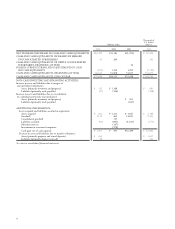

recognized as either assets or liabilities and measured at fair value,

and gains or losses on derivative transactions are recognized in

the statements of income and (b) for derivatives used for

hedging purposes, if derivatives qualify for hedge accounting

because of high correlation and effectiveness between the

hedging instruments and the hedged items, gains or losses on

derivatives are deferred until maturity of the hedged transac-

tions.

The foreign exchange forward contracts employed to hedge

foreign exchange exposures for export sales are measured at the

fair value and the unrealized gains/losses are recognized in

income. Forward contracts applied for forecasted (or commit-

ted) transactions are also measured at the fair value but the

unrealized gains/losses are deferred until the underlying transac-

tions are completed.

Long-term debt denominated in foreign currencies for which

foreign exchange forward contracts are used to hedge the foreign

currency fluctuations are translated at the contracted rate if the

forward contracts qualify for hedge accounting.

The interest rate swaps which qualify for hedge accounting

and meet specific matching criteria are not remeasured at market

value but the differential paid or received under the swap

agreements are recognized and included in interest expenses or

income.

o. Per Share Information

Effective April 1, 2002, the Company adopted a new accounting

standard for earnings per share of common stock issued by the

Accounting Standards Board of Japan. Under the new standard,

basic net income per share is computed by dividing net income

available to common shareholders, which is more precisely computed

than under previous practices, by the weighted-average number of

common shares outstanding for the period, retroactively adjusted for

stock splits.

Diluted net income per share reflects the potential dilution that

could occur if the outstanding stock options were exercised into

common stock. Diluted net income per share of common stock

assumes full exercise of the outstanding stock options at the begin-

ning of the year (or at the time of grant). Basic net income and

diluted net income per share for the years ended March 31, 2003,

2002 and 2001 are computed in accordance with the new standard.

Cash dividends per share presented in the accompanying consoli-

dated statements of income are dividends applicable to the respective

years including dividends to be paid after the end of the year.

No»3REORGANIZATION

(i) Reorganization of Subsidiaries to the Company’s Branches

On April 1, 2000, the Company purchased ORI Group which

consisted of 11 companies in the United States for ¥15,896

million and on October 31, 2000, Midwest Optical Laborato-

ries, Inc. (“MOL”) for ¥513 million. ORI Group, MOL and a

newly established American company consisted of Hoya Optical

Laboratories, Inc. (“HOL”) and 12 consolidated subsidiaries,

which had been wholly owned American subsidiaries of HOL.

On March 1, 2001, the Company reorganized HOL and the

12 consolidated subsidiaries to the Company’s branches. Due to

the reorganization, goodwill of ¥15,167 million was recorded and

subsequently ¥14,347 million was charged to income. Also an

adjustment of retained earnings for the reorganization of consoli-

dated subsidiaries to branches was recorded in the amount of

¥820 million as an adjustment to income from April 1, 2000 to

February 28, 2001 for HOL and subsidiaries.

(ii) Reorganization of Subsidiaries

On September 30, 2001, the Company purchased the minority

interest of Hoya Optikslip AB (“HOSL”) in Sweden for ¥384

million to become a wholly owned consolidated subsidiary.

Previously, HOSL had been accounted for by the equity

method.

On October 1, 2001, Welfare Corporation, which had been a

wholly owned unconsolidated subsidiary of the Company, was

merged into Hoya Healthcare Corporation (“HHC”). On

January 1, 2002, Welfare Corporation was then split up from

HHC.

On February 1, 2002, the Company purchased Eagle Optics,

Inc. in the United States for ¥474 million.

On March 31, 2002, the Company increased its ownership of

Thai Hoya Lens Ltd. to become a consolidated subsidiary, which

had been accounted for by the equity method.

(iii) Merger of the Company with Subsidiaries

On March 1, 2003, the Company purchased Hoya Lens of Chicago,

Inc. in the United States for ¥1,301 million ($10,842 thousand).

On March 1, 2003, the Company merged with Hoya Techno Process

Corporation and two other companies, which had been wholly

owned unconsolidated subsidiaries of the Company.

(iv) Transfer of Business

On March 31, 2003, a part of hearing aid business in Eye-Care field

was transferred to a third party.