Nissan 2011 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2011 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46

|

|

Maintaining Trust Through Transparency

Development of decision making system

In addition to the current rules of the SRMC, a system for delegation of authority was developed to

approve countermeasures and expenditures.

Following the March 11 disaster, we provided relief supplies to our suppliers in the stricken region.

We also carried out active aid efforts for suppliers based on their requests in order to help restore

the supply chain more quickly. We have now prepared measures with suppliers to address expected

power shortages.

5) Risk Financing and Loss Prevention

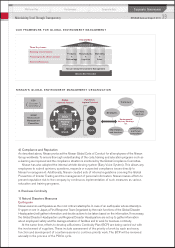

Global Insurance Management Policy

Nissan manages hazard risk with risk financing techniques that combine self-retained risk with

external risk transfer via insurance. In order to optimize the cost of risk, Nissan has introduced a risk

management policy.

• Predictable risks with low impact and high frequency

→Retained risks up to an acceptable level on a consolidated basis by the company

• Unpredictable risks with low frequency and high impact or shock value

→

Risks whose financial impact may exceed the acceptable level of self-retention are

transferred outside the company via insurance

Global Insurance Program

In order to minimize the cost of hazard risks and manage risks occurring globally and

interdependently in a concentrated manner, global insurance programs have been established for

main lines of insurance. The Finance Department in the Global Headquarters decides insurance

conditions and structures, and negotiates directly with insurance companies for these global

programs. The insurance companies are decided in consideration of risk spread and financial

solvency.

The following risks are covered in this way.

• Property damage and business interruption by accidents

Program covers risks not only for property damage but also for business interruption and

contingent business interruption due to accidents, taking into consideration global expansion of

supply chain for products and parts. Coverage limits are determined based on the probable

maximum loss amount measured by third party experts.

We achieved further improvement and optimization of the insurance conditions by negotiating

with insurance market together with our Alliance partner Renault from fiscal 2011.

• Transportation and storage of vehicles and products for sales

This programs covers risks of transportation and the supply chain for parts and products

globally. By covering risks spread geographically under a global program, we can manage loss

data spread globally and ensure stability of insurance cost.

From fiscal 2011, this program was also combined with Renault’s program for negotiating

with insurance companies to achieve best possible results utilizing synergies of scale.

• Product liability

To manage this risk, we have insurance programs suitable for the legal systems and practices in

each region. The programs are led by Global Headquarters in order to implement a consistent

strategy globally.

Utilization of captive insurance company

For the purpose of more efficient self-retention on a consolidated basis, a captive insurance

company (an insurance company of the Nissan Group) is utilized for these global insurance

programs.

Corporate Governance

Performance Corporate DataMid-term Plan

43

NISSAN Annual Report 2011