National Grid 2016 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2016 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

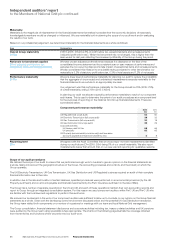

Area of focus

How our audit addressed the area of focus and whatwe reported

totheAuditCommittee

Revenue recognition

During the year National Grid has recognised revenue of £15.1bn;

£14.2bn of which is mostly related to the regulated segments in the

UK andUS.

In the UK, National Grid’s revenue is derived from anumber of

pricecontrols imposed by the UK regulator,Ofgem, when combined

with the application of IFRS, revenue recognition involves limited

judgement. The majority of revenue is derived from a small number

ofcustomers who settle within agreed terms.

In the US, different services and locations are regulated by different

authorities and are subject to numerous price controls. Unlike the

UK,revenue is earned through the transportation and supply of gas

and electricity toend customers, which does involve judgement

as aresult of the estimate of accrued income for services delivered

but not yet billed tothese customers. This is determined using a

long-established methodology within the Group.

As such revenue recognition is not an area of significant risk for our

audit but does require significant time and resource to audit due

to the magnitude.

Change in level of risk year on year: No change

In the UK, we have tested the design and operating effectiveness of

key controls in relation to the recognition ofrevenue, with particular

focus on controls over the setting of prices compared to those

allowed by the Ofgem price controls and we found no material

issuesthat would impact our audit approach.

We have tested the revenue recognised to amounts invoiced to

customers and the subsequent receipt of payment from those

customers, with no material exceptions noted.

In the US, in respect of transmission and other non-utility revenues,

we selected and tested individual transactions to ensure they were

appropriately recorded as revenue in the correct period. We inspected

proof of cash payments or confirmed amounts with customers where

itwas possible to do so. We also inspected regulator-approved

tariffs to test that amounts charged were consistent with such tariffs.

We found no material issues arising fromour work.

For utility revenues, we selected samples of rate classes to test

thatcustomer rates were properly updated in the billing systems,

andthat rate types were assigned to customers consistent with

thetype of customer and (where appropriate) the volume of usage.

We also selected samples of customer bills and tested that such

billswere paid by customers and were consistent with the regulator-

approved rate plans. For those bills selected that were outstanding

atthe end of the year, weconfirmed the balance with customers,

andtested amounts to subsequent cash receipts where no

confirmation was received.

With respect to unbilled revenue we tested management’s

assumptions in relation to consumption by reference to historical

dataas well as specific current year factors, including weather

patterns. In so doing, we did not note any significant issues which

would impact the Group financial statements.

Going concern

Under the Listing Rules we are required to review the Directors’ statement, set out on page 102, in relation to going concern. We have nothing

toreport having performed our review.

Under ISAs (UK & Ireland) we are required to report to you if we have anything material to add or to draw attention to in relation to the

Directors’statement about whether they considered it appropriate to adopt the going concern basis in preparing the financial statements.

Wehave nothing material to add or to draw attention to.

As noted in the Directors’ statement, the Directors have concluded that it is appropriate to adopt the going concern basis in preparing

the financial statements. The going concern basis presumes that the Group and Company have adequate resources to remain in operation,

and that the Directors intend them to do so, for at least one year from the date the financial statements were signed. As part of our audit

we have concluded that the Directors’ use of the going concern basis is appropriate. However, because not all future events or conditions

can be predicted, these statements are not a guarantee as to the Group’s and Company’s ability to continue as a going concern.

90 National Grid Annual Report and Accounts 2015/16 Financial Statements

Independent auditors’ report

to the Members of National Grid plc continued