Microsoft 2002 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2002 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

|

|

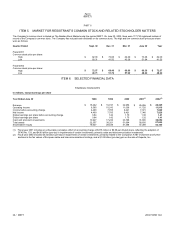

MSFT 32 / 2002 FORM 10-K

Part II

Item 7

wise Marketed. SFAS 86 specifies that costs incurred internally in creating a computer software product should be charged to expense when incurred as

research and development until technological feasibility has been established for the product. Once technological feasibility is established, all software costs

should be capitalized until the product is available for general release to customers. Judgment is required in determining when the technological feasibility of

a product is established. Microsoft has determined that technological feasibility for its products is reached shortly before the products are released to

manufacturing. Costs incurred after technological feasibility is established are not material, and accordingly, the Company expenses all research and

development costs when incurred.

Microsoft is subject to various legal proceedings and claims, the outcomes of which are subject to significant uncertainty. SFAS 5, Accounting for

Contingencies, requires that an estimated loss from a loss contingency should be accrued by a charge to income if it is probable that an asset has been

impaired or a liability has been incurred and the amount of the loss can be reasonably estimated. Disclosure of a contingency is required if there is at least a

reasonable possibility that a loss has been incurred. The Company evaluates, among other factors, the degree of probability of an unfavorable outcome and

the ability to make a reasonable estimate of the amount of loss. Changes in these factors could materially impact the Company’s financial position or its

results of operations.

SFAS 109, Accounting for Income Taxes, establishes financial accounting and reporting standards for the effect of income taxes. The objectives of

accounting for income taxes are to recognize the amount of taxes payable or refundable for the current year and deferred tax liabilities and assets for the

future tax consequences of events that have been recognized in an entity’s financial statements or tax returns. Judgment is required in assessing the future

tax consequences of events that have been recognized in the Company’s financial statements or tax returns. Fluctuations in the actual outcome of these

future tax consequences could materially impact the Company’s financial position or its results of operations.

ISSUES AND UNCERTAINTIES

The following issues and uncertainties, among others, should be considered in evaluating the Company’s financial outlook.

Challenges to the Company’s Business Model. Since its inception, the Company’s business model has been based upon customers agreeing to pay a

fee to license software developed and distributed by Microsoft. Under this commercial software development (“CSD”) model, software developers bear the

costs of converting original ideas into software products through investments in research and development, offsetting these costs with the revenues received

from the distribution of their products. The Company believes that the CSD model has had substantial benefits for users of software, allowing them to rely on

the expertise of the Company and other software developers that have powerful incentives to develop innovative software that is useful, reliable and

compatible with other software and hardware. In recent years, there has been a growing challenge to the CSD model, often referred to as the Open Source

movement. Under the Open Source model, software is produced by global “communities” of programmers, and the resulting software and the intellectual

property contained therein is licensed to end users at little or no cost. The Company believes that there are significant problems with the Open Source model,

the principal drawback being that no single entity is responsible for the Open Source software, and thus users have no recourse if a product does not work

properly or at all. Further, without the market incentives associated with the CSD model, the Company believes that the vigorous innovation and growth of the

software industry over the last 25 years would not have occurred. Nonetheless, the popularization of the Open Source movement continues to pose a

significant challenge to the Company’s business model, including recent efforts by proponents of the Open Source model to convince governments worldwide

to mandate the use of Open Source software in their purchase and deployment of software products. To the extent the Open Source model gains increasing

market acceptance, sales of the Company’s products may decline, the Company may have to reduce the prices it charges for its products, and revenues and

operating margins may consequently decline.

New Products and Services. The Company has made significant investments in research and development for new products, services and technologies,

including Microsoft .NET, Xbox, business applications, MSN, mobile and wireless technologies, and television. Significant revenue from these investments

may not be achieved for a number of years, if at all. Moreover, these products and services may never be profitable, and even if they are profitable, operating

margins for these businesses are not expected to be as high as the margins historically experienced in our Desktop and Enterprise Software and Services

businesses.

Declines in Demand for Software. If overall market demand for PCs, servers and other computing devices declines significantly, and consumer and

corporate spending for such products declines, Microsoft’s revenue growth will be adversely affected. Additionally, the Company’s revenues would be

unfavorably impacted if customers reduce their purchases of new software products or upgrades to existing products if such new offerings are not perceived

to add significant new functionality or other value to prospective purchasers.

Product Development Schedule. The development of software products is a complex and time-consuming process. New products and enhancements to

existing products can require long development and testing periods. Significant delays in new product releases or significant problems in creating new

products could negatively impact the Company’s revenues.

International Operations. Microsoft develops and sells products throughout the world. The prices of the Company’s products in countries outside of the

United States are generally higher than the Company’s prices in the United States because of the cost incurred in localizing software for non-U.S. markets.

The costs of producing and selling the Company’s products in these countries also are higher. Pressure to globalize Microsoft’s pricing structure might

require that the Company reduce the sales price of its software in other countries, even though the costs of the software continue to be higher than in the

United States. Unfavorable changes in trade protection laws, policies and measures, and other regulatory requirements affecting trade and investment;

unexpected changes in regulatory requirements for software; social, political, labor, or economic conditions in a specific country or region, including foreign

exchange rates; difficulties in staffing and managing foreign operations; and potential adverse foreign tax consequences, among other factors, could also

have a negative effect on the Company’s business and results of operations outside of the United States.