JetBlue Airlines 2012 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2012 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

JETBLUE AIRWAYS CORPORATION-2012 10K 35

PART II

ITEM7Management’s Discussion and Analysis of Financial Condition and Results of Operations

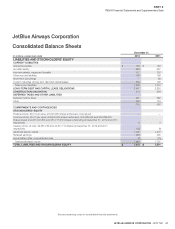

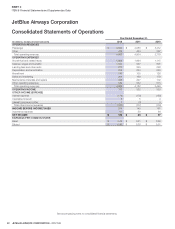

Financing Activities

Financing activities during 2012 consisted of (1)scheduled maturities of

$198 million of debt and capital lease obligations, (2) the pre-payment

of $185 million in high-cost debt secured by seven Airbus A320 aircraft,

(3) the repayment of $35 million of debt related to two EMBRAER 190

aircraft which were sold in 2012, (4)proceeds of $215 million in non-

public fl oating rate aircraft-related fi nancing secured by four Airbus A320

aircraft and four EMBRAER 190 aircraft, (5) the net repayment of $88

million under our available lines of credit, (6)the repayment of $12million

in principal related to our construction obligation for Terminal 5 and (7)the

acquisition of 4.8 million treasury shares for $26million primarily related

to our share repurchase program and the withholding of taxes upon the

vesting of restricted stock units.

Financing activities during 2011 consisted primarily of (1)the early

extinguishment of $39 million principal of our 6.75% Series A convertible

debentures due 2039 for $45 million, (2)scheduled maturities of $188 million

of debt and capital lease obligations, (3)the early payment of $3 million on

our spare parts pass-through certifi cates, (4)proceeds of $121 million in

fi xed rate and $124 million in non-public fl oating rate aircraft-related fi nancing

secured by four Airbus A320 aircraft and fi ve EMBRAER 190 aircraft, (5)the

net borrowings of $88 million under our available line of credit, (6)the

repayment of $10 million in principal related to our construction obligation

for Terminal 5 and (7)the acquisition of $4 million in treasury shares related

to the withholding of taxes, upon the vesting of restricted stock units.

In November 2012, we fi led an automatic shelf registration statement with

the SEC. Under this universal shelf registration statement, we have the

capacity to offer and sell from time to time debt securities, pass-through

certifi cates, common stock, preferred stock and/or other securities. The

net proceeds of any securities we sell under this registration statement

may be used to fund working capital and capital expenditures, including

the purchase of aircraft and construction of facilities on or near airports.

Through December 31, 2012, we had not issued any securities under

this registration statement. At this time, we have no plans to sell any such

securities under this registration statement. We may utilize this universal

shelf in the future to raise capital to fund the continued development of

our products and services, the commercialization of our products and

services or for other general corporate purposes.

None of our lenders or lessors are affi liated with us.

Capital Resources

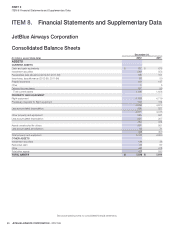

We have been able to generate suffi cient funds from operations to meet

our working capital requirements. Approximately 70% of our property and

equipment is encumbered, excluding 11 Airbus A320 aircraft and nine spare

engines which we own free and clear. We have historically fi nanced our

aircraft through either secured debt or lease fi nancing. At December31,

2012, we operated a fl eet of 180 aircraft, of which 60 were fi nanced under

operating leases, four were fi nanced under capital leases and all but 11

of the remaining 116 were fi nanced by private and public secured debt.

As noted above, we pre-paid some of 2013 aircraft deliveries. We have

committed fi nancing for two EMBRAER 190 aircraft scheduled for delivery

in 2013. We plan to opportunistically fi nance the remaining 2013 scheduled

deliveries at favorable borrowing terms relative to our weighted average

cost of debt. Although we believe debt and/or lease fi nancing should be

available for our remaining aircraft deliveries, we cannot give assurance we

will be able to secure fi nancing on terms attractive to us, if at all. While these

fi nancings may or may not result in an increase in liabilities on our balance

sheet, our fi xed costs will increase signifi cantly regardless of the fi nancing

method ultimately chosen. To the extent we cannot secure fi nancing, we

may be required to pay in cash, further modify our aircraft acquisition plans

or incur higher than anticipated fi nancing costs.

Working Capital

We had working capital defi cit of $508 million at December 31, 2012

compared to working capital of $216million at December31, 2011.

Working capital defi cits can be customary in the airline industry since air

traffi c liability is classifi ed as a current liability. The signifi cant decrease in

our working capital is primarily attributable to approximately $220 million

in debt prepayments made during 2012 and the $200 million prepayment

for future aircraft deliveries. Our working capital includes the fair value of

our short-term fuel hedge derivatives, which was a net liability of $1 million

and $4 million at December31, 2012 and 2011, respectively.

Also contributing to our working capital defi cit as of December 31, 2012

is $136 million in marketable investment securities classifi ed as long-

term assets, including $57 million related to a deposit made to lower the

interest rate on the debt secured by two aircraft. These funds on deposit

are readily available to us; however, if we were to draw upon this deposit,

the interest rates on the debt would revert to the higher rates in effect

prior to the re-fi nancing.

We have a corporate purchasing line with American Express allowing us

to borrow up to a maximum of $125million for the purchase of jet fuel.

Borrowings, which are to be paid monthly, are subject to a 6.9% annual

interest rate subject to certain limitations. This borrowing facility will

terminate no later than January 5, 2015. During 2012, we had borrowed

up to $125 million on this corporate purchasing line, all of which was

fully repaid, leaving the line undrawn as of December 31, 2012. In July

2012, we entered into a revolving line of credit with Morgan Stanley for

up to $100 million, and increased the line of credit for up to $200 million

in December 2012. This line of credit is secured by a portion of our

investment securities held by Morgan Stanley and the borrowing amount

may vary accordingly. This line of credit bears interest at a fl oating rate of

interest based upon LIBOR plus 100 basis points. During 2012, we had

borrowed up to the maximum $200 million, all of which was fully repaid,

leaving the line undrawn as of December 31, 2012.

We expect to meet our obligations as they become due through available

cash, investment securities and internally generated funds, supplemented

as necessary by fi nancing activities, as they may be available to us. We

expect to generate positive working capital through our operations.

However, we cannot predict what the effect on our business might

be from the extremely competitive environment we are operating in or

from events beyond our control, such as volatile fuel prices, economic

conditions, weather-related disruptions, the impact of airline bankruptcies,

restructurings or consolidations, U.S. military actions or acts of terrorism.

We believe the working capital available to us will be suffi cient to meet our

cash requirements for at least the next 12months.

Debt and Capital Leases

Our scheduled debt maturities are expected to increase over the next fi ve

years, with a scheduled peak in 2014 of nearly $600 million. Our scheduled

debt maturities in 2013 include fi nal mortgage payments on six Airbus

A320 aircraft, which will further increase our portfolio of unencumbered

assets. As part of our efforts to effectively manage our balance sheet

and improve ROIC, we expect to continue to actively manage our debt

balances. Our approach to debt management includes managing the mix

of fi xed vs. fl oating rate debt, managing the annual maturities of debt,

and managing the weighted average cost of debt. Further, we intend to

continue to opportunistically pre-purchase outstanding debt when market

conditions and terms are favorable. Additionally, our unencumbered assets,

including 11 A320 aircraft, allows us some fl exibility in managing our cost

of debt and capital requirements.