JetBlue Airlines 2012 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2012 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

JETBLUE AIRWAYS CORPORATION-2012 10K08

PART I

ITEM 1Business

We strive to provide a superior air travel experience, including communicating

openly and honestly with customers about delays and service disruptions.

We introduced the JetBlue Airways Customer Bill of Rights in 2007. This

provides for compensation to customers who experience avoidable

inconveniences (as well as some unavoidable circumstances), commits

us to perform at high service standards and holds us accountable if we

do not. We are the fi rst and currently the only U.S. major airline to provide

such a fundamental benefi t to customers. In 2012, we completed 99%

of our scheduled fl ights. Unlike most other airlines, we have a policy of

not overbooking our fl ights.

Brand Strength. JetBlue is a widely recognized and respected global

brand. We believe our brand differentiates us from our competitors and

identifi es us as a safe, reliable, high value airline. Our brand has evolved

into an important and valuable asset. Similarly, we believe customer

awareness of our brand has contributed to the success of our marketing

efforts. It enables us to promote ourselves as a preferred marketing partner

with companies across many different industries. In 2012, we once again

received several prestigious awards, including being voted “Highest in

Airline Customer Satisfaction among Low-Cost Carriers” by J.D. Power

and Associates for the eighth consecutive year.

Our customers have repeatedly indicated the JetBlue Experience is an

important reason why they choose us over other airlines. We believe our

high satisfaction rating serves as evidence our customers value what we

have to offer. We measure and monitor our customer feedback regularly

to achieve a primary goal of continuously improving customer satisfaction.

One way we do so is by measuring our net promoter score, or NPS. This

metric is used by many industries to gauge customer experience. Our

internal measurement shows improvements in our NPS score from 2011

to 2012, and we are focused on being an industry leader in this metric.

Many of the leading brands consumers are most familiar with receive high

NPS scores and are recognized for great customer service. We believe

a higher NPS score leads to higher customer loyalty which results in

increased revenue.

Marketing and Distribution

We market our services through advertising and promotions in various media

forms including using increasingly popular social media outlets. We engage

in large multi-market programs, many local events and sponsorships as

well as mobile marketing programs. Our targeted public and community

relations efforts refl ect our commitment to the communities we serve, as well

as promoting brand awareness and complementing our strong reputation.

Our primary and preferred distribution channel is through our website,

www.jetblue.com, our lowest cost channel. We re-designed our website in

2012 to ensure our customers continue to have as pleasant an experience

booking their travel as they do in the air. Our participation in global distribution

systems, or GDSs, supports our profi table growth in the corporate market.

We fi nd that business customers are more likely to book through a travel

agency or a booking product which rely on a GDS platform. Although

the cost of sales through this channel is higher than through our website,

the average fare purchased through the GDSs is generally higher and

often covers the increased distribution costs. We currently participate

in several major GDSs and online travel agents, or OTAs. In 2012, we

launched mobile applications for both Apple and Android devices designed

to enhance our customers’ travel experience. These applications have

robust features, including real-time fl ight information updates. Because

the majority of our customers book travel on our website, we maintain

relatively low distribution costs despite increases in recent years in our

participation in GDS and OTA.

We sell vacation packages through JetBlue Getaways™, a one-stop,

value-priced vacation website and service designed to meet customers’

demand for self-directed packaged travel planning. JetBlue Getaways™

packages offer competitive fares for air travel on JetBlue, along with a

selection of JetBlue-recommended hotels and resorts, car rentals and

attractions. We also offer a la carte hotel and car rental reservations through

our website which generates ancillary service revenues.

Route Network. We believe knowing our customers and understanding

the purpose of their travel helps optimize destinations, strengthen our route

schedules and increase unit revenues. Historically, we have been a strong

leisure focused airline resulting in high seasonality in our business. In recent

years, in order to offset this seasonality, we have increased our relevance to

the business customer, particularly in Boston. Additionally, we have continued

profi table growth in the Latin America and Caribbean region, with a mix of

leisure and visiting friends and relatives, or VFR, travelers. VFR travelers tend

to be slightly less seasonal and less susceptible to economic downturns than

traditional leisure destination travelers. We have also expanded our portfolio

of strategic commercial partnerships, which generate incremental customers

throughout our network and help to increase load factor during our off-peak

travel periods. We are focused on continuing to grow our network and further

reducing our seasonality by targeting new customers in the leisure, business

and VFR areas. Our operations primarily consist of transporting passengers

on our aircraft. Domestic U.S. operations, including Puerto Rico, accounted

for 84% of our capacity in 2012. The historic distribution of our available seat

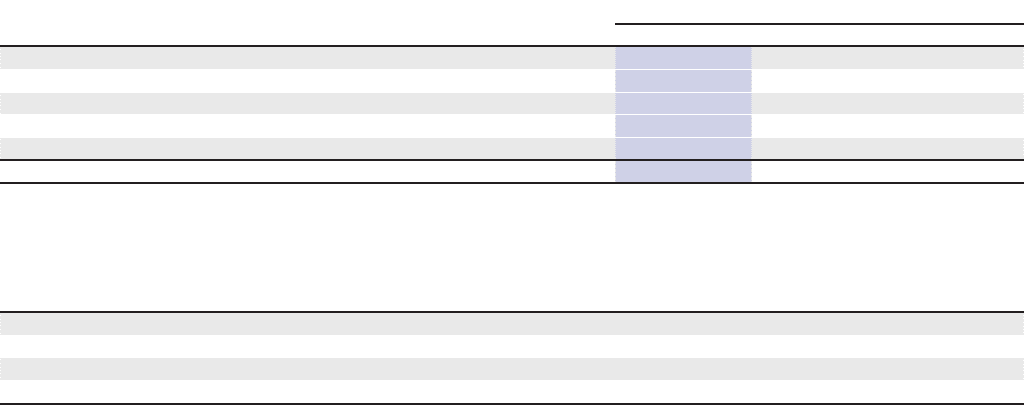

miles, or capacity, by region is:

Capacity Distribution

Year Ended December31,

2012 2011 2010

East Coast – Western U.S. 32.1% 32.4% 34.5%

Northeast – Florida 30.6 32.2 31.4

Medium-haul 2.9 3.2 3.3

Short-haul 7.2 7.5 7.6

Caribbean, including Puerto Rico 27.2 24.7 23.2

TOTAL 100.0% 100.0% 100.0%

As of December31, 2012, we provided service to 75 destinations in 23 states, Puerto Rico, the U.S. Virgin Islands, Mexico, and 12 countries in the Caribbean

and Latin America. In 2012, we commenced service to fi ve diverse new destinations, including Dallas/Fort Worth, Texas and Grand Cayman, Cayman Islands.

We also reduced service tactically across our system, where the markets were not performing adequately. In 2013, we intend to begin service to the following

destinations:

Destination ServiceScheduled to Commence

Charleston, South Carolina February 2013

Albuquerque, New Mexico April 2013

Philadelphia, Pennsylvania May 2013

Medellin, Colombia June 2013