Frontier Airlines 2005 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2005 Frontier Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

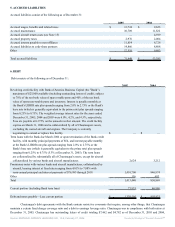

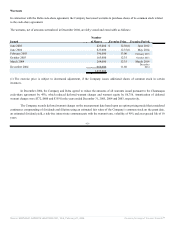

Deferred tax assets include benefits expected to be realized from the utilization of alternative minimum tax credit

carryforwards of $457, which do not expire, and net operating loss carryforwards of $504,000, which begin expiring in 2022.

Approximately $450,000 net operating loss carryforwards are limited under Internal Revenue Code Section 382, and approximately

$23,000 is not expected to be realized prior to expiration.

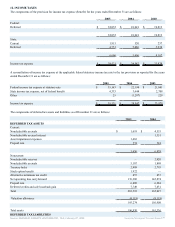

13. FAIR VALUE OF FINANCIAL INSTRUMENTS

The fair value of a financial instrument is defined as the amount at which the instrument could be exchanged in an arm's

length transaction between knowledgeable, willing parties. The fair value of long term debt is estimated based on discounting

expected cash flows at the rates currently offered to the Company for debt with similar remaining maturities. As of December 31,

2005 and 2004 respectively, the carrying value of long-term debt was greater than its fair value by approximately $95,302 and

$67,000. As of December 31, 2004, the fair value of the treasury locks was a liability of $4,012 based on quoted market values.

14. BENEFIT PLAN—401(k)

Republic has a defined contribution retirement plan covering substantially all eligible employees. The Company matches up

to 6.0% of eligible employees' wages. Employees are generally vested in matching contributions after three years of service with the

Company. Employees are also permitted to make pre-tax contributions of up to 90% (up to the annual Internal Revenue Code limit)

and after-tax contributions of up to 10% of their annual compensation. The Company's expense under this plan was $1,660, $1,128

and $540 for the years ended December 31, 2005, 2004 and 2003, respectively.

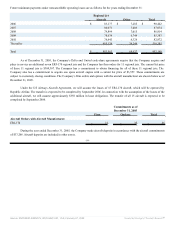

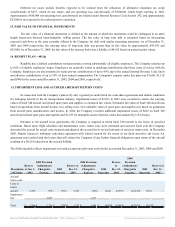

15. IMPAIRMENT LOSS AND ACCRUED AIRCRAFT RETURN COSTS

In connection with the Company’s plan to fly only regional jets under fixed fee code-share agreements and market conditions

for turboprop aircraft in the air transportation industry, impairment losses of $2,931 in 2003 were recorded to reduce the carrying

values of Saab 340 aircraft and related spare parts and supplies to estimated fair values. Estimated fair value of Saab 340 aircraft was

based on quotations from aircraft dealers, less selling costs. Net realizable value of spare parts and supplies was based on quotations

from aircraft parts manufacturers and dealers. In 2004, the Company recorded additional impairment losses of $416 on Saab 340

aircraft and related spare parts and supplies and $1,255 for intangible assets related to routes discontinued by US Airways.

Pursuant to the aircraft lease agreements, the Company is required to return Saab 340 aircraft to the lessor in specified

conditions. Based upon flight schedules and maintenance costs, return costs were estimated and accrued. Each year the Company

decreased the accrual for actual costs incurred and adjusted the accrual for its revised estimate of expected return costs. In December

2005, Shuttle America’s turboprop code-share agreement with United expired for the return of our Saab aircraft to the lessor. An

agreement was reached with the lessors that will release the Company of any further financial obligations upon return of the aircraft

resulting in a $4,218 reduction in the accrued liability.

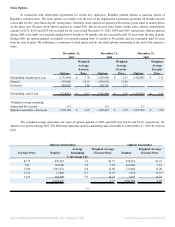

The following table reflects impairment costs and accrued aircraft return costs for the year ended December 31, 2003, 2004 and 2005.

Description

of Charge

Reserve

at Jan. 1,

2003

2003 Provision

(Adjustment)

Charged to

Expense

2003

Payments

Reserve at

Dec. 31,

2003

2004 Provision

(Adjustment)

Charged to

Expense

2004

Payments

Reserve

at

Dec. 31,

2004

2004

Provision

(Adjustment)

Charged to

Expense

2005

Payments

Reserve at

Dec. 31,

2005

Aircraft

return costs:

Costs to

return

aircraft

5,706 (175) (278) 5,253 (230) (424) 4,599 $ (4,218)$ (381) —

Impairment

loss 2,931 1,671 —

Total $ 5,706 $ 2,756 $ (278)$ 5,253 $ 1,441 $ (424)$ 4,599 $ (4,218)$ (381)$ —

Source: REPUBLIC AIRWAYS HOLDINGS INC, 10-K, February 27, 2006 Powered by Morningstar® Document Research℠