Foot Locker 2011 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2011 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

FOOT LOCKER, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies − (continued)

To the extent derivatives do not qualify or are not designated as hedges, or are ineffective, their changes in

fair value are recorded in earnings immediately, which may subject the Company to increased

earnings volatility.

Fair Value

The Company categorizes its financial instruments into a three-level fair value hierarchy that prioritizes

the inputs to valuation techniques used to measure fair value into three broad levels. The fair value

hierarchy gives the highest priority to quoted prices in active markets for identical assets or liabilities

(Level 1) and the lowest priority to unobservable inputs (Level 3). If the inputs used to measure fair value

fall within different levels of the hierarchy, the category level is based on the lowest priority level input

that is significant to the fair value measurement of the instrument. Fair value is determined based upon the

exit price that would be received to sell an asset or paid to transfer a liability in an orderly transaction

between market participants exclusive of any transaction costs.

The Company’s financial assets recorded at fair value are categorized as follows:

Level 1 − Quoted prices for identical instruments in active markets.

Level 2 − Quoted prices for similar instruments in active markets; quoted prices for identical or

similar instruments in markets that are not active; and model-derived valuations in which all

significant inputs or significant value-drivers are observable in active markets.

Level 3 − Model-derived valuations in which one or more significant inputs or significant

value-drivers are unobservable.

Income Taxes

The Company determines its deferred tax provision under the liability method, under which deferred tax

assets and liabilities are recognized for the expected tax consequences of temporary differences between

the tax basis of assets and liabilities and their reported amounts using presently enacted tax rates.

Deferred tax assets are recognized for tax credits and net operating loss carryforwards, reduced by a

valuation allowance, which is established when it is more likely than not that some portion or all of the

deferred tax assets will not be realized. The effect on deferred tax assets and liabilities of a change in tax

rates is recognized in income in the period that includes the enactment date.

A taxing authority may challenge positions that the Company adopted in its income tax filings. Accordingly,

the Company may apply different tax treatments for transactions in filing its income tax returns than for

income tax financial reporting. The Company regularly assesses its tax positions for such transactions and

records reserves for those differences when considered necessary. Tax positions are recognized only when

it is more likely than not, based on technical merits, that the positions will be sustained upon examination.

Tax positions that meet the more-likely-than-not threshold are measured using a probability weighted

approach as the largest amount of tax benefit that is greater than fifty percent likely of being realized upon

settlement. Whether the more-likely-than-not recognition threshold is met for a tax position is a matter of

judgment based on the individual facts and circumstances of that position evaluated in light of all available

evidence. The Company recognizes interest and penalties related to unrecognized tax benefits within

income tax expense in the accompanying consolidated statement of operations. Accrued interest and

penalties are included within the related tax liability line in the consolidated balance sheet.

Provision for U.S. income taxes on undistributed earnings of foreign subsidiaries is made only on those

amounts in excess of the funds considered to be permanently reinvested.

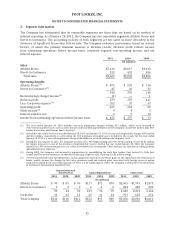

43