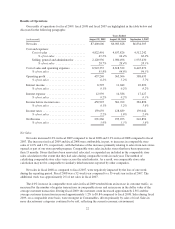

Family Dollar 2009 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2009 Family Dollar annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Property and Equipment:

We state property and equipment at cost. We calculate depreciation for financial reporting purposes using

the straight-line method over the estimated useful lives of the related assets. For leasehold improvements, this

depreciation is over the shorter of the term of the related lease (generally five years) or the asset’s useful

economic life. The valuation and classification of these assets and the assignment of useful depreciable lives

involves significant judgments and the use of estimates. We generally do not assign salvage value to property and

equipment. We review property and equipment for impairment whenever events or changes in circumstances

indicate that the carrying amount of an asset may not be recoverable. Historically, our impairment losses on fixed

assets, which typically relate to normal store closings, have not been material to our financial position and results

of operations. There were no material changes in the estimates or assumptions related to the valuation and

classification of property and equipment during fiscal 2009. See Note 1 and Note 4 to the Consolidated Financial

Statements included in this Report for more information on property and equipment.

Insurance Liabilities:

We are primarily self-insured for health care, property loss, workers’ compensation, general liability, and

auto liability costs. These costs are significant primarily due to the large number of our retail locations and

employees. Our self-insurance liabilities are based on the total estimated costs of claims filed and estimates of

claims incurred but not reported, less amounts paid against such claims, and are not discounted. We review

current and historical claims data in developing our estimates. We also use information provided by outside

actuaries with respect to medical, workers’ compensation, general liability, and auto liability claims. The

insurance liabilities we record are mainly influenced by changes in payroll expense, sales, number of vehicles,

and the frequency and severity of claims. The estimates of more recent claims are more volatile and more likely

to change than older claims. If the underlying facts and circumstances of the claims change or the historical trend

is not indicative of future trends, then we may be required to record additional expense or a reduction to expense,

which could be material to our reported financial condition and results of operations. Our liabilities for workers’

compensation, general liability, and auto liability costs were $210.1 million as of the end of fiscal 2009 and

$202.8 million as of the end of fiscal 2008. There were no other material estimates for insurance liabilities during

fiscal 2009 or fiscal 2008. Our insurance expense during fiscal 2009 and fiscal 2008 was impacted by changes in

our liabilities for workers’ compensation, general liability, and auto liability costs. See our discussion of SG&A

expenses under Results of Operations above for more information.

Contingent Income Tax Liabilities:

We are subject to routine income tax audits that occur periodically in the normal course of business. Our

contingent income tax liabilities are estimated based on the methodology prescribed in FASB Interpretation

No. 48, “Accounting for Uncertainty in Income Taxes” (“FIN 48”), which we adopted as of the beginning of

fiscal 2008. FIN 48 prescribes a minimum recognition threshold a tax position is required to meet before being

recognized in the financial statements. Our liabilities related to uncertain tax positions require an assessment of

the probability of the income-tax-related exposures and settlements and are influenced by our historical audit

experiences with various state and federal taxing authorities as well as by current income tax trends. If

circumstances change, we may be required to record adjustments that could be material to our reported financial

condition and results of operations. Our liabilities related to uncertain tax positions were $39.4 million as of the

end of fiscal 2009 and $39.2 million as of the end of fiscal 2008. There were no material changes in the estimates

or assumptions used to determine contingent income tax liabilities during fiscal 2009. See Note 7 to the

Consolidated Financial Statements included in this Report for more information on our contingent income tax

liabilities.

Contingent Legal Liabilities:

We are involved in numerous legal proceedings and claims. Our accruals, if any, related to these

proceedings and claims are based on a determination of whether or not the loss is both probable and

30