Advance Auto Parts 2001 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2001 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29

|

|

46 ADVANCE AUTO PARTS ANNUAL REPORT 2001 ADVANCE AUTO PARTS ANNUAL REPORT 2001 47

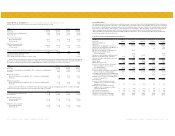

Net Sales

Net sales consist primarily of comparable store sales, new store net

sales, service net sales, net sales to the wholesale dealer network and

finance charges on installment sales. Comparable store sales is

calculated based on the change in net sales starting once a store has

been open for 13 complete accounting periods (each period represents

four weeks). Relocations are included in comparable store sales from the

original date of opening. Each Parts America store that was acquired in

the Western merger and subsequently converted to an Advance Auto

Parts store has been included in the comparable store sales calculation

after 13 complete accounting periods following the completion of its

physical conversion to an Advance Auto Parts store. Additionally, the

stores acquired in the Carport and Discount acquisitions will be

included in the comparable store sales calculation following thirteen

complete accounting periods following their system conversion to the

Advance Auto Parts store system. We do not include net sales from the

Western Auto retail stores in our comparable store sales calculation.

Cost of Sales

Our cost of sales includes merchandise costs and warehouse and

distribution expenses as well as service labor costs of our Western Auto

stores. Gross profit as a percentage of net sales may be affected by

variations in our product mix, price changes in response to competitive

factors and fluctuations in merchandise costs and vendor programs.

We seek to avoid fluctuation in merchandise costs by entering into

long-term purchasing agreements with vendors in exchange for

pricing certainty.

Selling, General and Administrative Expenses

Selling, general and administrative expenses are comprised of store

payroll, store occupancy (including rent), net advertising expenses, other

store expenses and general and administrative expenses, including

salaries and related benefits of corporate employees, administrative

office expenses, data processing, professional expenses and other related

expenses. We lease substantially all of our stores.

Fiscal 2001 Compared to Fiscal 2000

Net sales for 2001 were $2,517.6 million, an increase of $229.6 million,

or 10.0%, over net sales for 2000. Net sales for the retail segment

increased $252.4 million, or 11.6%. The net sales increase for the retail

segment was due to an increase in comparable store sales of 6.2%, sales

from the recently acquired Discount stores and contributions from new

stores opened within the last year. The comparable store sales increase

of 6.2% was a result of growth in both the DIY and DIFM market

segments, as well as the continued maturation of new stores. Net sales

for the wholesale segment decreased $22.8 million due to a decline in

the number of dealer stores we serviced and lower average sales to

each dealer.

During 2001, we opened 110 new stores (including the 30 net stores

from the Carport acquisition in April 2001), relocated 18 stores and

closed 24 stores. Additionally, we acquired 671 stores in the Discount

acquisition in November 2001 and closed two of these stores in

December 2001, bringing the total number of stores to 2,484. We have

increased the number of our stores participating in our commercial

delivery program to 1,370, primarily as a result of adding 167 Discount

stores with existing commercial delivery programs. Additionally, as of

December 29, 2001, we supplied approximately 470 independent dealers

through the wholesale dealer network.

Gross profit for 2001, excluding non-recurring charges associated

with our supply chain initiatives, was $1,076.0 million, or 42.7% of net

sales, as compared to $895.9 million, or 39.2% of net sales, in 2000.

The change in accounting principle accounted for approximately 220

basis points of the increase with the remaining increase attributable to

positive shifts in product mix. The $8.3 million net gain recorded as a

reduction to cost of sales during the first quarter of 2001 as a result of a

vendor contract settlement was equally offset by higher cost of sales

during the last three quarters of 2001 as a result of the new supplier

contract. The gross profit for the retail segment, excluding non-recurring

charges associated with our supply chain initiatives, was $1,062.0

million, or 43.9% of net sales, for 2001, as compared to $881.0 million,

or 40.7% of net sales, in 2000. The increase in gross profit was

primarily attributable to the change in accounting principle and positive

shifts in product mix.

Selling, general and administrative expenses, before merger and

integration expenses, non-recurring charges and non-cash stock option

compensation expense increased to $947.5 million, or 37.6% of net

sales for 2001, from $801.5 million, or 35.0% of net sales for 2000. The

change in accounting principle accounted for approximately 220 basis

points of the increase with the remaining increase attributable to

increased investment in store staffing and retention initiatives, which

were put in place in the third quarter of 2000, and higher insurance costs

due to adverse changes in the insurance market.

EBITDA (operating income plus depreciation and amortization), as

adjusted for merger and integration expenses, expenses associated with

our supply chain initiatives, restructuring expenses, devaluation of assets

held for sale and non-cash and other employee compensation, was $199.7

million in 2001 or 7.9% of net sales, as compared to $161.9 million, or

7.1% of net sales, in 2000. EBITDA is not intended to represent cash

flow from operations as defined by GAAP, and should not be considered

as a substitute for net income as an indicator of operating performance or

as an alternative to cash flow (as measured by GAAP) as a measure of

liquidity. Our method for calculating EBITDA may differ from similarly

titled measures reported by other companies. We believe certain non-

recurring charges, non-cash and other employee compensation, and

merger and integration expenses, should be eliminated from the EBITDA

calculation to evaluate our operating performance.

Interest expense for 2001 was $61.9 million, or 2.5% of net sales, as

compared to $66.6 million, or 2.9% of net sales, in 2000. The decrease

in interest expense was a result of lower average outstanding borrowings

and a decrease in average interest rates over 2000.

Our effective income tax rate was 39.7% of pre-tax income for 2001,

as compared to 38.8% for 2000. This increase is a result of an increase

in the amount of permanent differences between book and tax reporting

treatment on total income tax expense.

We recorded an extraordinary loss on the extinguishment of debt

during the fourth quarter of 2001. This loss is the result of the write-off

of $3.7 million, net of $2.4 million income taxes, or $0.13 loss per

diluted share, of deferred debt issuance costs associated with refinancing

our credit facility in connection with the Discount acquisition.

We also recorded a loss of $2.1 million, net of $1.4 million of

income taxes, or $0.07 loss per diluted share, for the cumulative effect

of a change in accounting principle during the fourth quarter of 2001.

This change in accounting principle is a result of our change in

accounting method related to certain cooperative advertising funds

received from vendors. This change resulted in the reduction of the cost

of inventory acquired from vendors and the resulting costs of sales.

After one-time expenses, we recorded net income of $11.4 million,

or $0.39 per diluted share, for 2001, as compared to net income of

$19.6 million, or $0.68 per diluted share, for 2000. We recorded certain

one-time expenses in 2001, resulting in a net loss of $0.91 per diluted

share. As a percentage of sales, net income for fiscal 2001 was 0.5% as

compared to 0.8% for 2000.

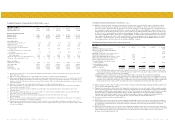

Fiscal 2000 Compared to Fiscal 1999

Net sales for 2000 were $2,288.0 million, an increase of $81.1 million,

or 3.7%, over net sales for 1999. Net sales for the retail segment

increased $149.9 million, or 7.4%. The net sales increase for the retail

segment was due to an increase in the comparable store sales of 4.4%

and contributions from new stores opened within the last year. The

comparable store sales increase of 4.4% was primarily a result of

growth in both the DIY and DIFM market segments, as well as the

continued maturation of new stores and the converted Parts America

stores. Net sales for the wholesale segment decreased 36.3% or $68.8

million due to a decline in the number of dealer stores serviced and

lower average sales to each dealer.

During 2000, we opened 140 new stores, relocated 10 stores and

closed 28 stores, bringing the total retail segment stores to 1,729. At

year end, we had 1,210 stores participating in our commercial delivery

program, a result of adding 116 net stores to the program during 2000.

Additionally, at December 30, 2000, we supplied approximately 590

independent dealers through the wholesale dealer network and our one

store in California.

Gross profit for 2000 was $895.9 million, or 39.2% of net sales, as

compared to $802.8 million, or 36.4% of net sales, in 1999. The gross

profit percentage increased 180 basis points due to the realization of

certain purchasing synergies, fewer product liquidations and a decline

in net sales of the lower margin wholesale segment. Additionally, lower

inventory shrinkage accounted for approximately 60 basis points and

lower logistics costs accounted for approximately 30 basis points of the

increased gross profit margin. The higher shrinkage and logistics costs

in 1999 were related to merchandise conversions and product

liquidations resulting from the Western merger. The gross profit for the

retail segment was $881.0 million, or 40.7% of net sales, for 2000, as

compared to $792.0 million, or 39.3% of net sales, for 1999. During

the fourth quarter of 2000, we recorded a gain as a reduction to cost of

sales of $3.3 million related to a lawsuit against a supplier. The gain

represents actual damages incurred under an interim supply agreement

with the supplier, which provided for higher merchandise costs.

Subsequent to December 30, 2000, we agreed to a cash settlement of

$16.6 million from the supplier. The remainder of the cash settlement

over the originally recorded gain, reduced by higher product costs

incurred under the interim supply agreement and fees and expenses

related to the settlement of the matter, was recognized as an $8.3

million reduction to cost of sales during the first quarter of 2001.

Selling, general and administrative expenses, before impairment of

assets held for sale, integration expenses and non-cash stock option

compensation, increased to $801.5 million, or 35.0% of net sales, for

2000, from $740.5 million, or 33.5% of net sales, for fiscal 1999. The

increase in selling, general and administrative expenses primarily is

attributable to the continued sales decline in the wholesale segment,

which carries lower selling, general and administrative expenses as a

percentage of sales as compared to the retail segment. Additionally, we

incurred higher than expected medical claims as well as higher payroll,

insurance and depreciation expense, partially offset by a decrease in net

advertising costs, as a percentage of sales, as compared to 1999. We

made certain investments in personnel and labor, which we believe are

critical to our long-term success. The increase in depreciation expense

is primarily related to the change in an accounting estimate to reduce

the depreciable lives of certain property and equipment on a

prospective basis.

EBITDA (operating income plus depreciation and amortization), as

adjusted for non-cash and other employee compensation and integration

expenses, was $161.9 million in 2000, or 7.1% of net sales, as

compared to $121.9 million, or 5.5% of net sales, in fiscal 1999.

EBITDA is not intended to represent cash flow from operations as

defined by GAAP and should not be considered as a substitute for net

income as an indicator of operating performance or as an alternative to

cash flow (as measured by GAAP) as a measure of liquidity. Our

method for calculating EBITDA may differ from similarly titled

measures reported by other companies. We believe certain non-

recurring charges, non-cash and other employee compensation, and

merger and integration expenses, should be eliminated from the

EBITDA calculation to evaluate our operating performance.

Interest expense for 2000 was $66.6 million, or 2.9% of net sales, as

compared to $62.8 million, or 2.8% of net sales, for 1999. The increase

in interest expense was a result of an increase in interest rates over

1999, offset by a decrease in net outstanding borrowings. During 2000,

we repurchased $30.6 million of senior subordinated notes on the open

market for $25.0 million.

Our effective income tax rate was 38.8% of pre-tax income for

2000, as compared to 33.2% of pre-tax loss for 1999. This increase is

due to our pre-tax income in 2000 and pre-tax loss in 1999 and the

resulting effect of permanent differences between book and tax

reporting treatment on total income tax expense (benefit). Due to

uncertainties related to the realization of deferred tax assets for certain

net operating loss carryforwards, we recognized additional valuation

allowances of $0.9 million during 2000.

We recorded net income of $19.6 million, or $0.68 per diluted

share, for 2000, as compared to a net loss of $25.3 million, or $0.90 per

diluted share, for 1999. In addition to the items previously discussed,

we also recorded an extraordinary gain related to the early

extinguishment of debt of $2.9 million, or $0.10 per diluted share, net

of $1.8 million provided for income taxes and $0.9 million for the

write-off of associated deferred debt issuance costs. As a percentage of

sales, net income for 2000 was 0.8%, as compared to a net loss of 1.1%

for 1999.