TCF Bank 2006 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2006 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

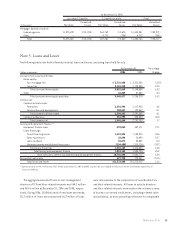

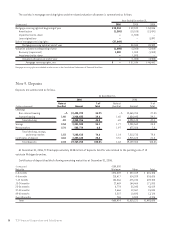

transactions with unrelated persons. The aggregate amount

of loans to executive officers of TCF was $30 thousand and

$115 thousand at December 31, 2006 and 2005, respectively.

In the opinion of management, the above mentioned

loans to outside directors and their related interests and

executive officers do not represent more than a normal

risk of collection.

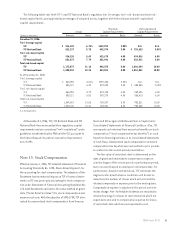

Future minimum lease payments for direct financing and

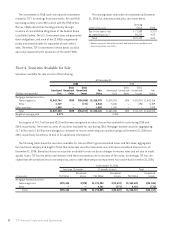

sales-type leases as of December 31, 2006 are as follows.

(In thousands) Total

2007 $ 516,704

2008 364,753

2009 245,090

2010 150,641

2011 75,466

Thereafter 22,189

Total $1,374,843

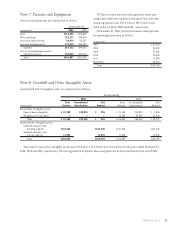

54 TCF Financial Corporation and Subsidiaries

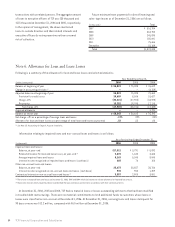

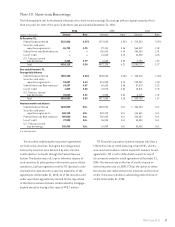

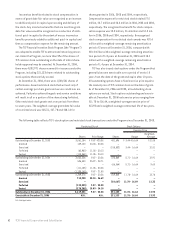

Note 6. Allowance for Loan and Lease Losses

Following is a summary of the allowance for loan and lease losses and selected statistics.

Year Ended December 31,

(Dollars in thousands) 2006 2005 2004

Balance at beginning of year $ 55,823 $ 75,393 $ 76,619

Change in accounting principle(1) –– (4,159)

Adjusted balance at beginning of year 55,823 75,393 72,460

Provision for credit losses 20,689 8,586 18,627

Charge-offs (33,221) (47,904) (34,595)

Recoveries 15,252 19,748 17,110

Net charge-offs (17,969) (28,156) (17,485)

Acquired allowance –– 1,791

Balance at end of year $ 58,543 $ 55,823 $ 75,393

Net charge-offs as a percentage of average loans and leases .17% .29% .20%

Allowance for loan and lease losses as a percentage of total loans and leases at year end .52 .55 .80

(1) See Note 25: Accounting for Deposit Account Overdrafts.

Information relating to impaired loans and non-accrual loans and leases is as follows.

At or For the Year Ended December 31,

(In thousands) 2006 2005 2004

Impaired loans and leases:

Balance, at year-end $17,512 $ 3,791 $ 8,092

Related allowance for loan and lease losses, at year-end(1) 2,470 1,642 3,668

Average impaired loans and leases 8,169 5,345 9,840

Interest income recognized on impaired loans and leases (cash basis) 603 76 108

Other non-accrual loans and leases:

Balance, at year-end 25,673 25,857 38,786

Interest income recognized on non-accrual loans and leases (cash basis) 978 960 1,409

Contractual interest on non-accrual loans and leases(2) 3,557 2,900 3,881

(1) There were no impaired loans and leases at December 31, 2006, 2005 and 2004 which did not have a related allowance for loan and lease losses.

(2) Represents interest which would have been recorded had the loans and leases performed in accordance with their contractual terms.

At December 31, 2006, 2005 and 2004, TCF had no material loans or leases outstanding with terms that had been modified

in troubled debt restructurings. There were no material commitments to lend additional funds to customers whose loans or

leases were classified as non-accrual at December 31, 2006. At December 31, 2006, accruing loans and leases delinquent for

90 days or more was $12.2 million, compared with $6.5 million at December 31, 2005.