TCF Bank 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

272006 Form10-K

a $1.4 million increase in foreclosed real estate expense

primarily due to net losses on sales in 2006 versus net

recoveries in 2005. In 2005, other non-interest expense

increased $11.4 million, or 8.7%, primarily due to increases

in card processing and issuance expenses related to the

overall increase in card volumes and increases in net real

estate expense as a result of net recoveries on sales of fore-

closed properties in 2004.

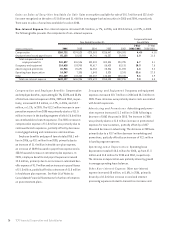

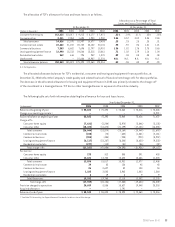

Income Taxes Income tax expense represented 31.41% of

income before income tax expense during 2006, compared

with 30.30% and 33.68% in 2005 and 2004, respectively.

The 2006 effective income tax rate increased over the 2005

rate primarily due to $6.1 million of reductions in income tax

expense in 2006 for favorable developments involving uncer-

tain tax positions, compared with $14 million of reductions

in income tax expense of 2005. Favorable developments

included the closing of certain previous years’ tax returns,

clarification of existing state tax legislation and favorable

developments in income tax audits. The lower effective

income tax rate in 2005, compared with 2004, was the result

of reductions of income tax expense of $14 million related

to favorable developments involving uncertain tax positions

including the closing of certain previous years’ tax returns,

clarification of existing state legislation and favorable

developments in income tax audits.

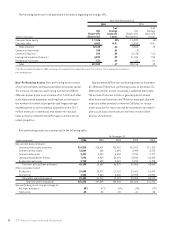

TCF has a Real Estate Investment Trust (“REIT”) and a

related foreign operating company (“FOC”) that acquire,

hold and manage real estate loans and other assets. These

companies are consolidated with TCF Bank and are included

in the consolidated financial statements of TCF Financial

Corporation. The REIT and related companies must meet

specific provisions of the Internal Revenue Code and state

tax laws. If these companies fail to meet any of the required

provisions of federal and state tax laws, TCF’s tax expense

could increase. TCF’s FOC operates under laws in certain

states (including Minnesota and Illinois) that allow FOCs.

Use of REITs and FOCs is and has been the subject of federal

and state audits and tax policy debates by various state

legislatures.

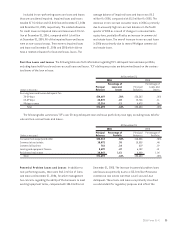

The determination of current and deferred income taxes is

a critical accounting estimate which is based on complex

analyses of many factors including interpretation of federal

and state income tax laws, the differences between the tax

and financial reporting bases of assets and liabilities (tem-

porary differences), estimates of amounts due or owed such

as the timing of reversal of temporary differences and current

financial accounting standards. Additionally, there can be

no assurance that estimates and interpretations used in

determining income tax liabilities may not be challenged by

federal and state taxing authorities. Actual results could

differ significantly from the estimates and tax law interpre-

tations used in determining the current and deferred income

tax liabilities.

In addition, under generally accepted accounting princi-

ples, deferred income tax assets and liabilities are recorded

at the federal and state income tax rates expected to apply

to taxable income in the periods in which the deferred

income tax assets or liabilities are expected to be realized.

If such rates change, deferred income tax assets and liabili-

ties must be adjusted in the period of change through a

charge or credit to income tax expense. Further detail on

income taxes is provided in Note 12 of Notes to Consolidated

Financial Statements.

Consolidated Financial Condition Analysis

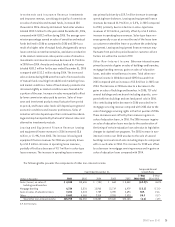

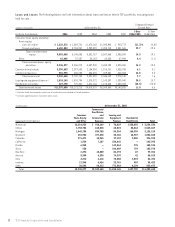

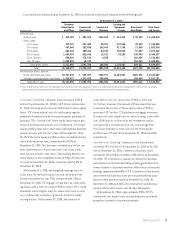

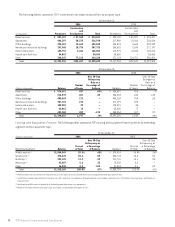

Securities Available for Sale Securities available for

sale increased $167.5 million to $1.8 billion at December

31, 2006. This increase reflects purchases of $397.5 million

of mortgage-backed securities, and normal payment and

prepayment activity. At December 31, 2006, the increase

in mortgage-backed securities partially offsets the declines

in residential loans in the treasury services portfolio. TCF’s

securities available for sale portfolio primarily included

fixed-rate mortgage-backed securities. Net unrealized pre-

tax losses on securities available for sale totaled $33.3 mil-

lion at December 31, 2006, compared with net unrealized

pre-tax losses of $33.2 million at December 31, 2005. TCF

may, from time to time, sell mortgage-backed securities

and utilize the proceeds to reduce borrowings, fund growth

in loans and leases and for other corporate purposes.