TCF Bank 2006 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2006 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

2006 Form10-K

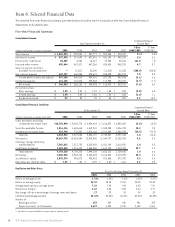

Item 7. Management’s Discussion

and Analysis of Financial Condition

and Results of Operations

Table of Contents Page

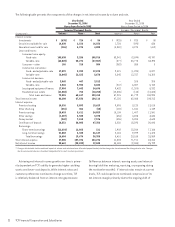

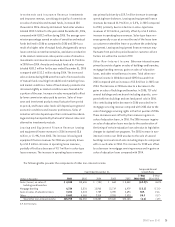

Overview 17

Results of Operations 18

Performance Summary 18

Operating Segment Results 19

Consolidated Income Statement Analysis 19

Net Interest Income 19

Provision for Credit Losses 23

Non-Interest Income 23

Non-Interest Expense 26

Income Taxes 27

Consolidated Financial Condition Analysis 27

Securities Available for Sale 27

Loans and Leases 28

Allowance for Loan and Lease Losses 31

Non-Performing Assets 34

Past Due Loans and Leases 35

Potential Problem Loans and Leases 35

Liquidity Management 36

Deposits 36

Branches 37

Borrowings 37

Contractual Obligations and Commitments 38

Stockholders’ Equity 39

Summary of Critical Accounting Estimates 39

Recent Accounting Developments 39

Fourth Quarter Summary 39

Legislative, Legal and Regulatory Developments 40

Forward-Looking Information 40

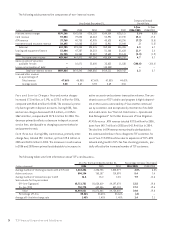

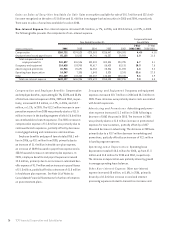

Management’s discussion and analysis of the consolidated

financial condition and results of operations of TCF Financial

Corporation (“TCF” or the “Company”) should be read in

conjunction with the consolidated financial statements in

Item 8 and selected financial data in Item 6.

Overview

TCF, a Delaware corporation, is a financial holding company

based in Wayzata, Minnesota. Its principal subsidiaries, TCF

National Bank and TCF National Bank Arizona, collectively “TCF

Bank,” are headquartered in Minnesota and Arizona and had

453 banking offices in Minnesota, Illinois, Michigan, Colorado,

Wisconsin, Indiana and Arizona at December 31, 2006.

TCF provides convenient financial services through

multiple channels in its primary banking markets. TCF has

developed products and services designed to meet the

needs of all consumers. The Company focuses on attracting

and retaining customers through service and convenience,

including branches that are open seven days a week and on

most holidays, extensive full-service supermarket branches,

automated teller machine (“ATM”) networks and telephone

and internet banking. TCF’s philosophy is to generate inter-

est income, fees and other revenue growth through business

lines that emphasize higher yielding assets and low or no

interest-cost deposits. The Company’s growth strategies

include new branch expansion and the development of new

products and services. New products and services are

designed to build on existing businesses and expand into

complementary products and services through strategic

initiatives.

TCF’s core businesses include retail banking; commercial

banking; small business banking; consumer lending; leasing

and equipment finance; and investments and insurance serv-

ices. The retail banking business includes traditional and

supermarket branches, campus banking, EXPRESS TELLER

ATMs and Visa U.S.A. Inc. (“Visa”) cards.

TCF emphasizes the checking account as its anchor

account, which provides opportunities to cross-sell other

convenient products and services and generate additional

fee income. The continued growth of deposit accounts is

a significant part of TCF’s growth strategy. Total deposit

accounts were 2,426,616, 2,296,199 and 2,216,013 at

December 31, 2006, December 31, 2005 and December 31,

2004, respectively.

Opening new branches is an integral part of TCF’s growth

strategy for generating new deposit accounts and the related

revenue that is associated with the accounts and other

products. New branches typically produce net losses during

the first two to three years of operations before they become

profitable, and therefore the level and timing of new branch

expansion can have a significant impact on TCF’s profitabil-

ity. TCF’s growth in checking accounts is primarily occurring

in new branches with growth in mature branches being slower.

TCF’s expansion is dependent on the continued long-term

success and viability of branch banking.

TCF’s lending strategy is to originate high credit quality,

primarily secured, loans and leases. Commercial loans are

generally made on local properties or to local customers.

TCF’s largest core lending business is its consumer home equity

loan operation, which offers fixed- and variable-rate loans

17