TCF Bank 2006 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2006 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

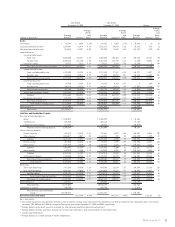

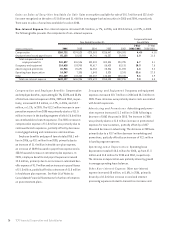

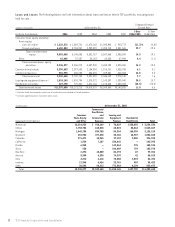

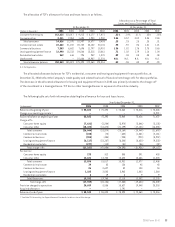

The leasing and equipment finance portfolio increased

$314.4 million from December 31, 2005 to $1.8 billion at

December 31, 2006. Total loan and lease originations and

purchases for TCF Equipment Finance and Winthrop Resources

were $1.1 billion for 2006, compared with $845.8 million

for 2005. The backlog of approved transactions increased

slightly to $249.7 million at December 31, 2006, from $249.2

million at December 31, 2005. TCF’s leasing activity is subject

to risk of cyclical downturns and other adverse economic

developments. In an adverse economic environment, there

may be a decline in the demand for some types of equipment,

resulting in a decline in the amount of new equipment being

placed into service as well as a decline in equipment values

for equipment previously placed in service. Declines in value

of equipment under lease increase the potential for impair-

ment losses and credit losses, due to diminished collateral

value, and may result in lower sales-type revenue at the end

of the contractual lease term. See Note 1 to Consolidated

Financial Statements-Policies Related to Critical Accounting

Estimates for information on lease accounting.

At December 31, 2006 and 2005, $53.7 million, and

$55.2 million, respectively, of TCF’s lease portfolio, were

discounted on a non-recourse basis with third-party financial

institutions and consequently TCF retains no credit risk on

such amounts. The leasing and equipment finance portfolio

tables above include lease residuals. Lease residuals

represent the estimated fair value of the leased equipment

at the expiration of the initial term of the transaction and

are reviewed on an ongoing basis. Any downward revisions

are recorded in the periods in which they become known.

At December 31, 2006, lease residuals totaled $34.7 million,

compared with $32.9 million at December 31, 2005.

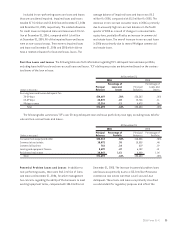

Residential Real Estate Residential real estate loans

were $627.8 million at December 31, 2006, down $142.7 mil-

lion from December 31, 2005.

The decline in residential real estate loans during 2006

was due to normal amortization of loan balances and loan

prepayments. Management expects that the residential

loan portfolio will continue to decline, which will provide

funding for anticipated growth in other loan, lease or invest-

ment categories. At December 31, 2006, TCF’s residential real

estate loan portfolio was $522.1 million in fixed-rate loans

and $105.7 million in adjustable-rate loans.

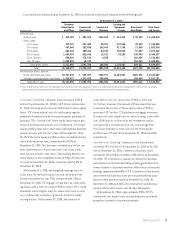

Allowance for Loan and Lease Losses The determina-

tion of the allowance for loan and lease losses is a critical

accounting estimate. TCF’s methodologies for determining

and allocating the allowance for loan and lease losses

focus on ongoing reviews of larger individual loans and

leases, historical net charge-offs, delinquencies in the loan

and lease portfolio, the level of impaired and non-perform-

ing assets, values of underlying loan and lease collateral,

the overall risk characteristics of the portfolios, changes

in character or size of the portfolios, geographic location,

prevailing economic conditions and other relevant factors.

The various factors used in the methodologies are reviewed

on a periodic basis.

31

2006 Form10-K

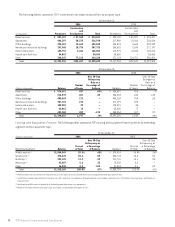

At December 31,

(Dollars in thousands) 2006 2005

Percent Percent

Equipment Type Balance of Total Balance of Total

Specialty vehicles $ 344,855 19.0% $ 257,497 17.1%

Manufacturing 327,057 18.0 277,895 18.5

Construction 310,323 17.1 236,939 15.8

Technology and data processing 260,146 14.3 222,623 14.8

Medical 230,153 12.7 199,729 13.3

Furniture and fixtures 66,999 3.7 60,278 4.0

Printing 65,545 3.6 58,600 3.9

Trucks and trailers 55,241 3.0 56,824 3.8

Material handling 49,722 2.7 39,814 2.6

Other 108,124 5.9 93,595 6.2

Total $1,818,165 100.0% $1,503,794 100.0%