Sharp 2013 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2013 Sharp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

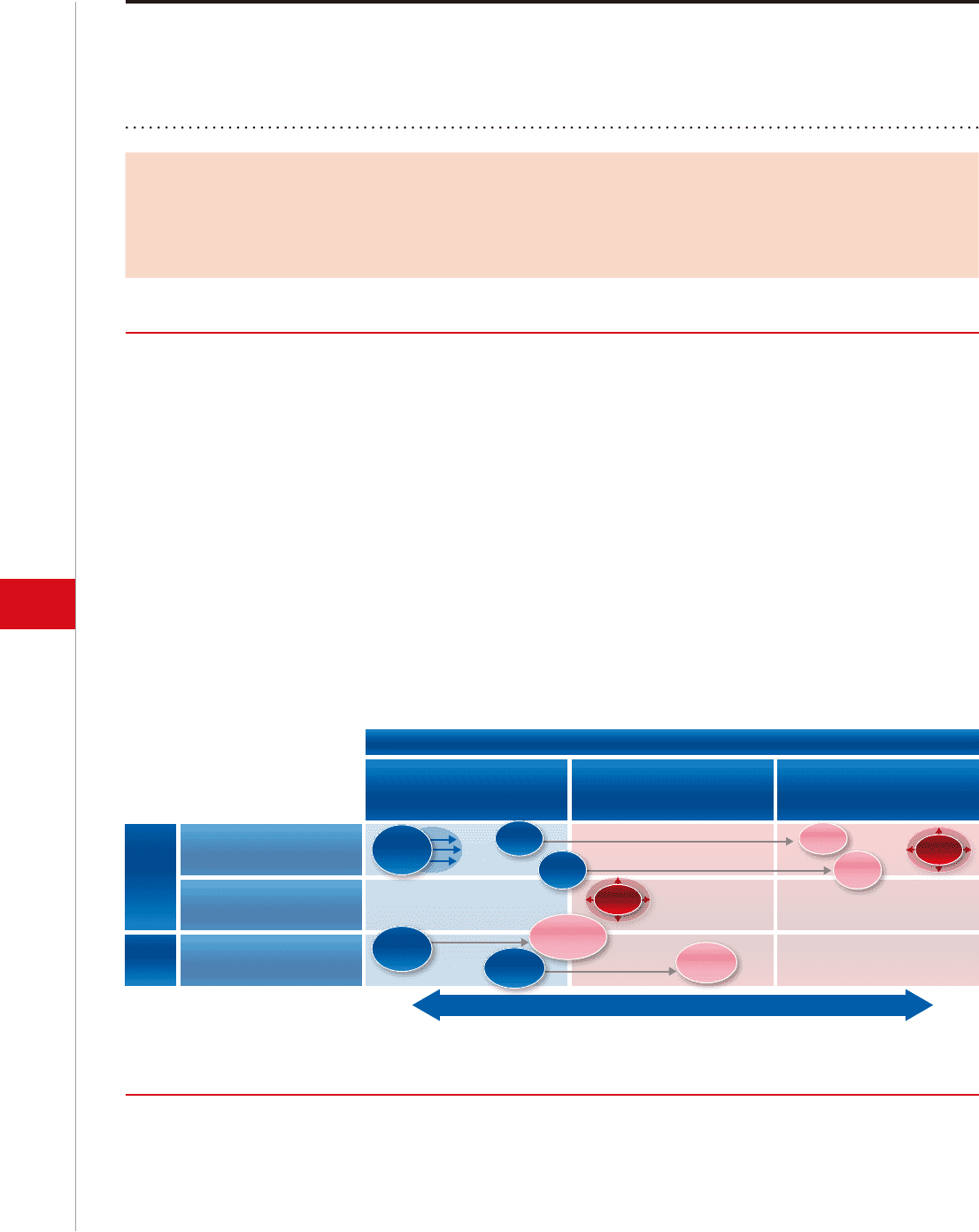

Shift to Value Markets (Compete in Advantageous Fields)

Competition

BtoC Business

Digital

information

equipment

(Audio-Visual)

Small- and

medium-size/

large-size

LCDs Electronic

devices

Fluctuation risk in profitability

High

Communi-

cation

systems

Communi-

cation

systems

Health and

environment

Solar

cells Solar

cells

Business

solutions

BtoB Business

Device Business

Global Value Market

Added value for each customer

type can be pursued

Global Scale-Driven Market

Scale-driven competitiveness

is required

Regional Value Market

Local adaptation for

each region is required

Product Device

Small- and

medium-size

LCDs

Electronic

devices

Low

•LCDTVs

(volumezone)

•Smartphones(high-end)

•Industrial/carapplications

Expandorderswith

ourhighresolutionand

hightechnologymodels

Contributestodifferentia-

tionofcustomersviaswift

responseatearly-stage

conceptdesign

•Smartphones

(volumezone)

•Ultrabook™,

tabletterminals

Controlvolatilitywith

strategicallianceswith

largeclients

6 SHARP CORPORATION

Medium-Term Management Plan for Fiscal 2013-2015: For Recovery and Growth

Five Strategic Measures to Realize Recovery and Growth

1Restructuring our Business Portfolio

Sharp will expand its business in advantageous fields while

controlling fluctuation risk in profitability.

(1) Shift to value markets

(2) Directions of innovation on each business

When considering medium- and long-term growth strategies,

Sharp identified three markets from the perspective of “differ-

ences in competitive environment.”

Global Scale-Driven Market

Scale-driven competitiveness on a global basis is required

Global Value Market

Added value for each customer type can be pursued on a

global scale

Regional Value Market

Local adaptation for each region is required

Digital consumer electronics, such as LCD TVs, and commod-

ity-type devices is a business domain where dominant business

scale in the global market is a key competitive determinant.

Sharp will seek to rebuild its business portfolio by shifting from

this “global scale-driven market” to “value markets” in which a

variety of winning methods exist.

We will minimize fluctuation risk in sales and profits and in-

crease operational stability by allocating core management re-

sources mainly toward “advantageous business domains (tech-

nologies, fields, and regions)” in which we are strong, such as

shifting to high value-added zones including IGZO and MEMS,

and expanding our presence in the domestic solar cell market,

where we have a robust business foundation.

Under the Medium-Term Management Plan, Sharp will under-

take a widespread reassessment of its entire operations with the

aim of concentrating management resources on fields and mar-

kets that it has identified as advantageous.

An urgent priority is to improve the profitability of our TV busi-

ness in Europe, Blu-ray Disc recorder/player businesses, and solar

cell businesses in Europe and the U.S. Here, we will formulate

drastic measures going forward.