Rite Aid 2013 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2013 Rite Aid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

|

|

RITE AID CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

For the Years Ended March 2, 2013, March 3, 2012 and February 26, 2011

(In thousands, except per share amounts)

3. Lease Termination and Impairment Charges (Continued)

have not met their original return on investment projections and have a historical loss of at least

2 years. Their future cash flow projections do not recover their current carrying value. Of this

total, 14, 19 and 43 stores for fiscal years 2013, 2012 and 2011 respectively have been fully

impaired.

(3) These charges are related to the remaining active stores that did not meet the recoverability test

during the current period. These stores have a historical loss of at least 2 years. Their future cash

flow projections do not recover their current carrying value. Of this total, 43, 43 and 141 stores for

fiscal years 2013, 2012 and 2011 respectively have been fully impaired.

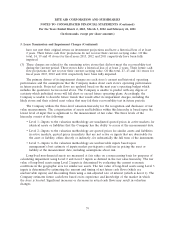

The primary drivers of its impairment charges are each store’s current and historical operating

performance and the assumptions that the Company makes about each store’s operating performance

in future periods. Projected cash flows are updated based on the next year’s operating budget which

includes the qualitative factors noted above. The Company is unable to predict with any degree of

certainty which individual stores will fall short or exceed future operating plans. Accordingly, the

Company is unable to describe future trends that would affect its impairment charges, including the

likely stores and their related asset values that may fail their recoverability test in future periods.

The Company utilizes the three-level valuation hierarchy for the recognition and disclosure of fair

value measurements. The categorization of assets and liabilities within this hierarchy is based upon the

lowest level of input that is significant to the measurement of fair value. The three levels of the

hierarchy consist of the following:

• Level 1—Inputs to the valuation methodology are unadjusted quoted prices in active markets for

identical assets or liabilities that the Company has the ability to access at the measurement date.

• Level 2—Inputs to the valuation methodology are quoted prices for similar assets and liabilities

in active markets, quoted prices in markets that are not active or inputs that are observable for

the asset or liability, either directly or indirectly, for substantially the full term of the instrument.

• Level 3—Inputs to the valuation methodology are unobservable inputs based upon

management’s best estimate of inputs market participants could use in pricing the asset or

liability at the measurement date, including assumptions about risk.

Long-lived non-financial assets are measured at fair value on a nonrecurring basis for purposes of

calculating impairment using Level 2 and Level 3 inputs as defined in the fair value hierarchy. The fair

value of long-lived assets using Level 2 inputs is determined by evaluating the current economic

conditions in the geographic area for similar use assets. The fair value of long-lived assets using Level 3

inputs is determined by estimating the amount and timing of net future cash flows (which are

unobservable inputs) and discounting them using a risk-adjusted rate of interest (which is Level 1). The

Company estimates future cash flows based on its experience and knowledge of the market in which

the store is located. Significant increases or decreases in actual cash flows may result in valuation

changes.

79