Rite Aid 2013 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2013 Rite Aid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

|

|

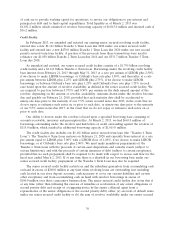

in selling, general and administrative expenses as these audits were related to pre-acquisition periods.

Additionally, the income tax benefit was recorded net of adjustments to maintain a full valuation

allowance against our net deferred tax assets.

ASC 740, ‘‘Income Taxes’’ requires a company to evaluate its deferred tax assets on a regular basis

to determine if a valuation allowance against the net deferred tax assets is required. In determining

whether a valuation allowance is required, we take into account all available positive and negative

evidence with regard to the recognition of a deferred tax asset including our past earnings history,

expected future earnings, the character and jurisdiction of such earnings, unsettled circumstances that,

if unfavorably resolved, would adversely affect recognition of a deferred tax asset, carryback and

carryforward periods, and tax planning strategies that could potentially enhance the likelihood of

realization of a deferred tax asset. A cumulative loss in recent years is significant negative evidence in

considering whether deferred tax assets are realizable. Based on the negative evidence, ASC 740

precludes relying on projections of future taxable income to support the recognition of deferred tax

assets. The ultimate realization of deferred tax assets is dependent upon the existence of sufficient

taxable income generated in the carryforward periods.

The fiscal 2012 income tax benefit of $23.7 million was primarily comprised of adjustments to

unrecognized tax benefits due to the lapse of statute of limitations. The fiscal 2011 income tax expense

of $9.8 million was primarily comprised of an accrual for state and local taxes, adjustments to

unrecognized tax benefits and the need for an accrual of additional state taxes resulting from the

receipt of a final audit determination. We monitor all available evidence related to our ability to utilize

our remaining net deferred tax assets. We maintained a full valuation allowance of $2,224.0 million and

$2,317.4 million against remaining net deferred tax assets at fiscal year end 2013 and 2012, respectively.

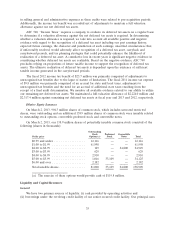

Dilutive Equity Issuances

On March 2, 2013, 904.3 million shares of common stock, which includes unvested restricted

shares, were outstanding and an additional 138.9 million shares of common stock were issuable related

to outstanding stock options, convertible preferred stock and convertible notes.

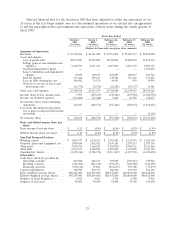

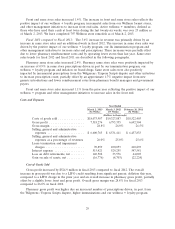

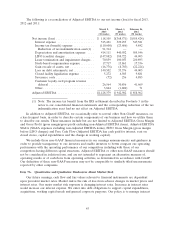

On March 2, 2013, our 138.9 million shares of potentially issuable common stock consisted of the

following (shares in thousands):

Outstanding

Stock Preferred Convertible

Strike price Options(a) Stock Notes Total

$0.99 and under .................. 12,116 — — 12,116

$1.00 to $1.99 ................... 61,998 — — 61,998

$2.00 to $2.99 ................... 149 — 24,800 24,949

$3.00 to $3.99 ................... 629 — — 629

$4.00 to $4.99 ................... 2,910 — — 2,910

$5.00 to $5.99 ................... 1,016 33,109 — 34,125

$6.00 and over ................... 2,182 — — 2,182

Total issuable shares ............... 81,000 33,109 24,800 138,909

(a) The exercise of these options would provide cash of $119.8 million.

Liquidity and Capital Resources

General

We have two primary sources of liquidity: (i) cash provided by operating activities and

(ii) borrowings under the revolving credit facility of our senior secured credit facility. Our principal uses

35