Qantas 2011 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2011 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

61 ANNUAL REPORT 2011

for the year ended 30 June 2011

Notes to the Financial Statements continued

Workers Compensation Insurance

The Qantas Group is a licensed self-insurer under the New South

Wales Workers Compensation Act, the Victorian Accident Compensation

Act and the Queensland Workers Compensation and Rehabilitation

Act. Qantas has made provision for all notied assessed workers

compensation liabilities, together with an estimate of liabilities incurred

but not reported, based on an independent actuarial assessment

discounted using Australian Government bond rates that have maturity

dates approximating the terms of Qantas’ obligations. Workers’

compensation for all remaining employees is commercially insured.

U EARNINGS PER SHARE

Basic earnings per share is determined by dividing the Qantas Group’s

net prot attributable to members of the Qantas Group by the weighted

average number of shares on issue during the current year.

Diluted earnings per share is calculated after taking into account the

number of ordinary shares to be issued for no consideration in relation

to dilutive potential ordinary shares.

V CASH AND CASH EQUIVALENTS

Cash and cash equivalents include cash at bank and on hand, cash

at call and short-term money market securities and term deposits that

are readily convertible to a known amount of cash and are subject to

an insignicant risk of change in value.

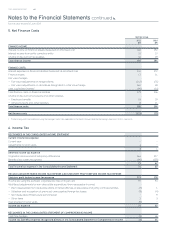

W NET FINANCE COSTS

Net nance costs comprise interest payable on borrowings calculated

using the effective interest method, unwinding of the discount on

provisions and receivables, interest receivable on funds invested,

gains and losses on mark-to-market movement in fair value hedges.

Finance income is recognised in the Consolidated Income Statement

as it accrues, using the effective interest method.

Finance cost is recognised in the Consolidated Income Statement

as incurred, except where interest costs relate to qualifying assets

in which case they are capitalised to the cost of the assets. Qualifying

assets are assets that necessarily take a substantial period of time

to be made ready for intended use. Where funds are borrowed

generally, borrowing costs are capitalised using the average interest

rate applicable to the Qantas Group’s debt facilities.

X INTERESTBEARING LIABILITIES

Interest-bearing liabilities are recognised initially at fair value less

attributable transaction costs. Subsequent to initial recognition,

interest-bearing liabilities are stated at amortised cost, with any

difference between cost and redemption value being recognised

in the Consolidated Income Statement over the period of the

borrowings on an effective interest basis. Interest-bearing liabilities

that are designated as hedged items are subject to measurement

under the hedge accounting requirements.

Y SHARE CAPITAL

Ordinary Shares

Incremental costs directly attributable to issue of ordinary shares are

recognised as a deduction from equity, net of any related income

tax benet.

Repurchase of Share Capital

When share capital recognised as equity is repurchased, the amount

of the consideration paid, including directly attributable costs, is

recognised as a deduction from equity.

Treasury Shares

Shares held by the Qantas sponsored employee share plan trust

are recognised as treasury shares and deducted from equity.

Z COMPARATIVES

Various comparative balances have been reclassied to align with

current year presentation. These amendments have no material

impact on the Financial Statements.

AA NEW STANDARDS AND INTERPRETATIONS NOT YET ADOPTED

The following standards, amendments to standards and interpretations

have been identied as those which may impact the Qantas Group in

the period of initial application. They are available for early adoption

at June , but have not been applied in preparing these

Financial Statements.

— AASB Financial Instruments and consequential amendments

in AASB - Amendments to Australian Accounting Standards

and AASB - Amendments to Australian Accounting Standards

(December ) includes requirements for the classication,

measurement and derecognition of nancial assets and nancial

liabilities. Retrospective application is generally required, although

there are exceptions, particularly if the entity adopts the standard

for the year ended June or earlier. The Qantas Group has

not yet determined the effect of the amendments to AASB , which

will become mandatory for the Qantas Group’s June

Financial Statements

— AASB Related Party Disclosures (revised December )

and amendments in AASB - Amendments to Australian

Accounting Standards simplies and claries the denition of

a related party. The amendments, which will become mandatory

for the Qantas Group’s June Financial Statements with

retrospective application required, are not expected to have

any impact

— AASB - Amendments to Australian Interpretation –

Prepayments of a Minimum Funding Requirement – AASB

make amendments to Interpretation AASB – The Limit on

a Dened Benet Asset, Minimum Funding Requirements removing

an unintended consequence arising from the treatment of the

prepayments of future contributions in some circumstances when

there is a minimum funding requirement. The amendments, which

will become mandatory for the Qantas Group’s June

Financial Statements with retrospective application required, are

not expected to have any impact

— AASB - Amendments to Australian Accounting Standards,

AASB - Further Amendments to Australian Accounting

Standards arising from the Annual Improvements Project and

AASB - Amendments to Australian Accounting Standards

results in minor changes affecting various AASBs. The amendments,

which become mandatory for the Qantas Group’s June

Financial Statements, are not expected to have any impact

— AASB Amended IAS Employee Benets (revised June )

has eliminated the use of the ‘corridor approach’ and instead

mandated immediate recognition of all re-measurements of

dened benet liability (asset) including gains and losses in other

comprehensive income. The amendments, which are generally

to be applied retrospectively, will become mandatory for the

Qantas Group’s June Financial Statements. If the dened

benet balances as at June remained at adoption, the

Qantas Group would report a dened benet liability instead of

a dened benet asset as a result of the immediate recognition

of the unrecognised actuarial losses through other comprehensive

income. Refer to Note for details of dened benet balances as

at June

1. Statement of Signicant Accounting Policies continued