Porsche 2010 Annual Report Download - page 202

Download and view the complete annual report

Please find page 202 of the 2010 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

|

|

Financials

200

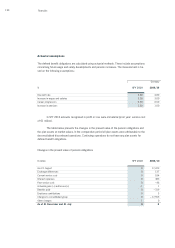

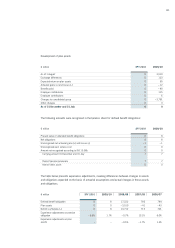

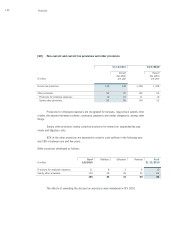

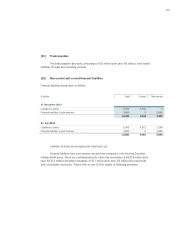

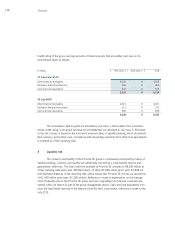

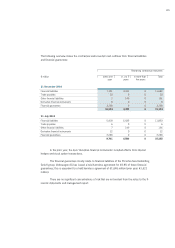

4 Market risk

4.1 Hedging policy and financial derivatives

In the reporting period, the Porsche SE group was exposed to interest rate and stock price

risks as well as risks from put and call options for the remaining shares held by Porsche SE in

Porsche Zwischenholding GmbH. The risks arise from financing activities, the cash-settled options

relating to Volkswagen AG shares which were still held in the reporting year but had been disposed

of in full by the reporting date, changes in the enterprise value of Porsche Zwischenholding GmbH

and to a small extent from cash investments. It is company policy to exclude or limit these risks by

entering into hedge transactions in some cases. All necessary hedging activities are coordinated by

Porsche SE’s finance department.

The nature and volume of hedging transactions is generally chosen with regard to the

hedged item. Hedging transactions may only be concluded to hedge existing underlyings or fore-

cast transactions. Only financial instruments approved by type and volume may be entered into.

There are no significant concentrations of risk that are not evident from the notes to the fi-

nancial statements and management report.

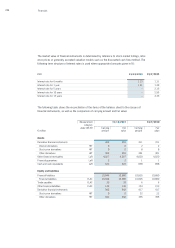

The market price risk from interest hedging and from the put and call option relating to the

shares in Porsche Zwischenholding GmbH remaining with Porsche SE was calculated using a sensi-

tivity analysis. In the comparative period, the market price risk was also presented using a value-at-

risk model for stock price risks.

The sensitivity analysis calculates the effect on equity and profit or loss by modifying risk

variables within the respective market risk. In the value-at-risk calculation, a historical simulation

was used to determine the potential change in market price. The value at risk shows the potential

future loss of a certain portfolio over a predefined period of time (retention period) with certain

probabilities which are not likely to be exceeded. The degree of risk does not, however, give any

information about the distribution and anticipated loss, if it is actually exceeded.