Dollar Tree 2006 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2006 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

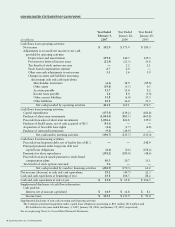

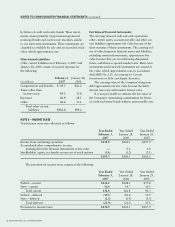

Costs directly associated with warehousing and

distribution are capitalized as merchandise invento-

ries. Total warehousing and distribution costs capital-

ized into inventory amounted to $25.6 million and

$25.3 million at February 3, 2007 and January 28,

2006, respectively.

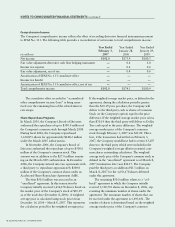

Property, Plant and Equipment

Property, plant and equipment are stated at cost and

depreciated using the straight-line method over the

estimated useful lives of the respective assets as follows:

Buildings 40 years

Furniture, fixtures and equipment 3 to 15 years

Transportation vehicles 4 to 6 years

Leasehold improvements and assets held under

capital leases are amortized over the estimated useful

lives of the respective assets or the committed terms

of the related leases, whichever is shorter. Amortiza-

tion is included in “selling, general and administrative

expenses” on the accompanying consolidated state-

ments of operations.

In the fourth quarter of 2004, the Company

revised its estimate of useful lives on certain store

equipment and distribution center assets. This change

increased net income by approximately $4.0 million in

the first three quarters of 2005 as compared to 2004.

Costs incurred related to software developed for

internal use are capitalized and amortized over three

years. Costs capitalized include those incurred in the

application development stage as defined in Statement

of Position 98-1, Accounting for the Costs of

Computer Software Developed or Obtained for

Internal Use.

Impairment of Long-Lived Assets and Long-Lived

Assets to Be Disposed Of

The Company reviews its long-lived assets and certain

identifiable intangible assets for impairment whenever

events or changes in circumstances indicate that the

carrying amount of an asset may not be recoverable,

in accordance with Statement of Financial Accounting

Standards (SFAS) No. 144, Accounting for the

Impairment or Disposal of Long-Lived Assets.

Recoverability of assets to be held and used is

measured by comparing the carrying amount of an

asset to future net undiscounted cash flows expected

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

to be generated by the asset. If such assets are consid-

ered to be impaired, the impairment to be recognized

is measured as the amount by which the carrying

amount of the assets exceeds the fair value of the

assets based on discounted cash flows or other readily

available evidence of fair value, if any. Assets to be

disposed of are reported at the lower of the carrying

amount or fair value less costs to sell. In fiscal 2006,

2005 and 2004, the Company recorded charges of

$0.5 million, $0.2 million and $0.5 million, respec-

tively, to write down certain assets. These charges

are recorded as a component of “selling, general

and administrative expenses” in the accompanying

consolidated statements of operations.

Intangible Assets

Goodwill and intangible assets with indefinite useful

lives are not amortized, but rather tested for impair-

ment at least annually. Intangible assets with finite use-

ful lives are amortized over their respective estimated

useful lives and reviewed for impairment in accor-

dance with SFAS No. 144. The Company performs its

annual assessment of impairment following the final-

ization of each November’s financial statements.

Financial Instruments

The Company utilizes derivative financial instruments

to reduce its exposure to market risks from changes in

interest rates. By entering into receive-variable, pay-

fixed interest rate swaps, the Company limits its

exposure to changes in variable interest rates. The

Company is exposed to credit-related losses in the

event of non-performance by the counterparty to the

interest rate swaps; however, the counterparties are

major financial institutions, and the risk of loss due

to non-performance is considered remote. Interest rate

differentials paid or received on the swaps are recog-

nized as adjustments to expense in the period earned

or incurred. The Company formally documents all

hedging relationships, if applicable, and assesses

hedge effectiveness both at inception and on an

ongoing basis.

Certain of the Company’s interest rate swaps

have not qualified for hedge accounting treatment

pursuant to the provisions of SFAS No. 133,

Accounting for Derivative Instruments and Hedging

Activities (SFAS 133). These interest rate swaps

are recorded at fair value in the accompanying

32 DOLLAR TREE STORES, INC. • 2006 ANNUAL REPORT