United Healthcare 2012 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2012 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

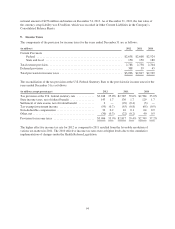

Maturities of commercial paper and long-term debt for the years ending December 31 are as follows:

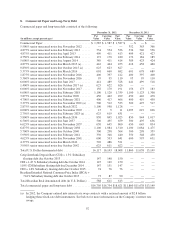

(in millions)

2013 (a) ............................................................................. $2,713

2014 ................................................................................ 920

2015 ................................................................................ 1,175

2016 ................................................................................ 1,152

2017 ................................................................................ 1,281

Thereafter ............................................................................ 9,513

(a) Includes $33 million of debt subject to acceleration clauses.

Long-Term Debt

In August 2012, the Company completed an exchange of $1.1 billion of its zero coupon senior unsecured notes

due November of 2022 for $0.5 billion additional issuance of its 2.875% notes due in March 2022, $0.1 billion

additional issuance of its 4.375% notes due March 2042 and $0.1 billion in cash.

Commercial Paper and Bank Credit Facilities

Commercial paper consists of short-duration, senior unsecured debt privately placed on a discount basis through

broker-dealers. As of December 31, 2012, the Company’s outstanding commercial paper had a weighted-average

annual interest rate of 0.3%.

The Company has $3.0 billion five-year and $1.0 billion 364-day revolving bank credit facility with 21 banks,

which mature in November 2017 and November 2013, respectively. These facilities provide liquidity support for

the Company’s $4.0 billion commercial paper program and are available for general corporate purposes. There

were no amounts outstanding under these facilities as of December 31, 2012. The interest rates on borrowings are

variable based on term and are calculated based on the London Interbank Offered Rate (LIBOR) plus a credit

spread based on the Company’s senior unsecured credit ratings. As of December 31, 2012, the annual interest

rates on both of the credit facilities, had they been drawn, would have ranged from 1.0% to 1.3%.

Debt Covenants

The Company’s bank credit facilities contain various covenants including requiring the Company to maintain a

debt to debt-plus-equity ratio not more than 50%. The Company was in compliance with its debt covenants as of

December 31, 2012.

Interest Rate and Currency Swap Contracts

In 2012, the Company entered into interest rate swap contracts to convert a portion of its interest rate exposure

from fixed rates to floating rates to more closely align interest expense with interest income received on its cash

equivalent and variable rate investment balances. The floating rates are benchmarked to LIBOR. The swaps are

designated as fair value hedges on the Company’s fixed-rate debt. Since the critical terms of the swaps match

those of the debt being hedged, they are assumed to be highly effective hedges and all changes in fair value of the

swaps are recorded as an adjustment to the carrying value of the related debt with no net impact recorded in the

Consolidated Statements of Operations. Both the hedge fair value changes and the offsetting debt adjustments are

recorded in Interest Expense on the Consolidated Statements of Operations. The net fair value of these swaps was

$3 million at December 31, 2012 and is recorded in Other Long-Term Assets for $14 million and Other Long-

Term Liabilities for $11 million in the Consolidated Balance Sheets.

In December 2012, the Company entered into currency swap contracts to hedge the foreign currency exposure on

the principal amount of intercompany borrowings denominated in Brazilian Real. The currency swaps have a

93