U-Haul 2004 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2004 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

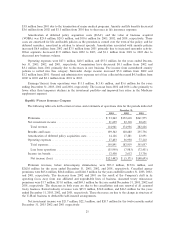

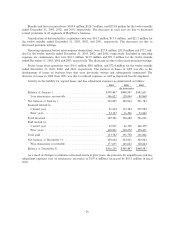

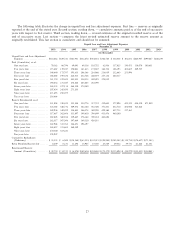

|

|

Accounting policies are considered critical when they are signiÑcant and involve diÇcult, subjective or

complex judgments or estimates. The accounting policies that we deem most critical to us, and involve the

most diÇcult, subjective or complex judgments include the following:

We also have other policies that we consider key accounting policies, such as revenue recognition;

however, these policies do not meet the deÑnition of critical accounting estimates, because they do not

generally require us to make estimates or judgments that are diÇcult or subjective.

Principles of Consolidation

The 2004 balance sheet includes the accounts of AMERCO, its wholly owned subsidiaries, and SAC

Holding II Corporation and its subsidiaries. The 2003 balance sheet and the 2004 statements of operations,

comprehensive income, and cash Öows, and the consolidated Ñnancial statements for Ñscal 2003 and 2002,

include all of those entities plus SAC Holding Corporation and its subsidiaries. In Ñscal 2003 and 2002, SAC

Holding Corporation and SAC Holding II Corporation (the SAC entities) were considered special purpose

entities and were consolidated based on the provision of Emerging Issues Task Force (EITF) Issue No. 90-15.

In Ñscal 2004, the Company applied FASB Interpretation No. 46 to its interests in the SAC Entities. Initially,

the Company concluded that the SAC entities were variable interest entities and that the Company was the

primary beneÑciary. Accordingly, the Company continued to include the SAC entities in the consolidated

Ñnancial statements. In February 2004, SAC Holding Corporation restructured the Ñnancing of three

subsidiaries and then distributed its interest in those subsidiaries to its sole shareholder. This triggered a

requirement to reassess the Company's involvement with those subsidiaries, which led to a conclusion that the

Company ceased to be the primary beneÑciary of those three subsidiaries at that date. In March 2004, SAC

Holding Corporation restructured its Ñnancing, triggering a similar reassessment that led to a conclusion that

the Company ceased to be the primary beneÑciary of SAC Holding Corporation and its remaining

subsidiaries. Accordingly, at the dates the Company ceased to be the primary beneÑciary, it deconsolidated

those entities. The deconsolidation was accounted for as a distribution of the Company's interests to the sole

shareholder of the SAC entities. Because of the Company's continuing involvement with SAC Holding

Corporation and its current and former subsidiaries, the distributions do not qualify as discontinued operations

as deÑned by SFAS No. 144. Inter-company accounts and transactions have been eliminated.

Recoverability of Property, Plant and Equipment

Property, plant and equipment are stated at cost. Interest costs incurred during the initial construction of

buildings or rental equipment are considered part of cost. Depreciation is computed for Ñnancial reporting

purposes principally using the straight-line method over the following estimated useful lives: rental equipment

2-20 years: buildings and non-rental equipment 3-55 years. Major overhauls to rental equipment are

capitalized and are amortized over the estimated period beneÑted. Routine maintenance costs are charged to

operating expense as they are incurred. Gains and losses on dispositions of property, plant and equipment are

netted against depreciation expense when realized. Depreciation is recognized in amounts expected to result in

the recovery of estimated residual values upon disposal (i.e. no gains or losses.) In determining the

depreciation rate, historical disposal experience and holding periods, and trends in the market for vehicles are

reviewed. Due to longer holding periods on trucks and the resulting increased possibility of changes in the

economic environment and market conditions, these estimates are subject to a greater degree of risk.

Reviews are periodically performed to determine whether facts and circumstances exist which indicate

that the carrying amount of assets, including estimates of residual value, may not be recoverable or that the

useful life of assets is shorter or longer than originally estimated. The company assesses the recoverability of

its assets by comparing the projected undiscounted net cash Öows associated with the related asset or group of

assets over their estimated remaining lives against their respective carrying amounts. Impairment, if any, is

based on the excess of the carrying amount over the fair value of those assets. If assets are determined to be

recoverable, but the useful lives are shorter or longer than originally estimated, the net book value of the assets

is depreciated over the newly determined remaining useful lives.

17