Tesco 2007 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2007 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

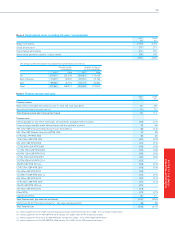

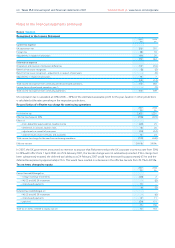

Notes to the Group financial statements continued

Note 1 Accounting policies continued

52 Tesco PLC Annual report and financial statements 2007 Find out more at www.tesco.com/corporate

Deferred tax is calculated at the tax rates that have been enacted

or substantively enacted by the Balance Sheet date. Deferred

tax is charged or credited in the Income Statement, except

when it relates to items charged or credited directly to equity,

in which case the deferred tax is also recognised in equity.

Deferred tax assets are recognised to the extent that it is

probable that taxable profits will be available against which

deductible temporary differences can be utilised.

The carrying amount of deferred tax assets is reviewed at each

Balance Sheet date and reduced to the extent that it is no

longer probable that sufficient taxable profits will be available

to allow all or part of the asset to be recovered.

Deferred tax assets and liabilities are offset against each other

when there is a legally enforceable right to set-off current

taxation assets against current taxation liabilities and it is the

intention to settle these on a net basis.

Foreign currencies

Transactions in foreign currencies are translated at the

exchange rate on the date of the transaction. At each Balance

Sheet date, monetary assets and liabilities that are denominated

in foreign currencies are retranslated at the rates prevailing on

the Balance Sheet date. All differences are taken to the Income

Statement for the period.

The financial statements of foreign subsidiaries are translated

into Pounds Sterling according to the functional currency

concept of IAS 21 ‘The Effects of Changes in Foreign Exchange

Rates’. Since the majority of consolidated companies operate as

independent entities within their local economic environment,

their respective local currency is the functional currency.

Therefore, assets and liabilities of overseas subsidiaries

denominated in foreign currencies are translated at exchange

rates prevailing at the date of the Group Balance Sheet; profits

and losses are translated into Pounds Sterling at average

exchange rates for the relevant accounting periods. Exchange

differences arising, if any, are classified as equity and

transferred to the Group’s translation reserve. Such translation

differences are recognised as income or expenses in the period

in which the operation is disposed of.

Goodwill and fair value adjustments arising on the acquisition

of a foreign entity are treated as assets and liabilities of the

foreign entity and translated at the closing rate.

Financial instruments

Financial assets and financial liabilities are recognised on the

Group’s Balance Sheet when the Group becomes a party to the

contractual provisions of the instrument.

Trade receivables

Trade receivables are non interest-bearing and are recognised

initially at fair value, and subsequently at amortised cost using

the effective interest rate method, reduced by appropriate

allowances for estimated irrecoverable amounts.

Investments

Investments are recognised at trade date. Investments are

classified as either held for trading or available-for-sale, and

are recognised at fair value.

For held for trading investments, gains and losses arising from

changes in fair value are recognised in the Income Statement.

For available-for-sale investments, gains and losses arising

from changes in fair value are recognised directly in equity, until

the security is disposed of or is determined to be impaired,

at which time the cumulative gain or loss previously recognised

in equity is included in the net result for the period. Interest

calculated using the effective interest rate method is

recognised in the Income Statement. Dividends on an

available-for-sale equity instrument are recognised in the

Income Statement when the entity’s right to receive payment

is established.

Financial liabilities and equity

Financial liabilities and equity instruments are classified

according to the substance of the contractual arrangements

entered into. An equity instrument is any contract that gives

a residual interest in the assets of the Group after deducting

all of its liabilities.

Interest-bearing borrowings

Interest-bearing bank loans and overdrafts are initially recorded

at fair value, net of attributable transaction costs. Subsequent

to initial recognition, interest-bearing borrowings are stated at

amortised cost with any difference between cost and

redemption value being recognised in the Income Statement

over the period of the borrowings on an effective interest basis.

Trade payables

Trade payables are non interest-bearing and are stated at

amortised cost.

Equity instruments

Equity instruments issued by the Company are recorded at the

proceeds received, net of direct issue costs.