Tesco 2007 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2007 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

10 Tesco PLC Annual report and financial statements 2007 Find out more at www.tesco.com/corporate

Operating and financial review continued

Operations, resources and relationships

We have continued to make good progress with all four parts

of our strategy:

• grow the core UK business

• become a successful international retailer

• be as strong in non-food as in food, and

• develop retailing services

We have done this by keeping our focus on trying to improve

what we do for customers. We try to make their shopping

experience as easy as possible, lower prices where we can to

help them spend less, give them more choice about how they

shop – in small stores, large stores or on-line, and seek to bring

simplicity and value to sometimes complicated markets.

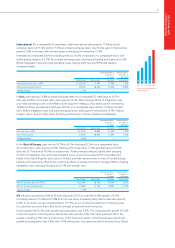

International Despite challenging economic conditions and

political uncertainty in some of our markets, our international

businesses delivered another good performance. Sales growth

has been strong – with like-for-like growth in all but one of our

markets (Hungary being the exception) and profits have again

moved ahead well. Margins continue to improve, despite

absorbing significant integration costs from the in-market

acquisitions we have completed in the year – in the Czech

Republic, Poland and Malaysia.

We are building-out our store networks more rapidly in existing

markets – through a combination of strong organic growth and

acquisitions. 484 stores, with 8.2m sq ft of selling area, were

opened during the year, including 76 hypermarkets. This is

four times the amount of new space opened in the UK. In Rest

of Europe we opened over 4.7m sq ft of space and in Asia

3.5m sq ft.

These numbers included the acquisition of:

• 11 Carrefour stores in the Czech Republic in May 2006 as

part of the asset swap deal announced in September 2005,

plus 27 small stores from Edeka in April, which together

added 1.2m sq ft – or 45% to our space there.

• 146 Leader Price stores in Poland in December, which

added a total of 1.4m sq ft – the equivalent of 29% of

the existing sales area.

• Eight large Makro stores in Malaysia in January, which

added 0.9m sq ft of sales area, nearly doubling our

space in the market.

We are keen to participate further in the process of

consolidation which is now taking place in many International

markets but we are selective purchasers of assets or businesses.

At the end of February, our international operations were

trading from 1,275 stores, including 411 hypermarkets, with a

total of 40.4m sq ft of selling space. Nearly 60% of Group sales

area is now in International. Excluding the United States, we

expect to open 442 new stores in our International markets

during the current year, adding 7.6m sq ft of selling area.

Returns – CROI* All our established markets are now

profitable and with growing local scale, increasing store

maturity and the benefits of investment in central distribution

now flowing, returns from our International operations are

continuing to rise. On a constant currency basis, cash return

on investment (CROI*) for International has increased again

– to 11.5% with our lead markets overall maintaining

significantly higher levels.

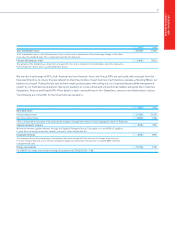

Asia

• In China we trade from 47 hypermarkets, mainly in

Shanghai, and the first stores in China’s other large

regional markets – Guangzhou, Shenzhen and Beijing

(our first Tesco-fascia store) have opened well. Our new

range of over 1,000 Tesco own brand lines have been

well-received by customers. Hymall’s sales have continued

to grow strongly – up overall by 19% in the year, with

strengthening like-for-like sales as the year progressed.

As a result of carrying higher overheads as we invest to

equip the business to grow faster, it made a small loss

after tax and interest, of which our share was £6m.

• In a still subdued retail market in Japan we made progress,

with modest overall sales growth and a stronger like-for-like

performance. Our focus in the year has been on refining

and developing the trial Express-type stores into a

profitable, expandable format and implementing our

‘Tesco in a Box’ suite of operating systems successfully.

We now plan to push on with a much larger opening

programme of up to 35 new stores this year.

• In Korea, Homeplus continued to do well, with solid sales

and very strong profit growth in more challenging market

conditions than in recent years. During the year we opened

29 new stores and, including extensions, almost 1m sq ft

of space. Most of our new selling area came from large

hypermarkets, but our development programme is now

broadly-based with nearly 20% coming from store

extensions, 21% from compact hypermarkets and the

remainder from the roll-out of our successful Express

convenience format, which now has almost 40 stores

trading. We have a strong forward pipeline of new space,

including plans to double the size of the Express business.

* Cash return on investment (CROI) is measured as earnings before interest, tax,

depreciation and amortisation, expressed as a percentage of net invested capital.