Redbox 2004 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2004 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

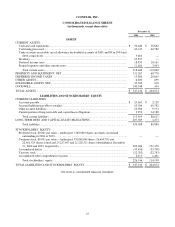

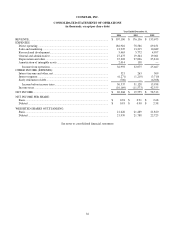

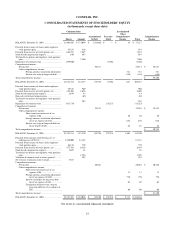

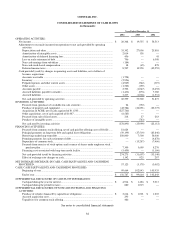

COINSTAR, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS –(Continued)

YEARS ENDED DECEMBER 31, 2004, 2003, AND 2002

43

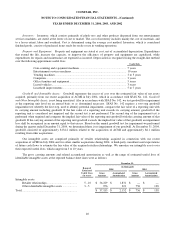

Recent accounting pronouncements: In January 2003, the Financial Accounting Standards Board (“FASB”) issued

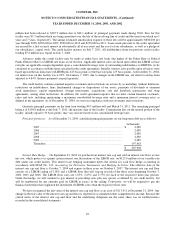

FASB Interpretation No. 46, Consolidation of Variable Interest Entities (“FIN 46”) and in December 2003 issued FIN 46R.

FIN 46 requires the consolidation of variable interest entities which have one or both of the following attributes (1) the equity

investment at risk is not sufficient to permit the entity to finance its activities without additional financial support from other

parties which is provided by other parties that will absorb some or all of the expected losses of the entity, (2) the equity

investors lack controlling financial interest as evidenced by (i) the ability to make decisions regarding the entity’s activities

through voting or similar rights (ii) the obligation to absorb expected losses, which make it possible for the entity to finance

its activities and (iii) the right to receive expected residual returns of the entity if they occur, which is the compensation for

absorbing the expected losses. FIN 46 was immediately effective for variable interest entities formed after January 31, 2003.

FIN 46R requires the adoption of either FIN 46 or FIN 46R in financial statements of public entities that have interests in

structures that are commonly referred to as special purpose entities for periods ending after December 15, 2003. Application

for all other types of variable interest entities is required in financial statements for periods ending after March 15, 2004. The

adoption of FIN 46 and FIN 46R did not have an effect on our financial position or results of operations.

In December 2004, the FASB issued Statement of Financial Accounting Standards No. 123 (revised 2004), Share-

Based Payment (“SFAS 123R”). SFAS 123R will require that the compensation cost relating to share-based payment

transactions be recognized in financial statements. That cost will be measured based on the fair value of the equity or liability

instruments issued. SFAS 123R covers a wide range of share-based compensation arrangements including share options,

restricted share plans, performance-based awards, share appreciation rights and employee share purchase plans. SFAS 123R

replaces FASB 123, Accounting for Stock Issued to Employees. SFAS 123R will be effective for us for our third fiscal quarter

ending September 30, 2005. We are in process of evaluating the impact of adopting SFAS 123R and of determining the

impact on our results of operations or financial position.

Reclassifications: Certain reclassifications have been made to the prior period balances to conform to the current

period presentation.

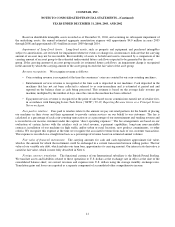

NOTE 3: ACQUISITIONS

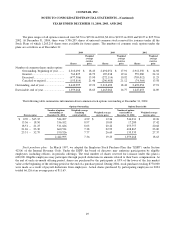

ACMI Holdings, Inc.: On July 7, 2004, we acquired ACMI for $235.0 million. As part of this acquisition, we

acquired cash totaling $11.5 million. The acquisition was effected pursuant to the “Agreement and Plan of Merger” dated

May 23, 2004 between ACMI and Coinstar. In addition to the purchase price, we incurred an estimated $4.3 million in

transaction costs, including investment banking fees and amounts relating to legal and accounting charges. The results of

operations of ACMI from July 7, 2004 to December 31, 2004 are included in our statement of operations.

ACMI offers various entertainment services to consumers in mass merchandisers, supermarkets, warehouse clubs,

restaurants, entertainment centers, truck stops and other distribution channels. These entertainment services include skill-

crane machines, bulk vending, kiddie rides and video games. We acquired ACMI in order to add new classes of trade,

broaden our retailer base, diversify services, expand the reach of field service and create a platform for growth across all

businesses, including coin-counting, e-payment and entertainment services.

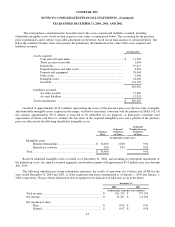

The total purchase consideration for the acquisition of ACMI consists of the following:

(in thousands)

Cash paid for acquisition of ACMI

(1)................................................................................................................................

...........

$ 235,000

Estimated acquisition related costs

(2) ................................................................................................................................

...........

4,295

$ 239,295

(1)

As part of the acquisition, we acquired cash, cash equivalents and cash-in-machine of approximately $11.5 million.

(2)

Acquisition related costs consist of investment banking, legal and accounting fees and other directly related charges.