Qantas 2016 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2016 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

Notes to the Financial Statements continued

For the year ended 30 June 2016

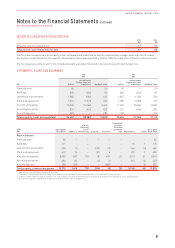

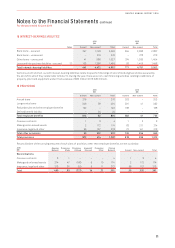

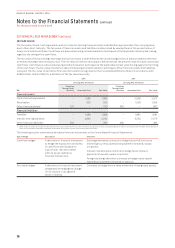

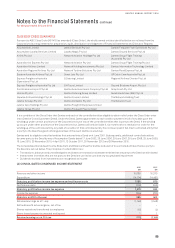

20 FINANCIAL RISK MANAGEMENT CONTINUED

iv. Fuel Price Risk

Nature of the Risk:

Exposure of future AUD fuel costs to unfavourable USD denominated price movements.

Management of Future AUD Fuel Costs Risk:

The Qantas Group uses options and swaps on jet kerosene, gasoil and crude oil to hedge exposure to movements in the USD price of

aviation fuel. Qantas considers the crude component to be a separately identifiable and measureable component of aviation fuel.

The foreign exchange risk in the total fuel cost is separately hedged using foreign exchange contracts and currency options. Hedging

is conducted in accordance with Qantas Group policy. Fuel consumption out to two years may be hedged within specific parameters,

with any hedging outside these parameters requiring approval by the Board. For the year ended 30 June 2016, other financial assets

and liabilities included fuel and foreign exchange derivatives totalling $70 million (net asset) (2015: $120 million (net asset)). These

are recognised at fair value in accordance with AASB 9.

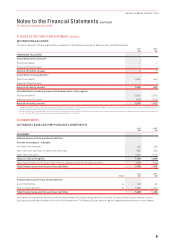

The table below summarises the gain/(loss) impact to Profit Before Tax and Equity Before Tax as a result of a movement in AUD fuelcosts:

Sensitivity to Foreign Exchange and Fuel Price Risk:

Profit Before Tax Equity (Before Tax)

$M 2016 2015 2016 2015

20% movement in AUD fuel costs1

20% (2015: 20%) USD depreciation, 20% (2015: 20%) increase per barrel in fuel indices – – 12 (26)

20% (2015: 20%) USD appreciation, 20% (2015: 20%) decrease per barrel in fuel indices – – 234 519

1. Sensitivity analysis assumes hedge designations as at 30 June 2016 remain unchanged and that all designations are effective. Sensitivity analysis on foreign currency pairs and fuel

indices of 20 per cent represent recent volatile market conditions. Sensitivity analysis assumes an offset between USD and fuel price indices based on observed market movements.

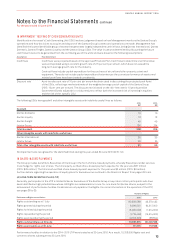

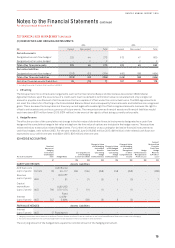

v. Credit Risk

Nature of the Risk:

Credit risk is the potential loss from a transaction in the event of default by the counterparty during the term of the transaction

oron settlement of the transaction. Credit exposure is measured as the cost to replace existing transactions should a

counterpartydefault.

Management of Credit Risk:

The Qantas Group conducts transactions with the following major types of counterparties:

–Trade debtor counterparties: the credit risk is the recognised amount, net of any impairment losses. As at 30 June 2016, trade

debtors amounted to $656 million (2015: $710 million). The Qantas Group has credit risk associated with travel agents, industry

settlement organisations and credit provided to direct customers. The Qantas Group minimises this credit risk through the

application of stringent credit policies and accreditation of travel agents through industry programs.

–Other financial asset counterparties: the Qantas Group restricts its dealings to counterparties that have acceptable credit

ratings. Should the rating of a counterparty fall below certain levels, internal policy dictates that approval by the Board is required

to maintain the level of the counterparty exposure.

The Qantas Group minimises the concentration of credit risk by undertaking transactions with a large number of customers and

counterparties in various countries in accordance with Board-approved policy. As at 30 June 2016, the credit risk of the Qantas

Group to counterparties in relation to other financial assets, cash and cash equivalents, and other financial liabilities amounted to

$1,811million (2015: $2,963 million). Refer to note 20 (C) for offsetting disclosures of contractual arrangements. The Qantas Group’s

credit exposure in relation to these assets is with counterparties that have a minimum credit rating of A-/A3, unless individually

approved by the Board.

77

QANTAS ANNUAL REPORT 2016