Proctor and Gamble 2006 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2006 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

|

|

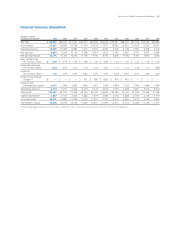

Millions of dollars except per share amounts or otherwise specified.

Notes to Consolidated Financial Statements

The Procter &Gamble Company and Subsidiaries

58

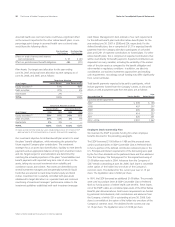

Assumed health care cost trend rates could have a significant effect

on the amounts reported for the other retiree benefit plans. A one-

percentage point change in assumed health care cost trend rates

would have the following effects:

One-Percentage One-Percentage

Point Increase Point Decrease

Effect on total of service and interest

cost components $ 57 $ (41)

Effect on postretirement benefit obligation 484 (371)

Plan Assets. Our target asset allocation for the year ending

June 30, 2007 and actual asset allocation by asset category as of

June 30, 2006, and 2005, are as follows:

Target Asset Allocation

Asset Category Pension Benefits Other Retiree Benefits

Equity securities(1) 51% 96%

Debt securities 47% 4%

Real estate 2% —

TOTAL 100% 100%

Actual Asset Allocation at June 30

Pension Benefits Other Retiree Benefits

Asset Category 2006 2005 2006 2005

Equity securities(1) 59% 64% 96% 99%

Debt securities 39% 33% 4% 1%

Real estate 2% 3% ——

TOTAL 100% 100% 100% 100%

(1) Equity securities for other retiree plan assets include Company stock, net of Series B ESOP

debt (see Note 5), of $2,693 and $2,604 as of June 30, 2006 and 2005, respectively.

Our investment objective for defined benefit plan assets is to meet

the plans‘ benefit obligations, while minimizing the potential for

future required Company plan contributions. The investment

strategies focus on asset class diversification, liquidity to meet benefit

payments and an appropriate balance of long-term investment return

and risk. Target ranges for asset allocations are determined by

matching the actuarial projections of the plans‘ future liabilities and

benefit payments with expected long-term rates of return on the

assets, taking into account investment return volatility and

correlations across asset classes. Plan assets are diversified across

several investment managers and are generally invested in liquid

funds that are selected to track broad market equity and bond

indices. Investment risk is carefully controlled with plan assets

rebalanced to target allocations on a periodic basis and continual

monitoring of investment managers’ performance relative to the

investment guidelines established with each investment manager.

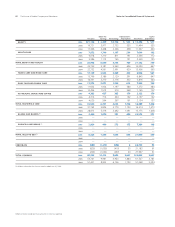

Cash Flows. Management‘s best estimate of our cash requirements

for the defined benefit plans and other retiree benefit plans for the

year ending June 30, 2007 is $398 and $24, respectively. For the

defined benefit plans, this is comprised of $137 in expected benefit

payments from the Company directly to participants of unfunded

plans and $261 of expected contributions to funded plans. For other

retiree benefit plans, this is comprised of expected contributions that

will be used directly for benefit payments. Expected contributions are

dependent on many variables, including the variability of the market

value of the plan assets as compared to the benefit obligation and

other market or regulatory conditions. In addition, we take into

consideration our business investment opportunities and resulting

cash requirements. Accordingly, actual funding may differ significantly

from current estimates.

Total benefit payments expected to be paid to participants, which

include payments funded from the Company‘s assets, as discussed

above, as well as payments paid from the plans, are as follows:

Other

Years ended June 30 Pension Benefits Retiree Benefits

Expected benefit payments

2007 $ 399 $ 190

2008 407 207

2009 405 223

2010 414 237

2011 426 251

2012 – 2016 2,337 1,367

Employee Stock Ownership Plan

We maintain the ESOP to provide funding for certain employee

benefits discussed in the preceding paragraphs.

The ESOP borrowed $1.00 billion in 1989 and the proceeds were

used to purchase Series A ESOP Convertible Class A Preferred Stock

to fund a portion of the defined contribution retirement plan in the

U.S. Principal and interest requirements of the borrowing were paid

by the Trust from dividends on the preferred shares and from advances

from the Company. The final payment for the original borrowing of

$1.00 billion was made in 2004. Advances from the Company of

$237 remain outstanding at June 30, 2006. Each share is convertible

at the option of the holder into one share of the Company‘s

common stock. The dividend for the current year was $1.15 per

share. The liquidation value is $6.82 per share.

In 1991, the ESOP borrowed an additional $1.00 billion. The proceeds

were used to purchase Series B ESOP Convertible Class A Preferred

Stock to fund a portion of retiree health care benefits. These shares,

net of the ESOP’s debt, are considered plan assets of the Other Retiree

Benefits plan discussed above. Debt service requirements are funded

by preferred stock dividends, cash contributions and advances from

the Company, of which $51 is outstanding at June 30, 2006. Each

share is convertible at the option of the holder into one share of the

Company‘s common stock. The dividend for the current year was

$1.15 per share. The liquidation value is $12.96 per share.