Panera Bread 2005 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2005 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

31

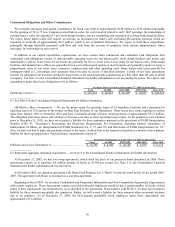

Our capital requirements, including development costs related to the opening or acquisition of additional bakery-cafes and fresh

dough facilities and maintenance and remodel expenditures, have and will continue to be significant. Our future capital requirements

and the adequacy of available funds will depend on many factors, including the pace of expansion, real estate markets, site locations,

and the nature of the arrangements negotiated with landlords. We believe that our cash flow from operations and the exercise of

employee stock options, supplemented, where necessary, by borrowings on our revolver, will be sufficient to fund our capital

requirements for the foreseeable future.

Impact of Inflation

In the past, we have been able to recover inflationary cost and commodity price increases, including, among other things, fuel,

butter, tuna, and cream cheese costs, through increased menu prices. There have been, and there may be in the future, delays in

implementing such menu price increases, and competitive pressures may limit our ability to recover such cost increases in their

entirety. Historically, the effects of inflation on our net income have not been materially adverse.

A majority of our employees are paid hourly rates related to federal and state minimum wage laws. Although we have and will

continue to attempt to pass along any increased labor costs through food price increases, there can be no assurance that all such

increased labor costs can be reflected in our prices or that increased prices will be absorbed by consumers without diminishing to

some degree consumer spending at the bakery-cafes. However, we have not experienced to date a significant reduction in bakery-cafe

profit margins as a result of changes in such laws, and management does not anticipate any related future significant reductions in

gross profit margins.

Recent Accounting Pronouncements

In December 2004, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards

(SFAS) No. 123R, “Share-Based Payment” (“SFAS 123R”), a revision of SFAS No. 123, “Accounting for Stock-Based

Compensation.” SFAS 123R will require us to, among other things, measure employee stock-based compensation awards where

applicable using a fair value method and record related expense in our consolidated financial statements. The provisions of SFAS

123R are effective for public companies for annual periods beginning after June 15, 2005. We anticipate we will adopt SFAS 123R

effective December 28, 2005 using the modified prospective transition approach and estimate adoption of the expensing requirements

will reduce our diluted earnings per share by $0.13 in 2006.

In December 2004, the FASB issued FASB Staff Position No. FAS 109-1, “Application of SFAS No. 109, Accounting for Income

Taxes, to the Tax Deduction on Qualified Production Activities provided by the American Jobs Creation Act of 2004” (“FSP 109-1”).

FSP 109-1 states that qualified domestic production activities should be accounted for as a special deduction under SFAS No. 109,

“Accounting for Income Taxes.” The provisions of FSP 109-1 are effective immediately. Adoption of this pronouncement did not

have a significant impact on our financial statements.

On October 6, 2005, the FASB issued FASB Staff Position No. FAS 13-1, “Accounting for Rental Costs Incurred During a

Construction Period” (“FSP 13-1”). FSP 13-1 is effective for the first reporting period beginning after December 15, 2005. FSP 13-1

states that rental costs associated with operating leases must be recognized as rental expense allocated on a straight-line basis over the

lease term, which includes the construction period. This accounting is consistent with our current practice.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We manage our commodity market risk in several ways. As of December 27, 2005, we had two swap agreements which fixed the

price of our projected butter purchases in 2006. All derivative instruments are entered into for other than trading purposes. See Note 2

to the Consolidated Financial Statements for further information on these derivatives. In addition, we purchase certain commodities,

such as flour and coffee, for use in our business. These commodities are sometimes purchased under agreements of one to three year

time frames usually at a fixed price. As a result, we are subject to market risk that current market prices may be above or below our

contractual price.

Our unsecured revolver bears an interest rate using LIBOR as the basis, and therefore is subject to additional interest expense

should there be an increase in LIBOR interest rates. We have not borrowed under the revolver in the last three years. As of December

27, 2005, we had no foreign operations, and accordingly, no foreign exchange rate fluctuation risk at that time.